The practical answer

- Short answer

- Why technical HubSpot consultancies trade at 12x EBITDA while marketing agencies stall at 5x. A guide for PE Operating Partners on the 2026 'Enterprise Expansion Premium'.

- Best fit

- Industry: Private Equity / Tech Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x Target EBITDA multiple for 'Enterprise Architecture' HubSpot partners, compared to 5x for marketing agencies.

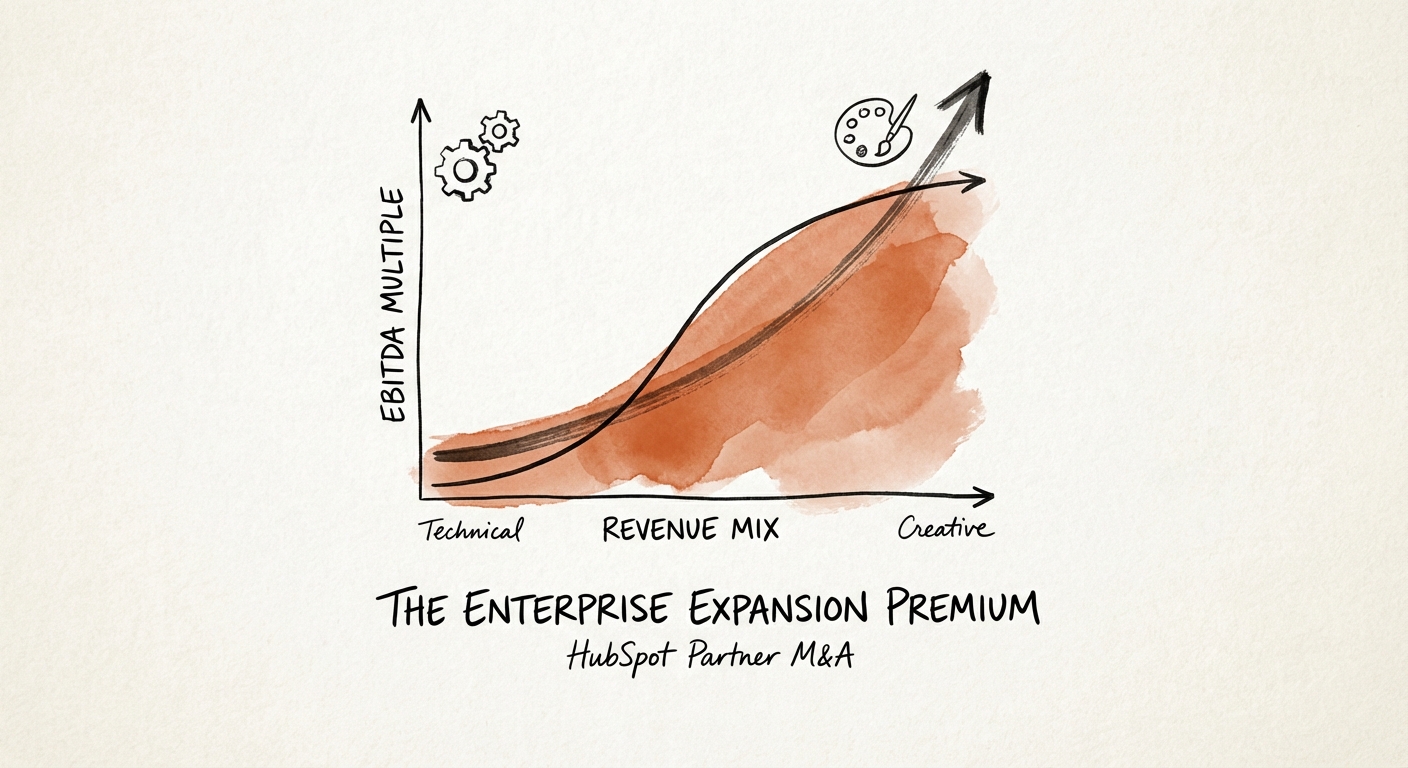

The Valuation Bifurcation: Why 'Creative' is a Commodity and 'Technical' is Gold

In 2026, the HubSpot ecosystem is no longer a monolith of inbound marketing agencies. It has bifurcated into two distinct asset classes with drastically different valuation profiles. If you are holding a portfolio company that primarily sells content retainers and blog management, you are sitting on a 4x to 6x EBITDA asset. You own a service business with low barriers to entry and high client churn.

