The practical answer

- Short answer

- Why MuleSoft and Salesforce integration partners command 12x+ EBITDA multiples while generalist dev shops struggle at 5x. A valuation guide for IT services founders.

- Best fit

- Industry: B2B Tech Services. Function: Corporate Strategy & M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Target EBITDA multiple for specialized MuleSoft/Salesforce partners, compared to 5x for generalist IT staffing.

The Tale of Two Term Sheets: Body Shop vs. Strategic Partner

If you put two IT services firms with identical P&Ls side-by-side, the market will value them differently based entirely on what they sell, not just how much they sell. Let’s look at the math that frustrates every generalist founder I meet.

Firm A is a generalist software development shop. They have $10M in revenue, $2M in EBITDA, and a bench of talented Java and Python developers. They solve whatever problem the client throws at them. In the eyes of a Private Equity buyer, Firm A is a staffing agency with better marketing. They trade at 4x to 6x EBITDA. Their exit value is $8M–$12M.

Firm B is a MuleSoft implementation partner. They also have $10M in revenue and $2M in EBITDA. But they don't sell "developers"; they sell enterprise connectivity. They hold MuleSoft certifications and have a library of reusable APIs. In the eyes of that same PE buyer, Firm B is a strategic platform play. They trade at 10x to 14x EBITDA. Their exit value is $20M–$28M.

