The practical answer

- Short answer

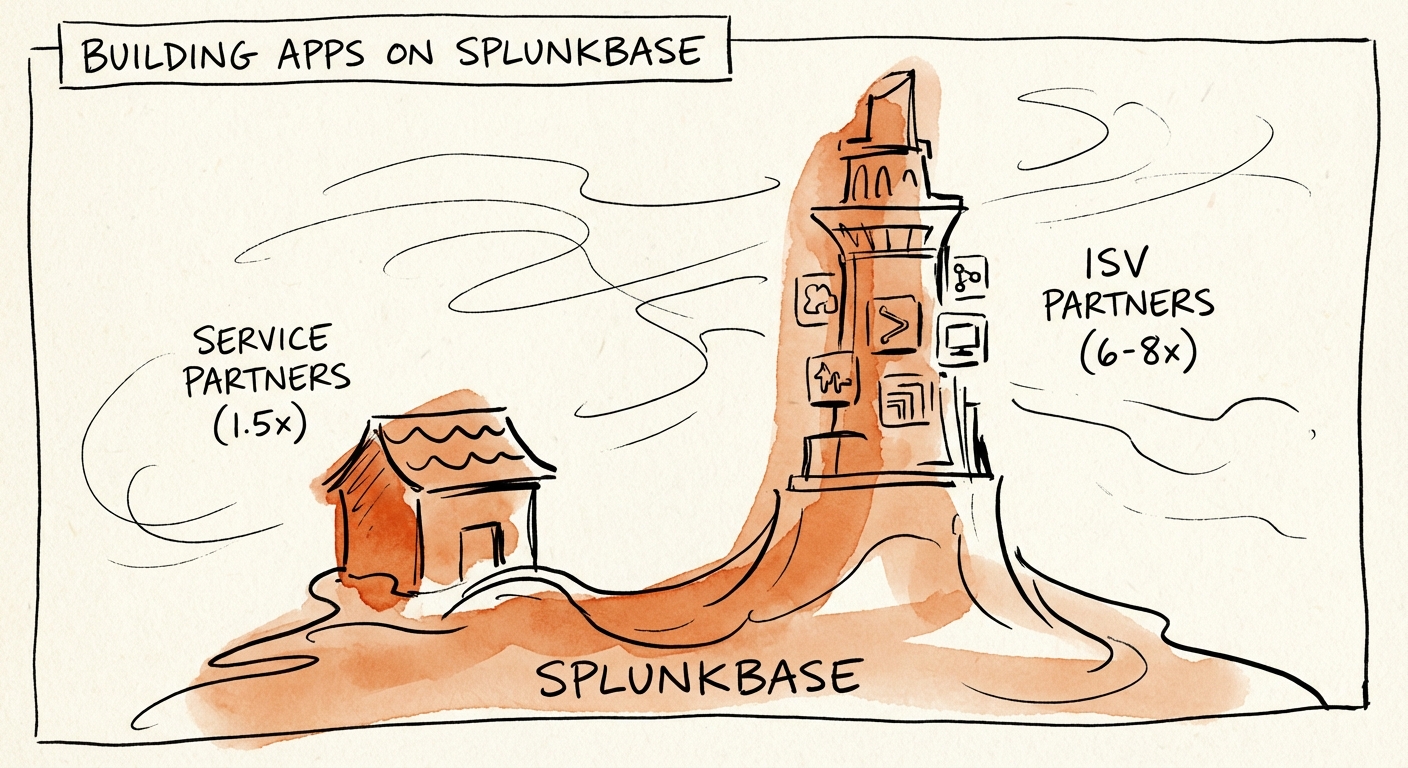

- Building a Splunk app can shift your valuation from 1.5x to 8x revenue. Discover the ISV strategy, Cisco acquisition impact, and 2026 benchmarks for Splunkbase success.

- Best fit

- Industry: Cybersecurity & Observability. Function: Product Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 6.2x Revenue multiple for specialized Data Infrastructure ISVs in 2025, compared to 1.2x for Services.

