The practical answer

- Short answer

- New 2026 data reveals how technical debt creates a 30% valuation discount in PE exits. Learn the benchmarks for code aging and remediation costs.

- Best fit

- Industry: Private Equity. Function: Technology Strategy

- Operating path

- Technical Debt → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 40% Higher failure rate of IT modernization projects in high-debt companies compared to low-debt peers.

The Invisible CapEx on Your Balance Sheet

For years, Private Equity operating partners viewed technical debt as an engineering complaint—a friction to be managed, not a liability to be priced. That era is over. In 2026, technical debt is no longer just an operational nuisance; it is a quantified valuation discount applied directly to Enterprise Value (EV) during due diligence. Recent data from the Consortium for Information & Software Quality (CISQ) places the cost of poor software quality in the U.S. at over $2.4 trillion, but the number that matters for PE Operating Partners is the specific impact on deal value.

When a buyer evaluates your portfolio company, they are not just buying the current revenue stream; they are buying the future cost of maintaining that stream. If your codebase requires a "Grand Rewrite" to scale or secure, that future CapEx is deducted from your exit price today. We call this the Legacy Code Discount.

According to recent quantification frameworks, this discount often hits 30% of the target valuation. Why 30%? It represents the convergence of three factors: direct remediation costs (typically 15-20% of the technology estate's value), the "Growth Drag" associated with slower feature velocity, and the risk premium buyers demand for assuming the modernization burden. If your engineering team spends 33% of their time fixing bugs instead of shipping features—a common benchmark for high-debt organizations—buyers will mathematically adjust your growth projections downward, compressing the multiple before they even subtract the remediation costs.

Tech debt is the off-balance-sheet accumulation of technology work a company needs to do in the future. In M&A, that future work is priced as a current liability.

The Valuation Math: Why 20% Less Growth = 30% Less Value

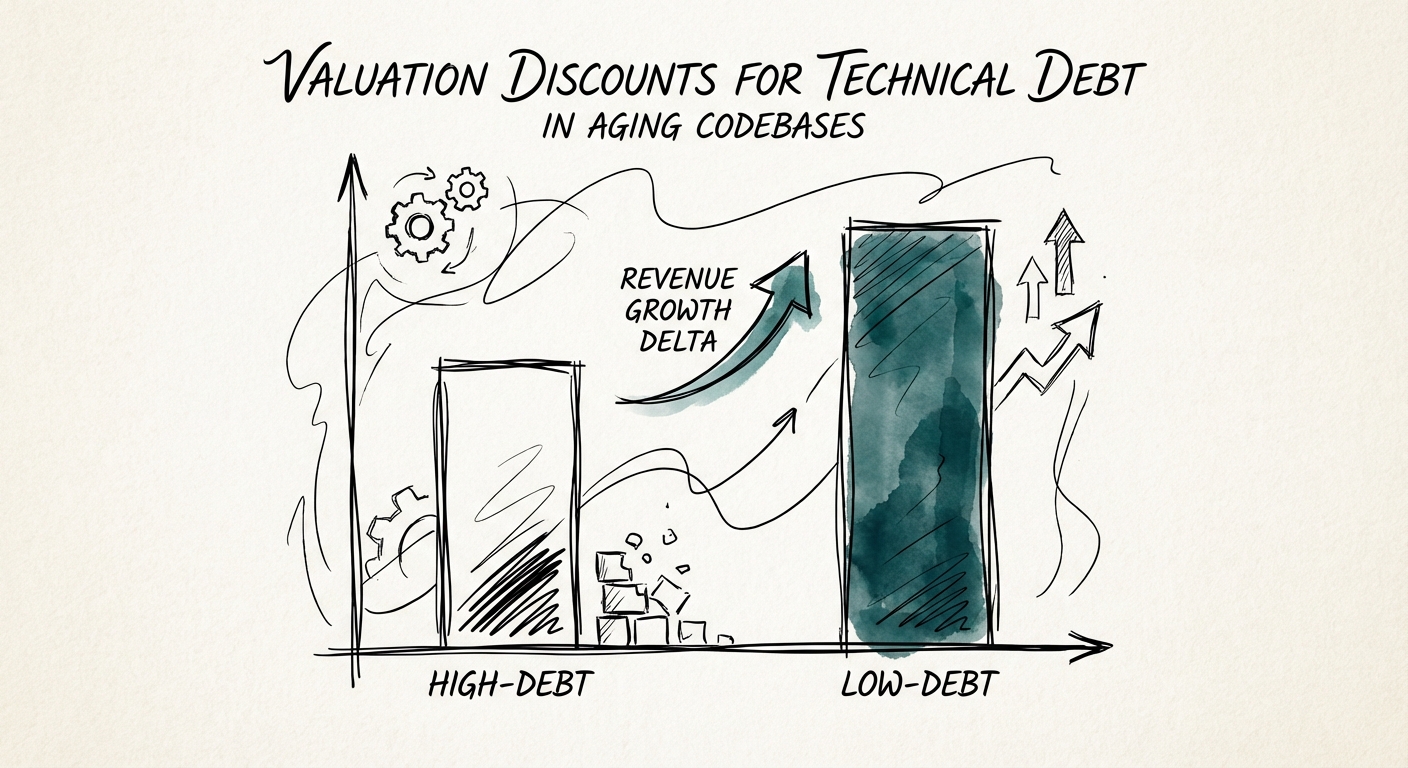

The correlation between code quality and business performance is increasingly visible in diligence. McKinsey analysis of over 200 companies found that organizations in the top 20% for technical health (low debt) achieved 20% higher revenue growth than their bottom-tier peers. This growth delta is the primary driver of the valuation discount.

Consider two SaaS companies, both with $50M ARR. Company A has a "Clean Core" and ships weekly. Company B has a "Spaghetti Monolith" and ships monthly. Buyers know that Company B will require significantly more capital to achieve the same growth rate as Company A. In due diligence, this shows up as a "Technology Risk Adjustment" to EBITDA.

Furthermore, the risk of failure in modernization projects is stark. The same data indicates that high-debt companies are 40% more likely to cancel or fail in their IT modernization efforts. This means a buyer isn't just funding a rewrite; they are betting against the odds that the rewrite will even succeed. To mitigate this risk, sophisticated acquirers are now demanding technical debt estimates that are 3x higher than what sellers typically disclose in the CIM. They aren't just looking for "spaghetti code"; they are looking for architectures where the cost of maintenance exceeds the value of the incremental revenue it supports.

The Remediation Playbook: Avoiding the 'Grand Rewrite' Trap

If you identify a high-debt asset 18-24 months before exit, you cannot afford a "Grand Rewrite." These projects almost always blow past timelines and budgets, often destroying more value than they create. Instead, the 2026 playbook for PE Operating Partners is the Strangler Fig Pattern.

This approach involves building new features in a modern microservices architecture that wraps around the legacy monolith, slowly strangling the old system over time. It allows you to demonstrate modernization momentum to buyers without pausing the product roadmap. The goal is not to reach zero debt—that's a vanity metric. The goal is to reach "Transferable Stability."

Transferable Stability means the code is documented, the high-risk dependencies are isolated, and the team has a proven velocity metric that buyers can trust. By shifting the narrative from "We need to rewrite everything" to "We have a proven migration path yielding 20% faster cycles," you can defend your multiple. The difference between a 30% discount and a premium exit often lies not in the code itself, but in the certainty you provide the buyer about the cost to fix it.