The practical answer

- Short answer

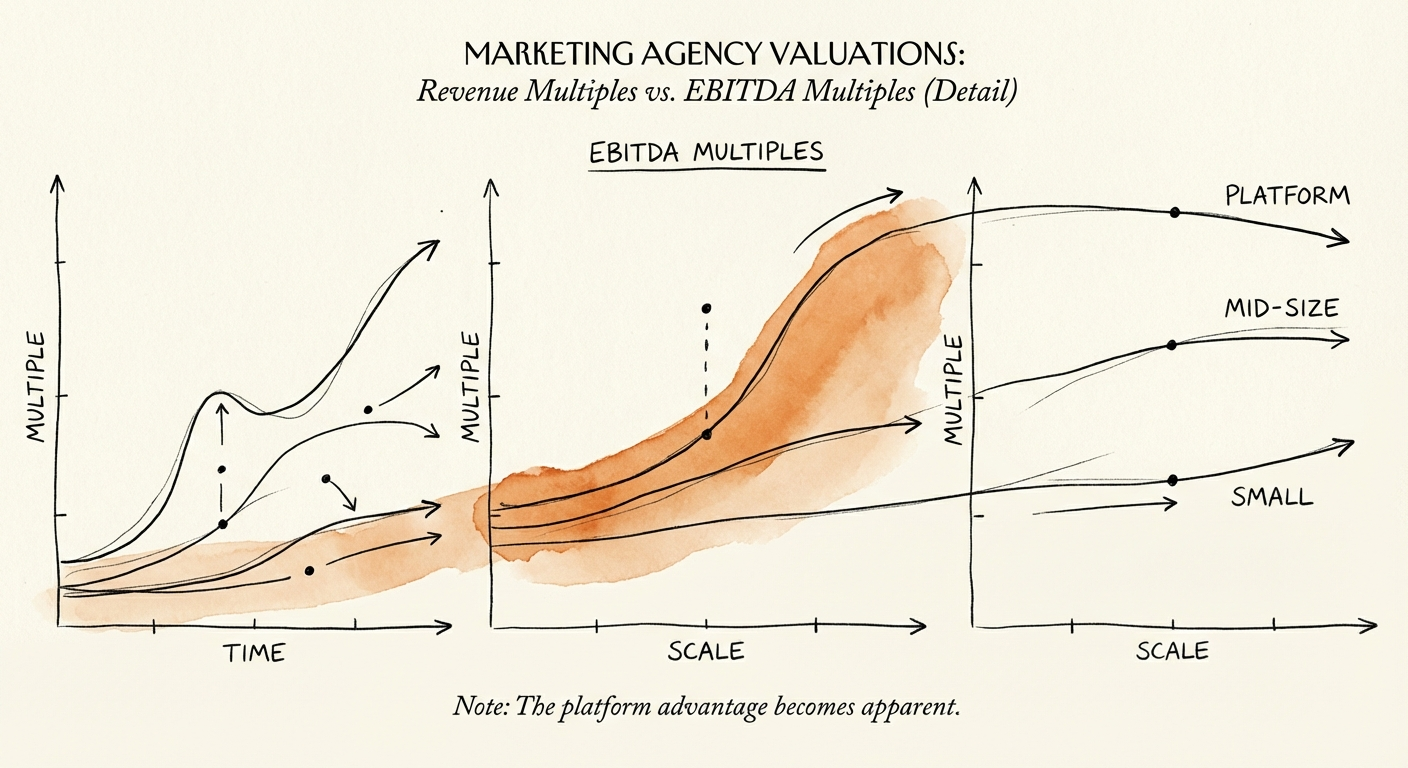

- Marketing agencies trade at ~1.2x revenue but 6.5x EBITDA — and 3x to 12x by size. Why buyers pay for EBITDA, not top line, and how to reach the top range.

- Best fit

- Industry: Marketing Services. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 6.5x Median EBITDA Multiple (2025)

The Founder's Delusion: Why You Think You're SaaS

You have hit $10M in revenue. You look at the public markets, you read TechCrunch, and you see SaaS companies trading at 10x revenue. You do the napkin math: $10M × 10 = $100M valuation. You order the expensive champagne.

Then you speak to an M&A advisor, and the hangover hits immediately.

