The practical answer

- Short answer

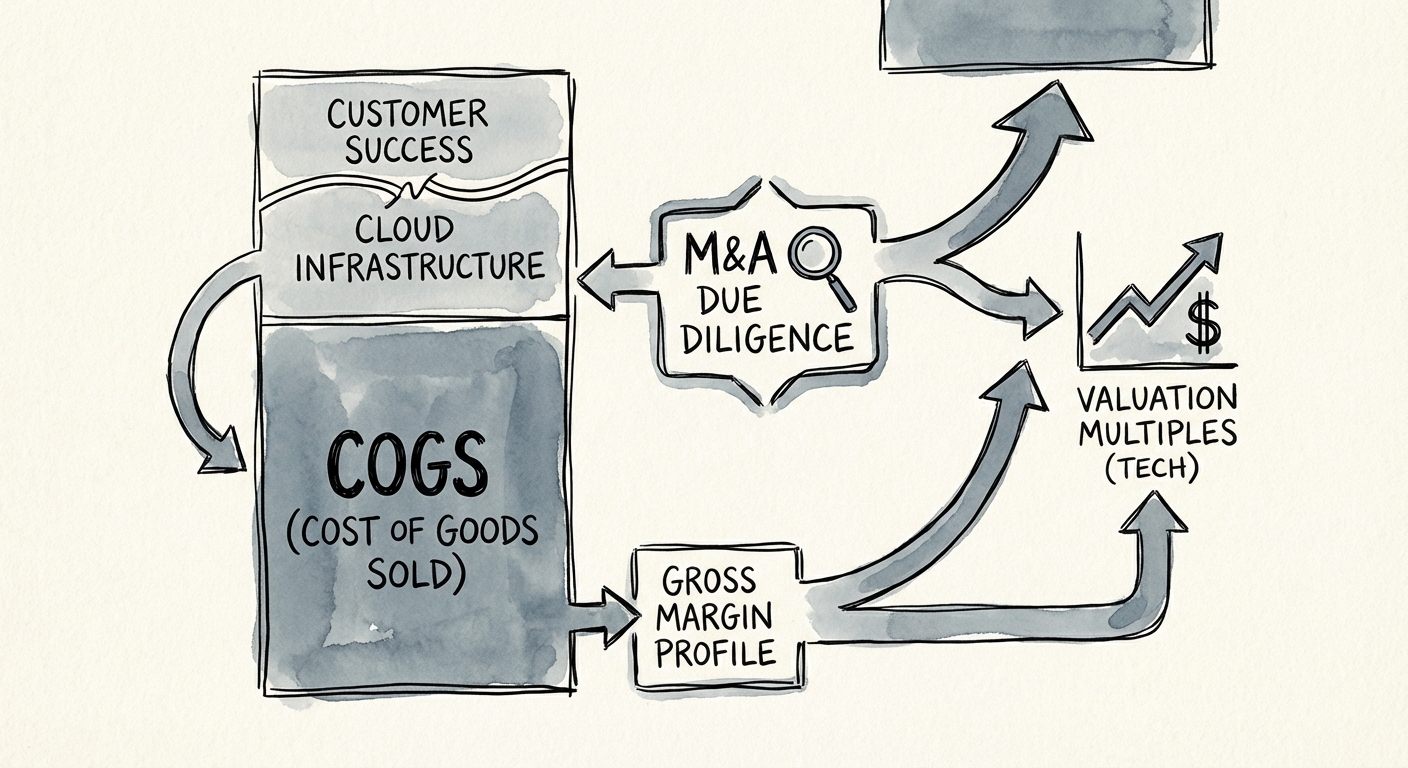

- New 2025 data shows SaaS companies with >80% gross margins trade at a 105% valuation premium over those below 60%. Here is the diagnostic guide to fixing your COGS before exit.

- Best fit

- Industry: B2B Technology. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 105% Valuation premium for SaaS companies with >80% Gross Margins vs. those with <60%.

The 3.7x Turn Gap: Why Margins Matter More Than Growth in 2026

For the last decade, revenue growth was the primary driver of valuation multiples. In 2026, that era is over. Private equity buyers and strategic acquirers have shifted their focus to unit economics, and specifically, Gross Margin Profile as the truest indicator of scalability.

Recent 2025 M&A market data reveals a stark bifurcation in valuation multiples based on gross margin thresholds. SaaS companies with gross margins above 80% are currently trading at a median of 7.2x EV/Revenue. In contrast, software companies with gross margins below 60%—often due to heavy services components or inefficient infrastructure—are trading at just 3.5x EV/Revenue.

This represents a 105% valuation premium for elite margin profiles. For a company with $20M in ARR, moving from a 55% margin profile to an 80% margin profile isn't just an operational improvement; it is a $74M increase in Enterprise Value. The market is effectively telling founders: if your revenue requires significant human capital or infrastructure to deliver, we will price you as a service provider, not a software platform.

The market is effectively telling founders: if your revenue requires significant human capital to deliver, we will price you as a service provider, not a software platform.

The "Hidden" COGS That Kill Your Multiple

Many scaling CEOs, particularly those we call "founders," unintentionally depress their valuations by misclassifying costs or allowing inefficiencies to bloat their Cost of Goods Sold (COGS). When we conduct Quality of Earnings (QofE) preparation, we frequently find three "silent killers" of gross margin.

1. The Customer Success Trap

Is your Customer Success team doing technical support? If they are fixing bugs, answering "how-to" tickets, or manually onboarding users, those salaries belong in COGS, not Sales & Marketing. Buyers will reclassify these expenses during due diligence, often causing a 5-10% drop in your adjusted gross margin overnight. True "Success" (renewals and upsells) is OpEx; "Support" is COGS.

2. The Cloud Waste

In the rush to scale, infrastructure efficiency often takes a backseat. We see B2B SaaS companies paying 15-20% of revenue to AWS or Azure because of unoptimized instances and lack of reserved capacity. Elite SaaS companies keep hosting costs under 5-8% of revenue. This excess spend is a direct hit to your valuation multiple.

3. The Professional Services Drag

If you bundle implementation into your subscription price to win deals, you are effectively providing free services. This depresses your recurring revenue margin. Buyers prefer to see a lower-margin Professional Services line item (even if it breaks even) separate from a pristine 85% Subscription Gross Margin. Blending them hides your true software scalability.

The Path to the 7x Multiple

Achieving an 80% gross margin profile requires a deliberate architectural and operational shift. It is rarely solved by "cutting costs" alone; it is solved by automation and pricing strategy.

First, analyze your revenue mix and margin benchmarks. If your "software" revenue includes manual data entry or human-in-the-loop verification, you must automate those processes or accept a lower multiple. Second, scrutinize your hosting bill. Implementing a FinOps practice to manage cloud spend can often recover 2-3 margin points within a quarter.

Finally, utilize gross margin expansion levers before you go to market. Migrating legacy single-tenant customers to multi-tenant environments, enforcing strict limits on "free" support hours, and raising prices on grandfathered cohorts are the fastest ways to signal to buyers that you possess the pricing power and operational discipline of a premium asset.