The practical answer

- Short answer

- Why adding Azure and GCP might reduce your exit value multiple. Benchmarks on the 'Generalist Discount' vs. the 'Specialist Premium' for AWS Partners in 2026.

- Best fit

- Industry: Cloud Services / System Integrators. Function: Strategy & Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- $7.13 Revenue generated for partners per $1 of AWS sold (Specialized)

The Multi-Cloud Hallucination: Why "More TAM" Equals Less Value

There is a dangerous slide in your Board deck right now. It’s likely titled "Strategic Growth: Multi-Cloud Expansion." The logic seems sound: your clients use AWS and Azure, so why leave money on the table? If you capture the Azure spend, you double your Share of Wallet. In the spreadsheet, this looks like revenue growth. In the data room, it looks like a lack of conviction.

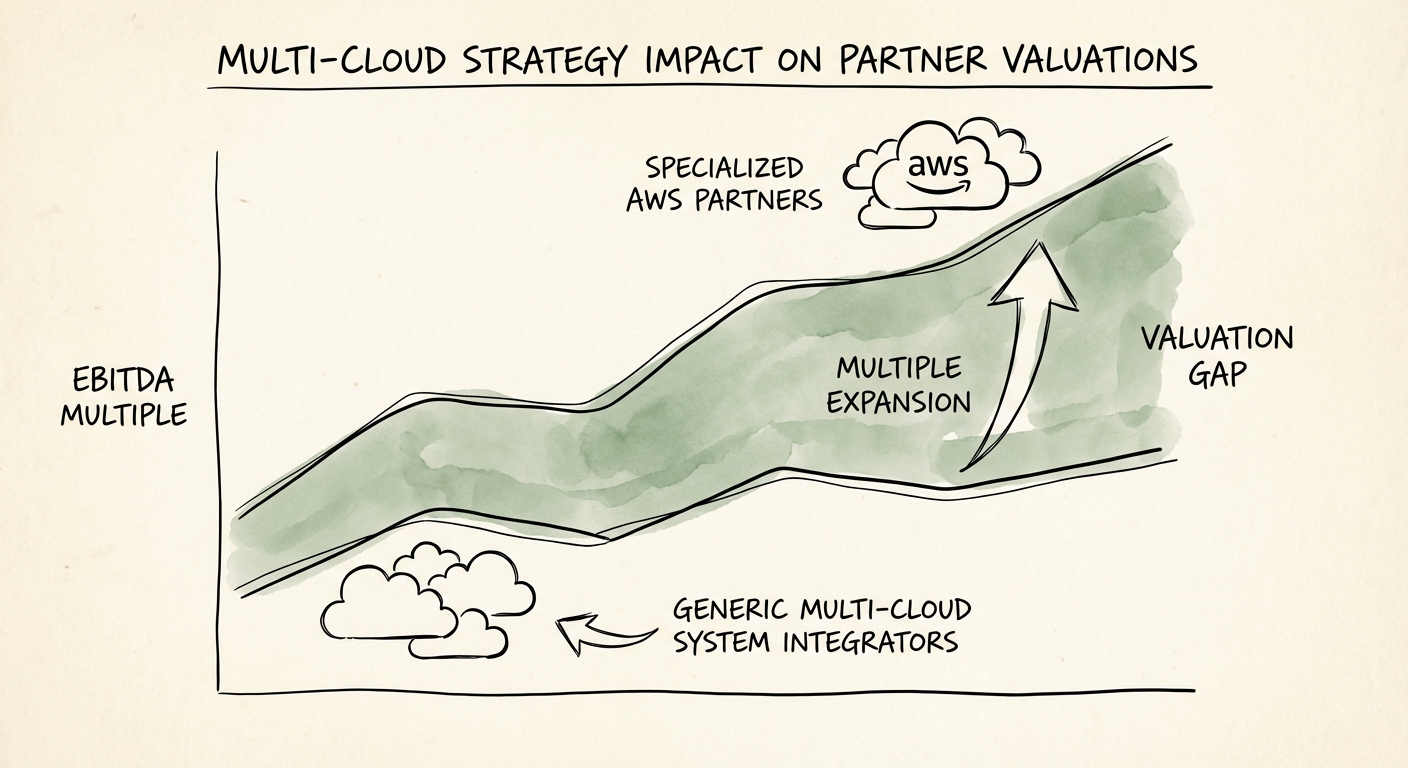

As we analyze 2025-2026 valuation trends for IT Services, a harsh reality has emerged for mid-market firms ($20M–$100M revenue). Specialization is trading at a premium; generalization is trading at a discount. The "Generalist Discount" for shops offering generic support across AWS, Azure, and GCP is currently averaging 2.5x to 4.2x turns of EBITDA lower than their specialized counterparts.