The Cisco Vacuum: Why Splunk ISVs Are Trading at 8x Revenue

In March 2024, Cisco completed its $28 billion acquisition of Splunk, effectively validating the 'Data-to-Everything' platform as the operating system for enterprise security and observability. For services partners, this event signaled a fork in the road. While traditional professional services firms (SIs) and MSPs continue to trade at 6x-10x EBITDA (roughly 1.2x to 1.5x revenue), partners who have successfully pivoted to the 'Build' track—developing certified apps on Splunkbase—are commanding valuations closer to 6.2x to 8x revenue.

This 'valuation gap' exists because PE buyers and strategic acquirers (including Cisco itself) are no longer looking for 'body shops' that implement Splunk. They are hunting for IP-led partners that solve the 'last mile' data ingestion and visualization problems that the core platform cannot address. Specifically, the integration of Splunk Partnerverse into the Cisco 360 Partner Program (slated for February 2026) has created a scarcity of 'specialized IP' capable of bridging legacy Cisco infrastructure with modern Splunk observability.

The 'Service-to-IP' Arbitrage

The math behind this pivot is compelling. A $10M services firm with 20% EBITDA ($2M) might sell for $16M (8x EBITDA). However, if that same firm generates $3M of its revenue from a high-retention Splunkbase app (ARR), that specific revenue stream could be valued at $18M (6x Revenue) alone, potentially doubling the total enterprise value. The strategic goal for 2026 is not to abandon services, but to use them as the funding engine for this high-value IP.

The combination of Cisco and Splunk has created a vacuum for specialized ISVs. The acquirers we talk to aren't looking for more implementation capacity; they are paying 8x revenue for partners who own the 'last mile' of data integration.

The 2026 Splunkbase Diagnostic: Utility vs. Platform

Not all Splunk apps are created equal. In our analysis of M&A activity within the ecosystem, acquirers distinguish sharply between 'Utility Apps' and 'Platform Extensions.'

1. Utility Apps (Valuation Neutral)

These are typically free connectors or basic dashboards uploaded to Splunkbase to generate leads. While they drive service pipeline, they possess no intrinsic transferable value. They suffer from:

- Zero ARR: They are given away for free.

- Low Barrier to Entry: Competitors can replicate them in a week.

- Maintenance Debt: They consume engineering resources without direct monetization.

2. Platform Extensions (Valuation Drivers)

These are 'Premium' or 'Built for Splunk' certified apps that charge a license fee (often via AWS Marketplace or direct paper). They trade at premium multiples because they feature:

- Data Gravity: They ingest unique data (e.g., proprietary IoT protocols, niche healthcare logs) that makes ripping out Splunk impossible.

- Workflow Stickiness: They don't just visualize data; they trigger actions (SOAR) or compliance reporting that business users rely on daily.

- Cisco Synergy: They align with Cisco’s new focus on AI-driven observability, filling gaps in the AppDynamics/Splunk integration.

Recent market data indicates that infrastructure SaaS companies—the closest proxy for Splunk ISVs—are trading at a median of 6.2x NTM revenue, whereas traditional MSPs struggle to break 1.5x revenue. This 4-turn spread is the 'IP Premium' available to partners who execute the pivot correctly.

Execution: The Path to 'Built for Splunk' Status

To capture this premium, partners must navigate the Splunk Partnerverse 'Build' track with precision. The days of 'launch and forget' are over. M&A due diligence now scrutinizes the technical health and market fit of your app.

The 'Badged' Requirement

Acquirers look for the 'Splunk Cloud vetted' and 'Built for Splunk' badges. These are not just marketing assets; they are technical proofs of transferable quality. An app without these badges is considered a liability (technical debt) rather than an asset. In 2026, with the Cisco integration, ensuring your app is compatible with both Splunk Enterprise and Splunk Observability Cloud is non-negotiable.

Monetization Strategy: The Marketplace Wedge

The most successful ISVs are bypassing direct sales and leveraging the AWS Marketplace or Cisco SolutionsPlus programs. By listing your Splunk app as a transactable offer, you allow customers to burn down their committed cloud spend (MACC/EDP) to buy your software. This reduces sales friction by 40% and positions your firm as a strategic partner to the cloud hyperscalers—further increasing your attractiveness to PE buyers.

Don't build a 'better dashboard.' Build a connector for a high-value, underserved data source (e.g., manufacturing OT data, specialized fintech logs) and charge for the ingestion value, not the visualization.