However, if you own a firm that architects multi-hub migrations (Marketing + Sales + Service + Ops) for mid-market enterprises, you are holding a potential 10x to 14x EBITDA asset. This is the 'Enterprise Expansion Premium.'

The market data is clear. According to PwC’s 2025 Global M&A Outlook, while general marketing services valuations have softened due to AI automation fears, technical transformation consultancies have seen multiple expansion. Buyers—specifically private equity sponsors executing consolidation plays—are paying premiums for partners who own the data layer rather than just the creative layer. Why? Because you can fire your blog writer tomorrow, but you cannot rip out the team that integrated your CRM with your NetSuite ERP.

The 'Agency' vs. 'Consultancy' Trap

Many PE operating partners fail to distinguish between these two models until they hit the market. They see "HubSpot Elite Partner" and assume a premium exit. But buyers drill down into the revenue mix immediately. If your revenue is 80% creative services (email templates, social media, blogging) and 20% technical (implementation, integration), you will be valued as an agency. Your goal over the next 18 months must be to flip that ratio. Marketing agency valuations are notoriously capped because creative work is hard to scale and easy to churn.

You can fire your blog writer tomorrow, but you cannot rip out the team that integrated your CRM with your ERP. That is the difference between a 4x and a 12x exit.

The 'Ops Hub' Moat: The New Metric for Stickiness

The single biggest driver of the Enterprise Expansion Premium is the deployment of HubSpot Operations Hub (Ops Hub) and complex data orchestration. In the SMB days, HubSpot was a marketing island. Today, in the enterprise, it is a connected ecosystem. The partners trading at premium multiples are those leveraging Ops Hub to build permanent bridges between HubSpot and the rest of the enterprise stack (Snowflake, NetSuite, SAP).

We call this the 'Integration Density' metric. A customer with HubSpot isolated to the marketing department has a churn risk of moderate to high. A customer where HubSpot is bi-directionally syncing deal data with the ERP, ticket data with the product platform, and usage data with the data warehouse has near-zero churn. Unlike Salesforce partners who often struggle with massive customer concentration, elite HubSpot partners can build a diverse, sticky base by becoming the 'data traffic controllers' for their clients.

HubSpot's own Q3 2025 financial results highlight this shift, with enterprise revenue growing at over 20% YoY and multi-hub adoption becoming the standard for their upmarket push. If your portfolio company isn't selling Ops Hub with every deal, they are leaving enterprise value on the table. The ability to audit a mess of legacy data, clean it, and structure it for a friction-less migration is what justifies $150k+ initial contract values (ACV) compared to the $15k retainers of the past.

The Exit Roadmap: Converting Creative Revenue to Technical Equity

To capture the Enterprise Expansion Premium by 2027, you need to execute a rigorous transformation of your portfolio company's revenue architecture. Stop measuring 'retainer renewals' and start measuring 'Net Revenue Retention (NRR)' based on cross-hub expansion.

1. The Talent Pivot: Stop hiring generalist account managers. Start hiring Solution Architects and Data Engineers. The 'talent war' in the HubSpot ecosystem has shifted from creative strategists to technical resources who understand API endpoints and data schemas. Technical debt is a deal killer; your team needs the skills to fix it, not just work around it.

2. The 'Land and Expand' Fallacy: In the agency world, 'expand' meant selling more blog posts. In the premium consultancy world, 'expand' means activating Service Hub or Commerce Hub. Your sales compensation plans must be rewired to incentivize multi-hub adoption, not just service hours. A client using 4 Hubs is worth 3x the enterprise value of a client using 1 Hub, even if the MRR is identical, because the quality and durability of that revenue is superior.

3. Documentation as Intellectual Property: Value isn't just in the people; it's in the playbook. Premium exits happen when you can demonstrate a proprietary methodology for 'Enterprise Onboarding' that reduces time-to-value. If your delivery relies on heroics, you have a job, not a company. If it relies on a documented, repeatable 60-day migration sprint, you have a platform worth acquiring.

According to Founders Advisors' 2025 MarTech M&A Report, buyers are aggressively filtering for this 'productized service' capability. They want to see that you can take a Series C SaaS company and migrate them from Salesforce to HubSpot with zero downtime. That is the capability that commands the premium.