The practical answer

- Short answer

- Usage-based pricing models are trading at a 50% premium over seat-based SaaS. Here is the diagnostic guide to consumption pricing, NRR, and valuation multiples for 2026 exits.

- Best fit

- Industry: SaaS. Function: Pricing Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 120% Benchmark NRR for top-quartile usage-based SaaS companies in 2025 (Iconiq Growth).

The Valuation Gap: Why Seats Are Trading at a Discount

For the last decade, the "per user, per month" subscription was the gold standard of SaaS valuation. It was predictable, easy to model, and comforting to private equity investors. In 2026, that comfort has become a liability. The market has bifurcated: recent data indicates that while traditional seat-based SaaS companies are stabilizing at approximately 4x-5x revenue multiples, companies with mature usage-based pricing (UBP) models are commanding 6x to 8x multiples.

The driver of this premium is not just growth rate—though UBP companies historically grow faster—but Net Revenue Retention (NRR). Seat-based pricing has a natural ceiling: a customer only has so many employees. Once you have sold a seat to every employee, expansion stops unless you upsell new modules. Consumption pricing, however, scales with the customer's business success, uncapping NRR. Net Revenue Retention for top-quartile consumption businesses is settling in the 110-120% range, significantly outperforming the seat-based median.

Acquirers in 2026 are paying for this "expansion engine." A strategic buyer views seat-based revenue as "capped annuity" and consumption revenue as "growth equity." If you are approaching an exit with a pure seat-based model, you are likely leaving 30-50% of your potential enterprise value on the table because you cannot demonstrate the same effortless expansion dynamics as your usage-based peers.

Strategic corporate buyers are valuing predictable consumption revenue 50% higher than flat subscription revenue. The market wants the upside of usage with the safety of a contract.

The Predictability Paradox: Why "Pay-As-You-Go" Scares PE Buyers

Despite the valuation premium, there is a dangerous trap in consumption pricing: Volatility. While strategic buyers (like Salesforce or Microsoft) love the upside of usage, financial buyers (Private Equity) hate the downside risk. A pure "pay-as-you-go" model, where revenue resets to zero on the first of every month, is often treated with a valuation discount in due diligence because it lacks the contractual guarantees of a subscription.

We see this constantly in valuation assessments. A Founder presents a chart showing 150% NRR driven by usage spikes, but the PE firm's Quality of Earnings (QofE) team argues that this revenue is "non-recurring" or "one-time." They will stress-test your forecast: "What happens if the economy slows and your customers simply run fewer queries?" If you cannot answer that with contractual certainty, they will haircut your EBITDA adjustments.

This is the Predictability Paradox: To get the highest multiple, you need the expansion of usage-based pricing, but the predictability of subscriptions. The data supports this: pure usage adoption has actually cooled slightly (from 46% to 41% in some indices) as companies pivot toward hybrid models to protect their valuation floor during economic stabilization.

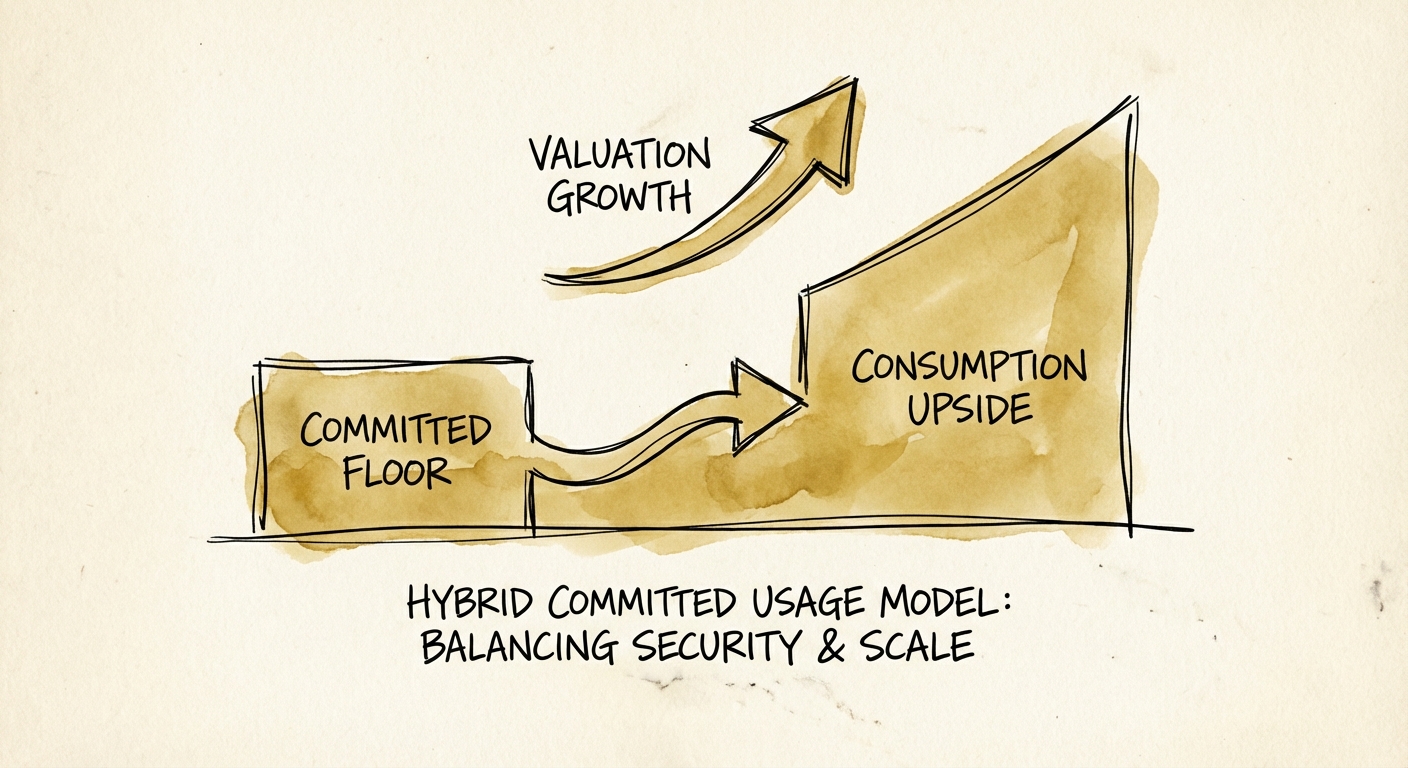

The Hybrid "Gold Standard": Structuring for an 8x Exit

The solution to the predictability paradox is the Hybrid Committed Model. This is the valuation-maximizing structure for 2026. Instead of charging purely in arrears (pay-as-you-go), high-value exits are built on "Committed Usage" contracts with a "Drawdown" mechanic.

The Winning Structure

- The Floor (Commitment): The customer commits to $100k of usage annually, paid upfront or quarterly. This satisfies the PE requirement for recognized recurring revenue and predictability.

- The Upside (Overage): Usage above the committed floor is billed at a premium rate, or triggers an early renewal/upsell conversation. This drives the NRR expansion that strategic buyers crave.

By shifting to this model 12-24 months before an exit, you convert "volatile utility revenue" into "high-quality ARR." Benchmarks show that strategic acquirers value this specific type of consumption revenue up to 50% higher than standard subscription revenue because it proves the product is mission-critical. If usage drops, the commitment protects you; if usage grows, your multiple expands. This is the only way to capture the consumption premium without suffering the volatility discount.