The practical answer

- Short answer

- Net Working Capital (NWC) targets can silently cost SaaS founders 10-15% of deal value. Learn how to negotiate the 'Peg' and defend deferred revenue treatment.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- $1.2M Average purchase price reduction for SaaS sellers who fail to exclude Deferred Revenue from 'Debt' definitions.

The SaaS Paradox: Why 'Negative' is Positive

In traditional manufacturing or retail M&A, buyers expect Positive Net Working Capital. They want to see that Current Assets (Inventory + Accounts Receivable) exceed Current Liabilities (Accounts Payable) to ensure the business can fund its own operations. If you are selling a widget factory, you hand over the keys and the inventory on the shelves.

But in B2B SaaS, this logic is inverted. Because your customers pay upfront (often annually), your cash balance swells while your Deferred Revenue (a liability) grows. This typically results in Negative Net Working Capital. Your business doesn't need operating capital; it generates it.

The Trap: Unsophisticated buyers (or sophisticated ones hoping you are unsophisticated) will propose a Net Working Capital (NWC) target of $0 or a 'normalized' positive number in the Letter of Intent (LOI). If you agree to a $0 target but your actual NWC is -$2M (due to deferred revenue), you will be forced to leave $2M of extra cash on the balance sheet at closing to fill the hole. That is a dollar-for-dollar reduction in your exit value that does not appear in the headline price.

Net Working Capital is not an accounting detail; it is a secondary price negotiation that typically happens after you think you've already agreed on the price.

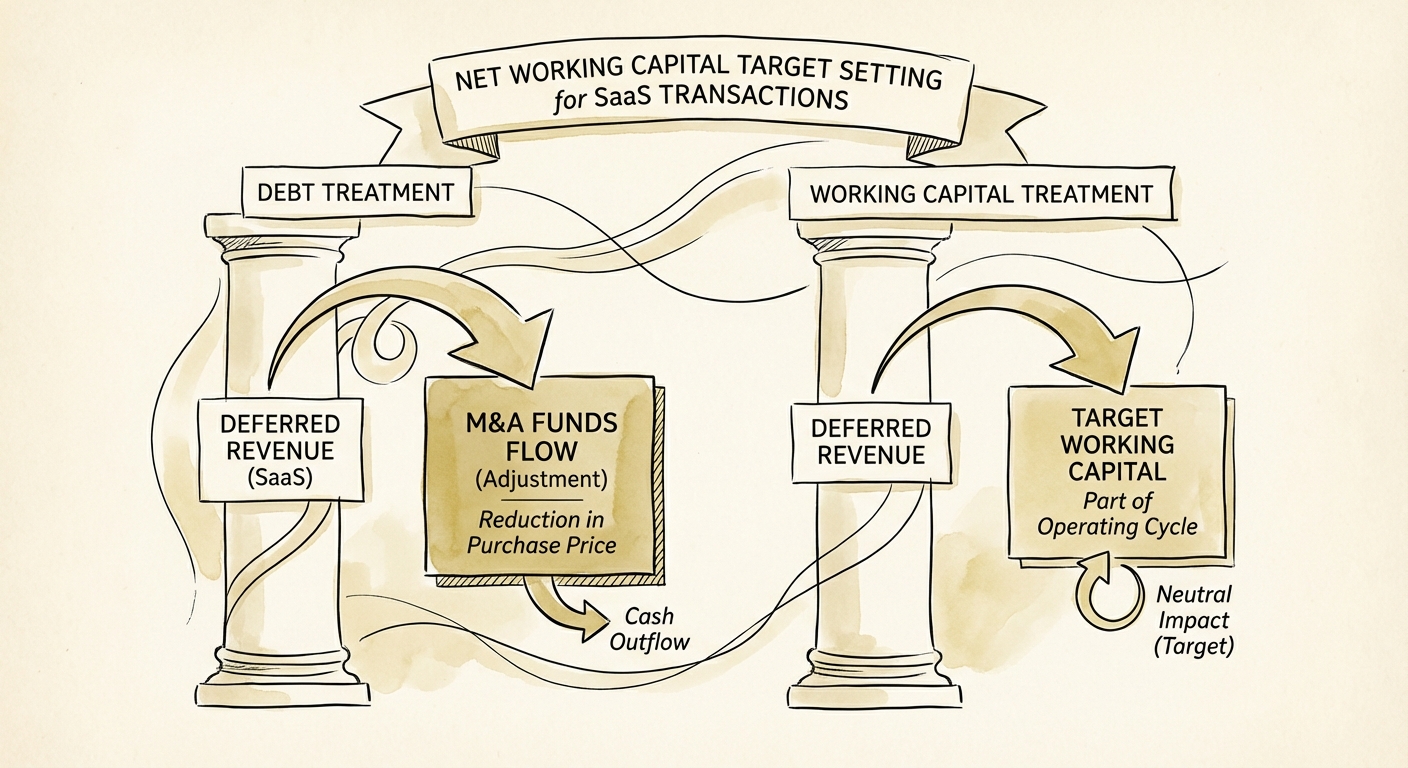

The Battleground: Deferred Revenue vs. Debt

The single most contentious line item in SaaS NWC negotiations is Deferred Revenue. In a standard "Cash-Free, Debt-Free" transaction, the buyer keeps the debt obligation and you keep the cash. The fight is over how to classify the service obligation you owe to customers who have already paid.

The Three Treatments of Deferred Revenue

- The Buyer's Move (Debt Treatment): The buyer argues that Deferred Revenue is a debt-like item. They exclude it from the NWC calculation and deduct the full balance from the purchase price. Result: You pay the buyer to service the contracts you already sold.

- The Seller's Move (Working Capital Treatment): You argue that Deferred Revenue is an operating liability, just like Accounts Payable. It stays in the NWC calculation, driving the target negative (e.g., -$2M). Result: You keep the cash associated with those pre-payments, provided you deliver the negative working capital at close.

- The Compromise (Cost-to-Serve): If the buyer refuses to treat Deferred Revenue as working capital, pivot to the "Cost-to-Serve" model. You argue that the liability isn't the revenue amount, but the cost to fulfill the service. If your gross margin is 80%, the liability is only 20% of the deferred revenue balance.

The 'Peg' Manipulation: Seasonality and Growth

Once you define what goes into the calculation, the next fight is how much. The NWC Target (or 'Peg') is typically calculated as the average of the trailing 12 months (TTM) of Net Working Capital.

For a flat business, a 12-month average works. For a scaling SaaS company, it is a mathematical trap.

The Growth Penalty

As you grow, your Deferred Revenue balance grows larger every month. A 12-month average will reflect a balance that is significantly smaller (less negative) than your current reality. If your average NWC is -$1M but your current NWC is -$2M, and you agree to the average, you are effectively penalizing yourself for growing.

The Seasonality Swing

If 60% of your renewals happen in Q4, your cash and deferred revenue spike in December. If you close your deal in June (the trough of your cash cycle), your actual NWC might be far lower than the TTM average. Buyers will demand a 'True-Up' payment to cover the difference.

Actionable Defense: Do not accept a generic TTM average. Propose a 3-month or 6-month lookback that reflects the current scale of the business, or normalize the Peg for known seasonality to avoid a massive check-swing at closing.