The practical answer

- Short answer

- In a SaaS acquisition, the buyer's PPA can assign your code an 18-month useful life and quietly gut a Net-Income earnout. Here's how to fight it pre-close.

- Best fit

- Industry: Private Equity. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 55-65% Average allocation to Goodwill in 2025 SaaS acquisitions, reflecting high valuations relative to tangible assets.

You won the price. Then a spreadsheet you never saw changed the math.

Picture a 60-person vertical SaaS company that just signed at a number everyone in the room felt good about. Founder rolls some equity, takes a Net-Income earnout for the rest, shakes hands. Six weeks later, a valuation analyst at the buyer's firm—someone the founder will never meet—opens a model and types a single assumption into a cell: developed technology, useful life, 24 months. That keystroke just reshaped the next three years of the founder's P&L, and nobody asked.

That model is the Purchase Price Allocation. It splits the price you agreed on across three buckets: tangible assets (the laptops, the cloud commitments), identifiable intangibles (your code, your customer base, your brand), and Goodwill—the residual that's left when the price exceeds what you can pin to a specific asset. Most founders treat the PPA as the buyer's homework, due long after the wire clears. It is, in fact, the place where the dollars you negotiated quietly get recategorized into the dollars you actually receive.

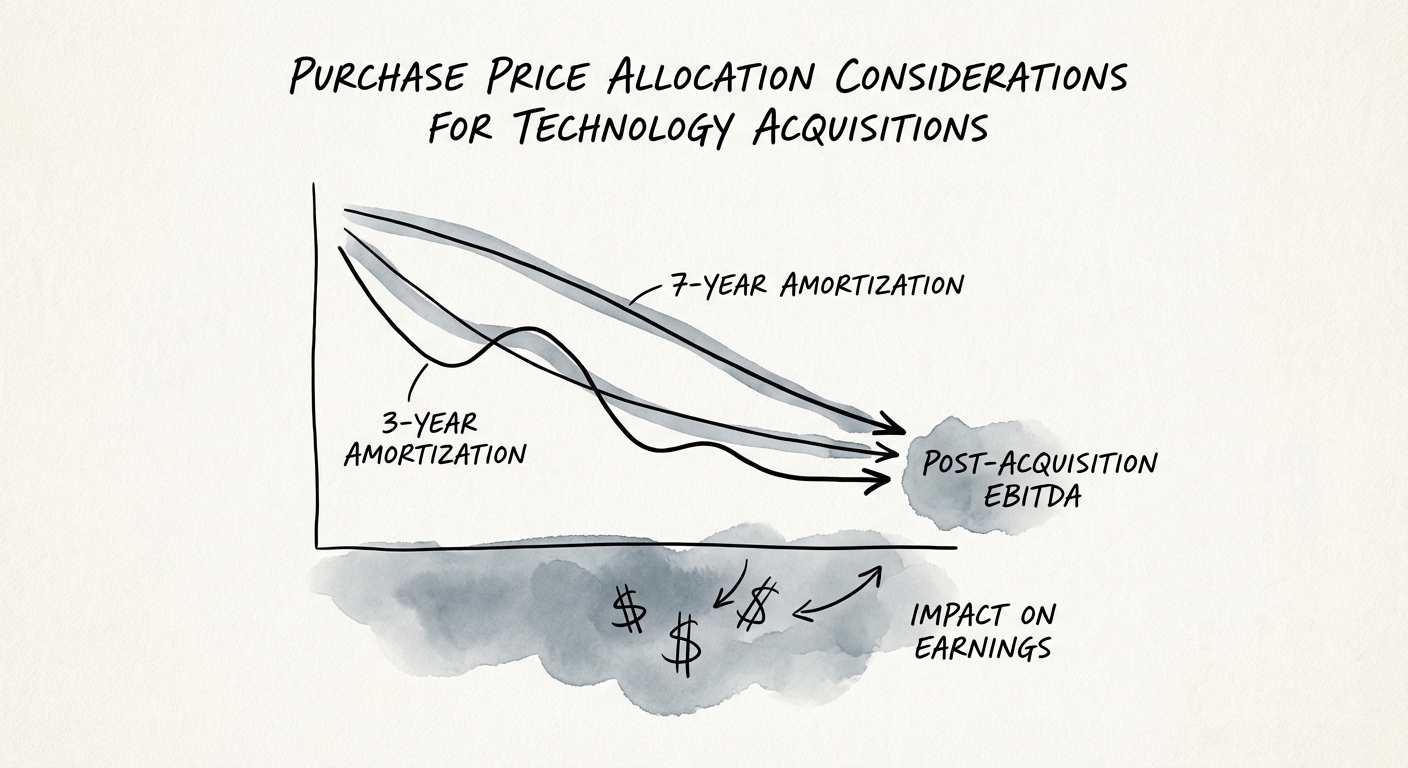

The fight is almost entirely about your code. Buyers are incentivized to call "developed technology" short-lived—amortize it fast, reset the asset base, take the GAAP earnings hit now while the deal is still being explained to the board as transformational. The same Quality-of-Earnings scrutiny that priced your recurring revenue down to the dollar turns, in PPA, into pressure to label your platform a depreciating bridge to a rewrite. Stout's allocation work shows the SaaS mix has been sliding toward Goodwill and away from technology precisely because of these compressed obsolescence assumptions (Stout, "Purchase Price Allocation Study 2025," October 2025). That slide isn't accounting trivia. If your earnout keys off Net Income or EBIT, a fat amortization charge on a short-lived software asset is a fixed expense sitting on your number every quarter you're trying to hit it.

The earnout you signed and the useful life the buyer's valuation firm assigns to your code are the same number argued from two ends of the table. If you only negotiate one of them, you negotiated half a deal.

Run the arithmetic the buyer is running, because they already did.

Take the hypothetical 60-person SaaS firm and say the deal allocates roughly a fifth of the price to developed technology. Amortize that over seven years and the annual charge is modest. Compress it to two and the charge nearly quadruples—a hard line through your operating income every period of the earnout window. EBITDA-focused PE buyers shrug, because amortization adds back. But a Net-Income earnout doesn't add it back, and neither does a strategic acquirer watching EPS. The shorter the useful life, the lower the earnings you're measured against, the further away your payout. The buyer isn't being malicious; they're optimizing their own books. The problem is the two of you optimized in opposite directions and only one of you saw the model.

