The practical answer

- Short answer

- Learn which technology costs qualify as EBITDA add-backs in 2026. A diagnostic guide for founders and PE firms on defending 'one-time' tech investments in due diligence.

- Best fit

- Industry: Private Equity. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 66% Average add-backs as a percentage of LTM EBITDA in 'High Technology' deals (PitchBook).

The $2 Million Mistake in Your Quality of Earnings

In the high-stakes theater of M&A due diligence, the battleground has shifted from revenue recognition to the purity of EBITDA. For technology companies, this battle is particularly bloody. According to PitchBook data, “high technology” companies now average add-backs totaling 66.1% of their LTM EBITDA—the highest of any sector. This massive disparity between reported and adjusted earnings has put private equity buyers on high alert.

The central conflict lies in the definition of “one-time.” Founders view a $2 million cloud migration as a singular, heroic event—a transformation that sets the stage for future scale. Buyers, however, increasingly view these costs as deferred maintenance or “continuous modernization”—recurring operating expenses necessary just to stay competitive. When a buyer reclassifies a $500,000 “one-time” technology project as recurring OpEx, at a 12x multiple, you don’t just lose the deduction; you lose $6 million in Enterprise Value.

This diagnostic framework helps founders and CFOs distinguish between defensible technology add-backs and the “digital transformation” fluff that gets shredded in Quality of Earnings (QofE) reports. To survive the 2026 due diligence environment, you must stop treating “tech debt” as an accounting bucket and start treating it as a distinct, auditable investment class.

In 2026, 'Digital Transformation' is no longer a valid EBITDA add-back. It's just the cost of doing business. If you can't prove it has a start date, an end date, and a distinct ROI, it's operating expense.

