The practical answer

- Short answer

- Why vertical SaaS companies command higher exit multiples than horizontal generalists. New 2026 data on CAC efficiency, NRR, and PE buyout trends.

- Best fit

- Industry: Software / SaaS. Function: Strategy & Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- $200 vs $2,500 The dramatic difference in Customer Acquisition Cost (CAC) between vertical specialists and broad horizontal platforms.

The Generalist Discount vs. The Vertical Moat

For the last decade, the venture capital playbook was dominated by the "Total Addressable Market" (TAM) obsessed narrative. Founders were encouraged to build horizontal platforms—project management tools for everyone, CRMs for any sales team, communication apps for every office. The logic was simple: bigger market, bigger outcome. In 2026, that logic is demonstrably false for the vast majority of exits.

We are witnessing a bifurcation in valuation multiples. According to October 2025 market data, while horizontal SaaS valuations face wide dispersion (with sectors like AdTech trading as low as 1.1x revenue), premium vertical players in sectors like automotive and industrial software are commanding median multiples of 4.3x to 5.5x. The reason is not market size; it is market efficiency.

The data is stark: Vertical SaaS companies are currently seeing 40-50% greater sales efficiency than their horizontal counterparts. While a generalist project management tool might spend $1,200 to $2,500 to acquire a customer (CAC) through broad, expensive digital advertising, a vertical-specific solution (e.g., project management for commercial construction) acquires customers for as little as $200 to $300. In a capital-constrained environment, private equity buyers are no longer paying for the potential of a massive TAM; they are paying a premium for the predictability of a captured niche.

Horizontal SaaS casts a wide net; Vertical SaaS uses a spear. In 2026, buyers are paying for the spear.

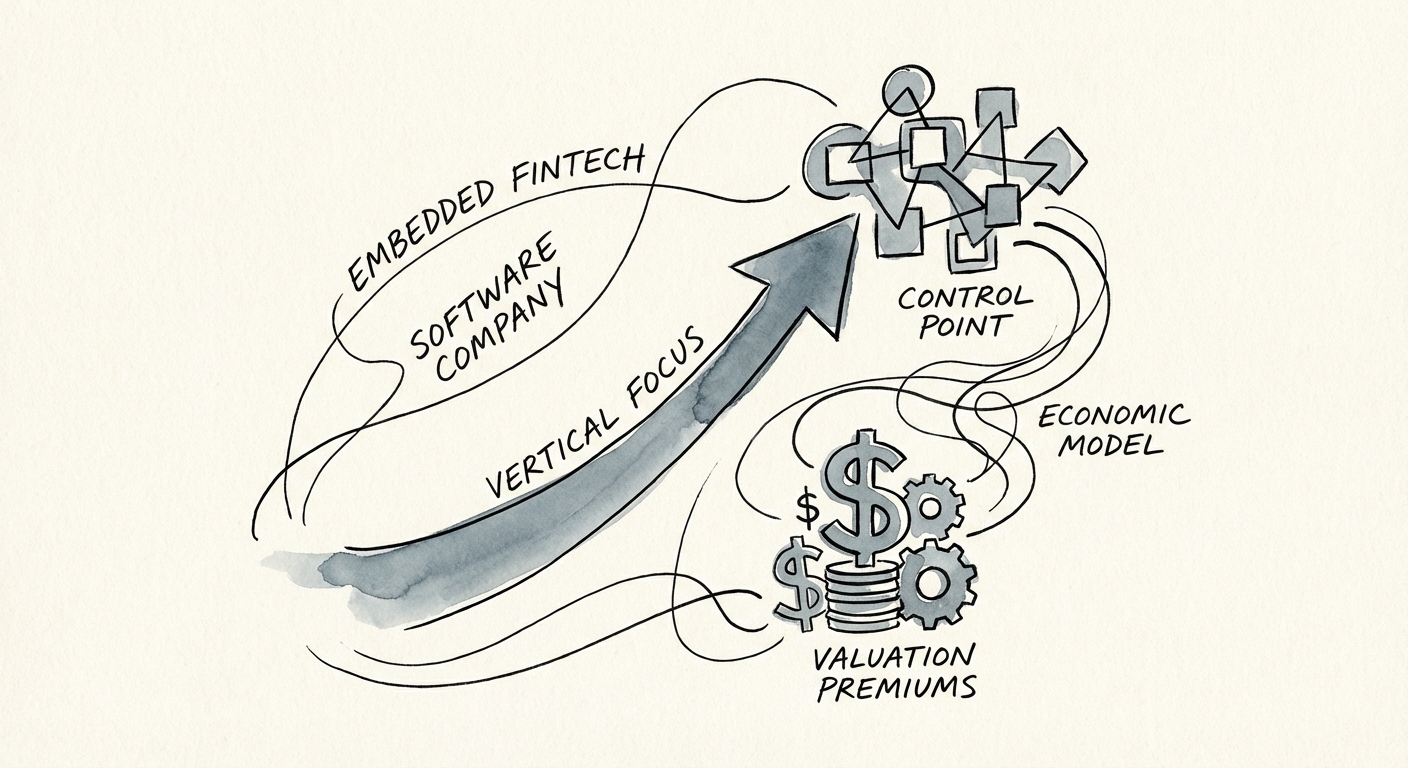

The "Control Point" Economics

The valuation premium for vertical software isn't just about cheaper acquisition; it's about the depth of the revenue stack. Horizontal tools are often treated as discretionary line items—easily swapped for a cheaper competitor. Vertical platforms, however, become the "operating system" of the business, creating a defensive moat that drives significantly higher Net Revenue Retention (NRR).

This "stickiness" allows vertical players to execute a multi-product strategy that horizontal competitors cannot match. By 2025, 59% of vertical SaaS companies had successfully launched more than one product, often embedding fintech, payments, or payroll directly into the workflow. This transforms a simple SaaS subscription into a transaction-based revenue engine.

The Multi-Product Multiplier

Consider the difference in exit math. A horizontal CRM with $10M ARR growing at 15% might trade at 3x revenue due to high churn and competitive pressure. A vertical CRM for dental practices with the same $10M ARR—but with embedded payments and patient financing—often commands a 6x to 8x multiple. Why? Because the "Control Point" dynamics mean that customer is not just using software; they are running their entire financial life through the platform. The churn risk is effectively zero, and the expansion revenue potential is uncapped.

The Exit Reality: Depth Beats Breadth

For founders looking to exit in the next 18 to 24 months, the strategic imperative is to stop widening the aperture and start deepening the hook. Private equity firms are currently allocating 44% of their software deal flow specifically to vertical market leaders. They are actively hunting for "systems of record" in unsexy industries—hvac, legal, logistics, and healthcare—where AI disruption is lower and customer durability is higher.

If you are currently positioning your company as a "tool for everyone," you are likely positioning yourself for a discount. The market has shifted from rewarding the breadth of your vision to rewarding the depth of your grip. To maximize your exit multiple, you must demonstrate that you are not just a vendor, but the inevitable infrastructure of your specific industry.