The hook the buyer reaches for is your technical due diligence. Every remediation item their diligence team flagged becomes ammunition: if the platform needs work, the argument goes, its remaining useful life is short. We routinely see older codebases land 18-to-24-month useful-life designations on exactly this logic—the platform reframed as disposable. Deloitte's PPA guidance is blunt that useful-life and discount-rate assumptions are where most of the subjectivity (and most of the disagreement) lives (Deloitte, "Purchase Price Allocation (PPA) Guide," October 2025).

There's a second move worth watching, and it's a tax move. Value the buyer strips off "technology" doesn't vanish—it usually drifts into Goodwill. In a straight stock purchase, that Goodwill generally isn't tax-deductible for the buyer; in an asset deal or a 338(h)(10) election, it amortizes over 15 years for tax. So a buyer may push a Goodwill-heavy allocation to stretch their own tax benefit—fine for them, but if it drags down the very Net-Income line your earnout rides on, you're subsidizing their tax planning with your payout. Grant Thornton frames PPA as a management problem precisely because these allocation choices ripple into earnings, covenants, and reporting long after close (Grant Thornton, "Purchase Price Allocation: Challenges for Management," January 2024).

What current SaaS allocations actually look like

For grounding, not as targets to demand:

- Goodwill: roughly 55-65%, rising as deal prices outrun tangible asset bases.

- Developed technology: roughly 15-20%, drifting down as useful-life assumptions compress.

- Customer relationships: roughly 10-15%, with churn assumptions under heavier scrutiny.

- Trademarks and brand: low single digits.

What to do before you sign, while you still have leverage

The mistake is treating PPA as something that happens to you after close. It's an input you can shape while the buyer still wants the deal. Three concrete moves:

1. Put the principle in the LOI, not the price in the PPA. You won't dictate the buyer's final allocation, but you can refuse a blank "customary allocation" clause and instead negotiate an agreed methodology—especially that the earnout calculation adds back acquisition-driven amortization, or is computed on a defined basis insulated from the PPA. Get the principle locked in writing alongside the LOI. After signing, the buyer's only incentive is their own book.

2. Build the useful-life defense before diligence starts. If you believe your platform has real shelf life, document it now: your modernization history, your architecture decisions, your forward roadmap. The same integration and platform evidence that justifies a longer useful life is the evidence that blunts a valuation firm's reflexive 3-year default. A founder who hands the analyst a credible longevity case changes the starting assumption in that cell. A founder who says nothing accepts whatever default the analyst types.

3. Make tax counsel review allocations early—watch non-competes and personal goodwill. Be wary of value routed into a "non-compete agreement." For a seller, that can recharacterize what should be capital gains as ordinary income, and the rate gap is real money. The split between personal goodwill and corporate goodwill carries its own tax consequences. None of this is fixable after the definitive agreement is signed—so it gets reviewed before, not during the wire.

Here's the Monday version: pull your last signed LOI or term sheet and find the sentence that defines how the earnout is calculated. If it doesn't explicitly neutralize acquisition-driven amortization, you have an exposure you can still close. A few points of allocation shifting from Goodwill onto a short-lived software asset can move post-tax proceeds and earnout payouts by seven figures. Control that input now, or inherit whatever a stranger's spreadsheet decides later.