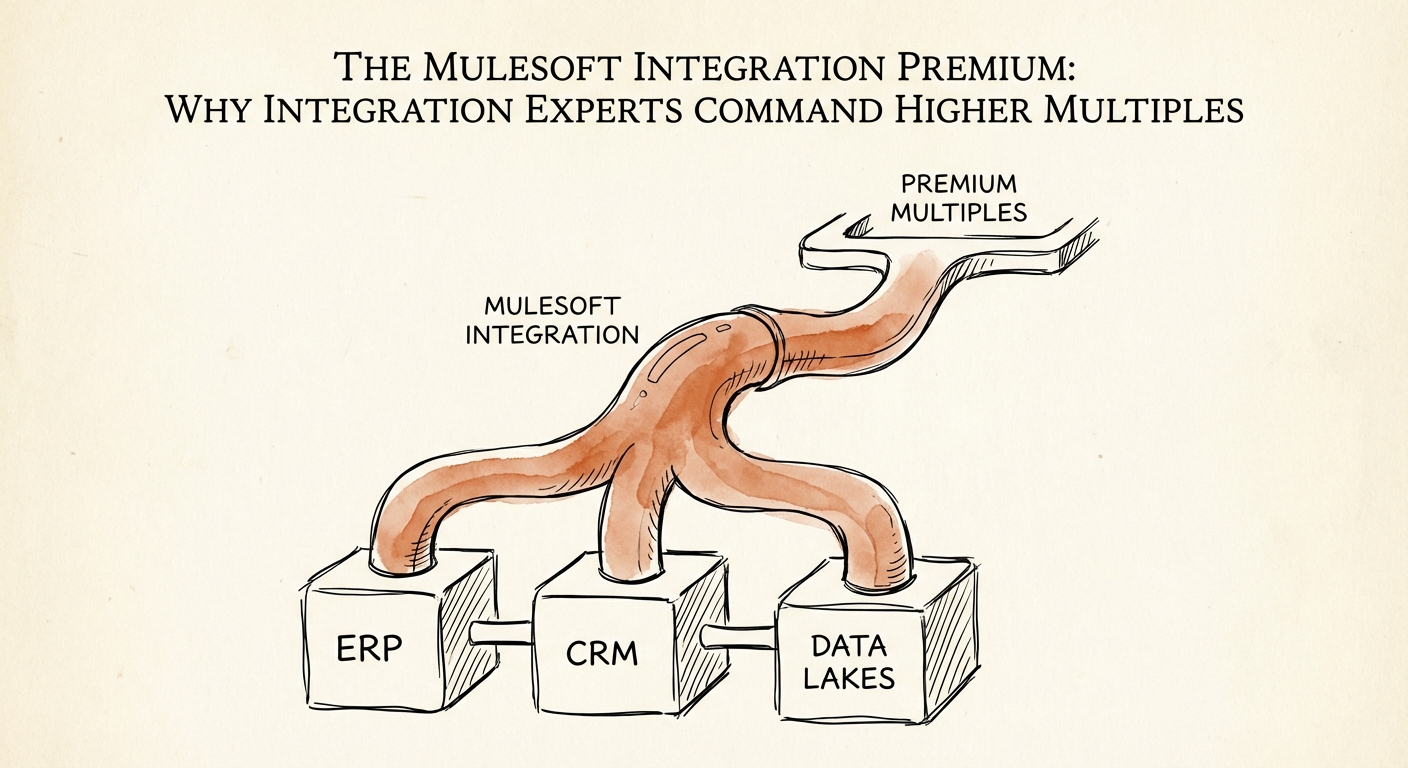

The difference is not margin; it’s moat. Generalist code is transient. If a client fires Firm A, they hire another dev shop tomorrow. But MuleSoft is the plumbing of the enterprise. It connects the ERP to the CRM to the Data Lake. Ripping out Firm B doesn’t just stop a project; it breaks the company's nervous system. That stickiness commands the premium.

Generalist code is transient. If a client fires you, they hire another dev shop tomorrow. But integration is the plumbing. Ripping out a MuleSoft partner doesn’t just stop a project; it breaks the company's nervous system. That stickiness commands the premium.

Why the "Plumbing" Pays: The Economics of Integration

The valuation gap exists because "Digital Transformation" has stalled, and integration is the bottleneck. Companies have bought the SaaS tools (Salesforce, ServiceNow, Workday), but they can't get them to talk to each other. This reality has shifted the power dynamic in M&A.

According to 2025 market data, specialized partners in the Salesforce ecosystem (which includes MuleSoft) are seeing valuations decouple from the broader IT services market. While generalist firms face compression due to AI efficiency fears, integration partners are insulated. Why? Because AI doesn't work without clean, connected data pipelines. You are no longer just a service provider; you are the enabler of the acquirer's entire AI thesis.

The Three Drivers of the MuleSoft Premium:

- High Barrier to Entry: You can't fake a MuleSoft practice. The certification path for Architects and Developers is rigorous. This creates a supply constraint that drives bill rates 30-40% higher than generalist engineering roles ($225+ vs. $160/hr).

- Reusable IP (The Asset Test): Buyers pay for assets, not hours. A mature MuleSoft shop has a library of "Anypoint Connectors" and pre-built API templates. This allows you to deliver faster with higher margins, breaking the linear relationship between revenue and headcount.

- Managed Connectivity as ARR: Unlike project-based dev work, integration requires constant monitoring. This allows specialized firms to sell "Managed Integration Services"—multi-year, recurring revenue contracts that look and smell like SaaS to an investor.

If you are running a generalist shop, you are leaving 50% of your enterprise value on the table by ignoring specialization. Read more about IT Services M&A valuation trends to see where your firm fits.

How to Pivot: From Body Shop to Integration Powerhouse

You don't need to fire your engineering team to capture this premium, but you do need to re-architect your go-to-market strategy. The transition from "Staff Augmentation" to "Solution Partner" is painful but necessary for a Series B or C exit.

1. Stop Selling Hours, Start Selling "Connectors"

Audit your revenue mix. If 80% of your revenue comes from "time and materials" staffing, you are capped at a 5x multiple. You must package your expertise. Instead of "200 hours of development," sell a "Fixed-Price NetSuite-to-Salesforce Integration Accelerator." This shifts the risk (and the margin upside) to you.

2. The Certification Factory

Your bench needs credentials. A "Senior Java Developer" is a commodity. A "Certified MuleSoft Platform Architect" is a rare asset. Aggressively invest in certifying your existing team. This immediately raises your blended bill rate and signals to acquirers that your talent is defensible. Review our guide on pricing services for acquisition to understand how this impacts your EBITDA adjustments.

3. Document the "Plumbing"

The biggest killer of service firm deals is "Tribal Knowledge." If your integration logic lives in your CTO's head, it's worthless to a buyer. You must document your methodologies. Create standard operating procedures (SOPs) for API lifecycle management. This turns your service into a productized offering.

The market is screaming for integration. The technical debt created by disconnected SaaS tools is massive. By positioning yourself as the expert who solves this specific, high-value problem, you stop competing on price and start competing on value. That is how you double your exit multiple.