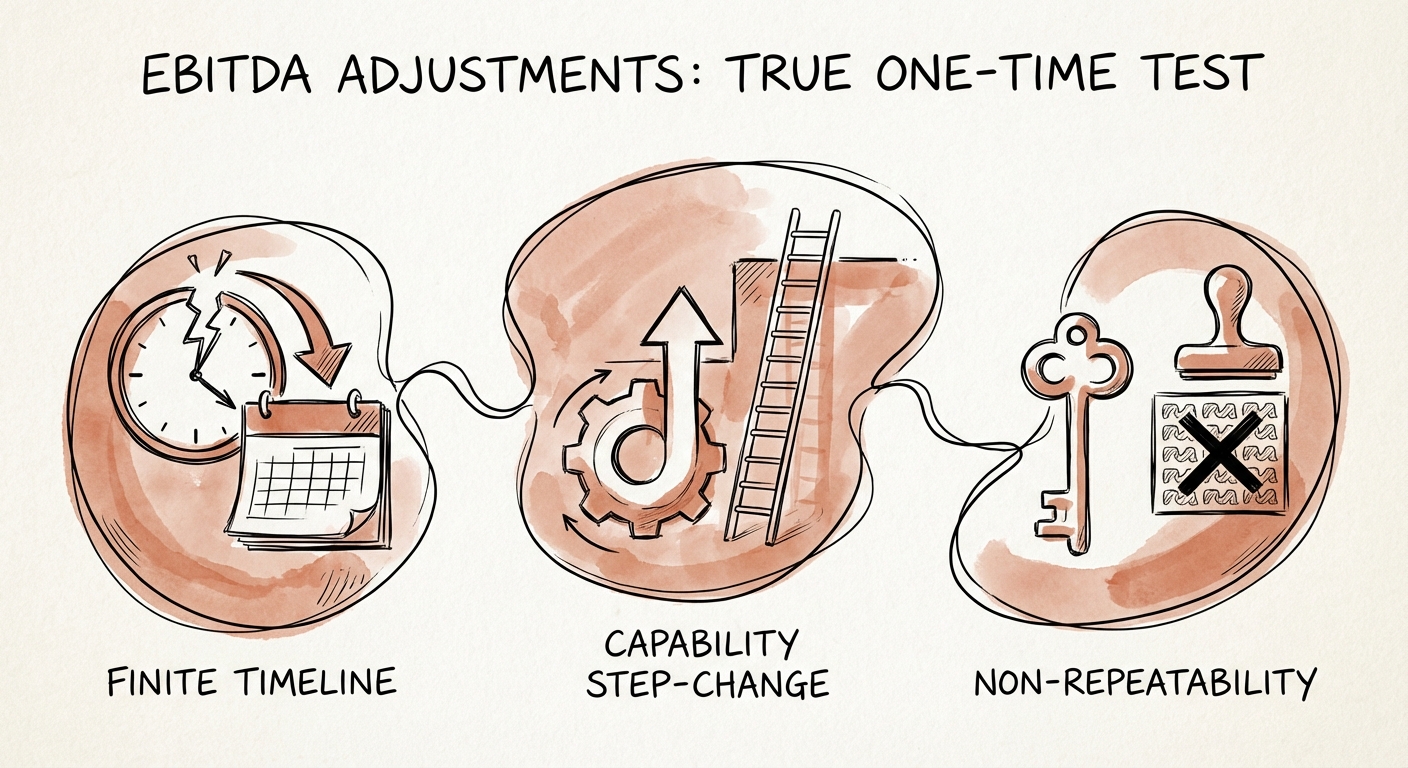

The “True One-Time” Diagnostic Test

Not all technology spend is created equal. To defend an add-back in a Quality of Earnings report, the expense must pass the “True One-Time” test. This rigorous three-part framework is used by top-tier accounting firms to validate adjustments.

1. The Finite Timeline Test

A true one-time project has a Scope of Work (SOW) with a hard start date and a hard end date. If you are paying a vendor “Time & Materials” (T&M) for “ongoing cloud optimization,” that is not an add-back; it is staff augmentation. Defensible add-backs are tied to milestones, not hours.

2. The Capability Step-Change Test

Does this investment create a new capability, or does it merely repair an existing one? Migrating from a legacy on-premise ERP to NetSuite is a capability step-change (Defensible). Rewriting spaghetti code because your MVP wasn’t scalable is “deferred maintenance” (Red Flag). Buyers view the latter as the cost of technical negligence, which they will not credit back to your profitability.

3. The Non-Repeatability Test

Will you need to do this again in 36 months? This is where “Digital Transformation” add-backs often fail. If your roadmap shows a major platform refactor every three years, that cost is effectively amortized R&D, not a one-time event. You must prove that this specific investment resolves a structural bottleneck permanently.

Three Dangerous Add-Back Categories (And How to Fix Them)

Our analysis of 2025 deal data highlights three specific areas where tech add-backs are most frequently rejected.

1. The “Tech Debt Paydown” Trap

Founders love to classify code refactoring as a one-time expense. Buyers argue that if you didn’t pay down tech debt, your product would fail; therefore, it is an operational necessity. The Fix: Frame these costs as “Platform Re-Architecture” tied to a specific strategic pivot (e.g., “Enabling Enterprise Multi-Tenancy”), rather than generic “cleanup.” Use our Technical Debt Quantification Framework to assign specific dollar values to the liability being removed.

2. The “SaaS Implementation” Grey Area

Implementing a new CRM or ERP is costly. However, the internal labor allocated to these projects is often rejected as an add-back because those employees would have been paid regardless. The Fix: You must strictly segregate “Run” vs. “Change” time. Use project codes in your timesheet software to prove that 40% of your VP of Engineering’s time was explicitly diverted to the integration, necessitating backfill or temporary degradation of other duties.

3. The “Synergy” Hallucination

Projected cost savings from new tech stacks are the most rejected class of add-back (nearly 30% rejection rate). Buyers simply do not believe that implementing Salesforce will allow you to fire three sales reps. The Fix: Only claim realized synergies. If you implemented an AI agent and actually reduced headcount by Q4, that is defensible. Hypothetical future efficiencies are credibility killers.

For a complete list of what currently passes scrutiny, review our guide on 15 EBITDA Add-Backs PE Firms Will Actually Accept.