The Economics of Dilution

Why do PE buyers punish the "one-stop-shop"? Because multi-cloud complexity destroys unit economics unless you are at massive scale (>$500M revenue). When a $30M AWS shop adds an Azure practice, three things typically happen to the P&L:

- Utilization Drag: Engineers cannot effectively context-switch between CloudFormation and ARM templates without a 15% productivity loss. Your blended utilization drops from a healthy 74% to a dangerous 66%.

- Sales Friction: Your differentiator becomes diluted. Instead of being the "Data on AWS" experts, you become "Just another IT vendor." Win rates drop as you compete against specialists on every front.

- Margin Erosion: Maintaining two distinct sets of Premier/Expert competencies requires duplicate overhead in partner management, training, and certifications.

Investors aren't buying your ability to say "Yes" to every RFP. They are buying your ability to command pricing power. You cannot command pricing power in a commodity market, and "General Cloud Support" is the ultimate commodity.

You cannot command pricing power in a commodity market, and 'General Cloud Support' is the ultimate commodity. EBITDA doesn't care about your 'capabilities' slide. It cares about your utilization.

The $7.13 Multiplier: Why Depth Beats Width

The smartest capital in the room is looking for what I call "Ecosystem Leverage." According to the 2025 Omdia and AWS Partner study, specialized partners generate up to $7.13 in services revenue for every $1 of AWS consumed. This is the new "Golden Ratio" for valuation.

Compare this to the "Generalist" ratio, which hovers closer to $3.50. The difference? IP and High-Value Workloads.

The "Focused Partner" Advantage

Data from the 2025 partner ecosystem shows that "Focused Partners" (those with deep competencies in specific workloads like GenAI, Migration, or Security) are seeing opportunity growth outpace generic multi-category partners by substantial margins. But the real story is in the quality of that revenue.

A PE buyer looks at a $5M EBITDA AWS Specialist and sees a platform for "Bolt-on" acquisitions. They look at a $5M EBITDA Multi-Cloud Generalist and see a "Fixer-Upper" with fragmented processes.

The Valuation Gap by the Numbers:

- Generic Managed Services (Multi-Cloud): Trading at 6x - 8x EBITDA. This is priced as "Staff Augmentation."

- Specialized Ecosystem Leader (Single Cloud Depth): Trading at 10x - 14x EBITDA. This is priced as "Strategic IP."

If you are doing $5M in EBITDA, that "Strategic Multi-Cloud" decision might be costing you $20M in Enterprise Value at exit. You are effectively paying a $20M tax for the privilege of struggling to manage two different partner portals.

How to Execute Multi-Cloud Without Killing Your Exit

Does this mean you should never go multi-cloud? No. But you must stop treating it as a "Cross-Sell" and start treating it as a "Business Unit." If your Portfolio Company is pushing for multi-cloud, here is the Operating Partner's Guide to doing it without destroying value.

1. The "Pillars, Not Pools" Rule

Do not create a blended resource pool. If you launch Azure, it must be a distinct P&L with its own Practice Leader, its own dedicated bench, and its own utilization targets. If I see a "Cloud Engineer" on your org chart who is expected to do Terraform for AWS in the morning and Bicep for Azure in the afternoon, I know your margins are masking the underlying economics.

2. Target "High-Value Intersections" Only

Don't resell generic compute on both. Specialize by function. Be the "AWS Data & AI" shop and the "Azure Corporate IT & Identity" shop. This minimizes competitive overlap and justifies high rates in both. The 2025 valuation trends clearly favor firms that own a problem domain (e.g., "Secure Identity") rather than just an infrastructure domain.

3. The "Partner Margin" Test

Before you sign that partnership agreement with Google or Microsoft, calculate the fully loaded cost of compliance. The "Gold/Premier" bar is rising every year. If the new practice cannot generate at least $5M in ARR within 18 months, the overhead of maintaining the partnership status will eat the margin contribution of the first $3M entirely. You are eroding margin just to put a logo on your website.

Summary: Pick Your Lane or Build Two Highways

The market does not pay for optionality; it pays for outcome certainty. A deep, 200-person AWS practice with 10 competencies is a scarce asset. A 100-person shop split 50/50 between AWS and Azure is a commodity. Choose your strategy based on the multiple you want, not just the revenue you think you can catch.