Unless you are a pure-play software platform with 90% gross margins and zero professional services, you are not getting a revenue multiple. You are a service business. You sell time, talent, and outcomes—not code. And in the eyes of a private equity buyer or a strategic acquirer in 2026, you are valued on one metric: EBITDA.

The gap is brutal. While SaaS firms might command 6x–10x revenue, the median marketing agency in 2025 trades at 1.2x revenue. If you are unprofitable, you might be worth nothing at all, regardless of your top-line growth. This is the valuation gap that blindsides founders during their first exit conversation.

Buyers view agencies through a lens of risk. Unlike software, your assets go down the elevator every night. If your creative director quits or your biggest client walks, your revenue evaporates. That risk profile demands a valuation model based on cash flow, not hype. To a buyer, your revenue is vanity; your EBITDA is sanity.

To a buyer, your revenue is vanity; your EBITDA is sanity. A $50M revenue agency with 5% margins is worth less than a $10M agency with 30% margins.

The 2025 Valuation Landscape: Hard Numbers

Let’s look at the data from the trenches. Following the interest rate cuts in late 2024, M&A activity surged 22% in Q4, but buyers remained disciplined. The days of paying for "potential" are over. Today, buyers pay for Transferable EBITDA.

EBITDA Benchmarks by Size

According to 2025 transaction data from leading M&A advisors, agency multiples have bifurcated based on scale and specialization:

- Small Agencies ($500k – $1M EBITDA): Trade at 3.0x – 5.0x. At this size, you are buying a job, not a business. Key-person risk is high.

- Mid-Market Agencies ($2M – $5M EBITDA): Trade at 5.0x – 7.0x. This is the sweet spot where systems begin to replace founder heroics.

- Platform Agencies ($5M+ EBITDA): Trade at 8.0x – 12.0x. These firms have proven management teams, diversified revenue, and proprietary IP.

The "Quality of Revenue" Multiplier

Not all EBITDA is created equal. A dollar of EBITDA from a project-based web dev shop is worth less than a dollar of EBITDA from a performance marketing retainer. Buyers apply a "Quality of Revenue" scorecard that can swing your multiple by 2-3 turns:

- Recurring vs. Project: 70%+ recurring revenue commands a premium. If you have to resell your entire capacity every January 1st, expect a discount.

- Client Concentration: If one client is >20% of revenue, you have a whale trap problem. Buyers will structure the deal with heavy earn-outs to protect themselves.

- Tech-Enablement: Agencies that use proprietary tech to drive efficiency (e.g., automated reporting, AI-driven bid management) trade closer to the top of the range because their margins are defensible.

The math is unforgiving. A $50M revenue agency with 5% margins ($2.5M EBITDA) trading at 6x is worth $15M. That is a 0.3x revenue multiple. If you want a higher valuation, stop chasing empty calorie revenue and fix your EBITDA calculation.

The Bridge to 10x: How to Engineer Your Multiple

You cannot change the market reality that agencies are valued on EBITDA. But you can engineer your business to command the top of the range. The difference between a 4x exit and an 8x exit on $3M EBITDA is $12M in your pocket. Here is the playbook to bridge that gap.

1. Productize Your Service Delivery

The biggest drag on agency valuations is the "custom work" trap. If every project requires a unique scope and a unique team, your margins will never scale. You need to turn your service into a product. Define standard packages, standard deliverables, and standard pricing. This allows you to document processes and lower the skill level required for delivery, expanding your gross margins.

2. Diversify or Die

If your top customer leaves tomorrow, does your EBITDA drop by 50%? If yes, you are not exit-ready. Aggressively hunt for new business in different verticals to dilute your concentration. No single client should represent more than 15% of your Gross Profit. This is the single fastest way to de-risk your deal and increase the cash-at-close component.

3. Clean Up Your Financial House

Buyers don’t trust "Founder Math." If you are running personal expenses through the business or mixing cash and accrual accounting, you will get crushed in Quality of Earnings (QofE). Implement ASC 606 revenue recognition standards now. Hire a fractional CFO to build a data room that tells a clean story. When a buyer sees audited financials and a clear EBITDA bridge, their confidence—and their offer price—goes up.

Conclusion

Valuation is not a lottery ticket; it is a report card on your operational maturity. The market is telling you exactly what it values: predictability, profitability, and transferability. Stop trying to convince buyers you are a SaaS company and start building the best damn service operation they have ever seen.