The practical answer

- Short answer

- New data on Google Cloud Partner valuations. Why specialized Data & GenAI firms trade at 12x-15x EBITDA while infrastructure generalists stall at 6x. M&A benchmarks for 2026.

- Best fit

- Industry: Cloud Consulting & IT Services. Function: M&A & Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

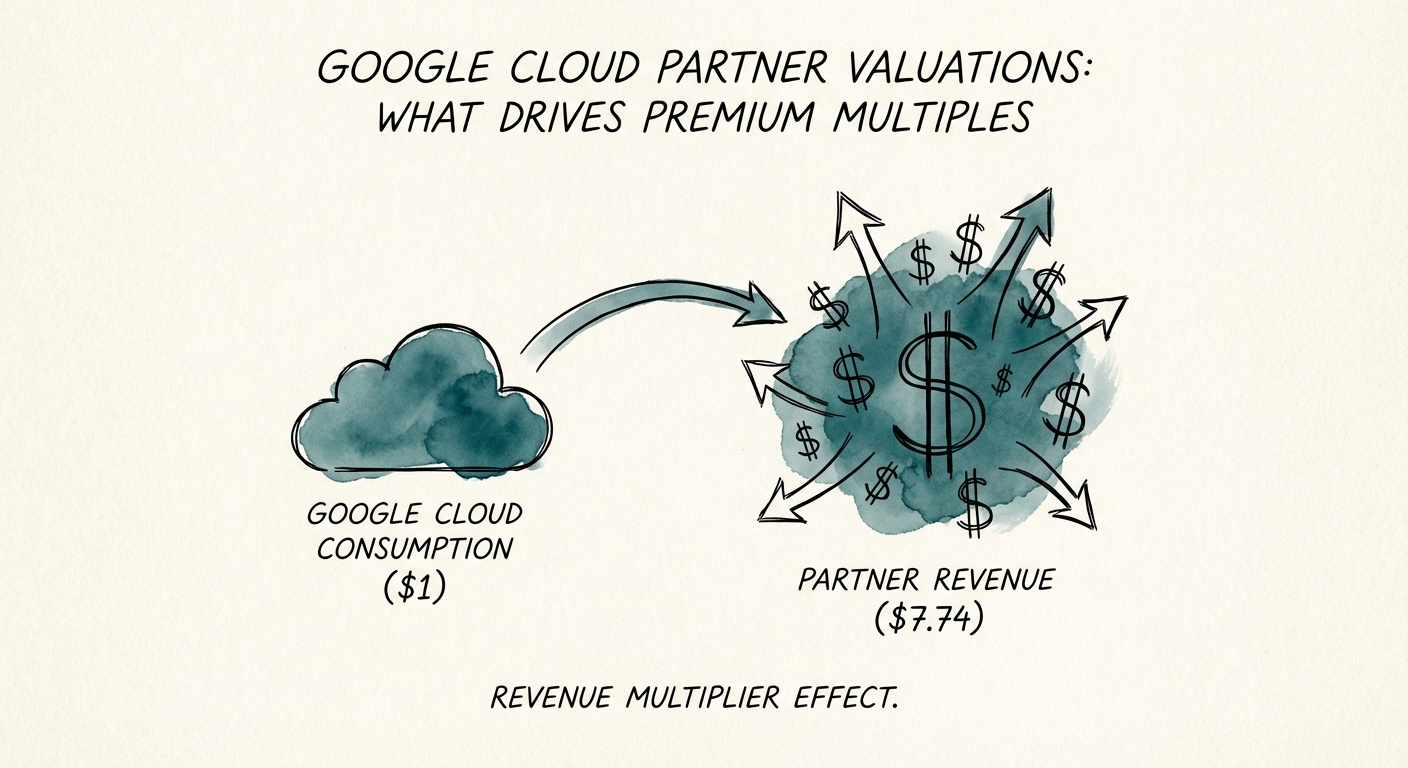

- $7.74 Partner revenue generated for every $1 of Google Cloud sold (IDC Forecast)

The Great Bifurcation: Why "Google Cloud Partner" Is No Longer a Valuation Class

For years, Private Equity viewed the entire Google Cloud Platform (GCP) ecosystem as a monolithic "growth bet." If you had the badges, you got the multiple. That era is over. As we move into 2026, the valuation landscape for GCP partners has fractured into two distinct asset classes with radically different economic profiles.

On one side, we see the Generalist Infrastructure Shops. These firms focus on "lift and shift" migrations, compute resale, and basic implementation. While they often boast high top-line revenue driven by pass-through cloud spend, their gross margins hover in the 25-35% range. In the current M&A market, these assets are trading at 5x-7x EBITDA. They are viewed as commodities—necessary plumbing with low switching costs and high labor intensity.

On the other side are the Data & GenAI Specialists. These firms have pivoted away from low-margin infrastructure resale to focus on high-margin workflows: BigQuery modernization, Vertex AI integration, and proprietary industry solutions. Their gross margins often exceed 50%, and their revenue is sticky because it is embedded in the client's competitive advantage, not just their server room. Consequently, these firms are commanding 12x-15x EBITDA multiples, with strategic acquirers occasionally paying even higher for specific IP.

The "Resale Trap" in Due Diligence

For PE Operating Partners, the most dangerous metric in a GCP partner's CIM is "Gross Revenue" that includes low-margin license resale. I recently reviewed a target boasting $50M in revenue, but $35M of that was pass-through GCP consumption with a razor-thin 3% margin. The real business was a $15M services firm struggling to break even. If you value that company on a revenue multiple—or even a blended EBITDA multiple—you are overpaying for empty calories. The market now strips out resale margin almost entirely, valuing the pure-services EBITDA.

Stop looking at revenue multiples. Your 3x revenue shop is actually a 6x EBITDA shop if you don't fix the gross margin mix. The market pays for IP and high-margin services, not pass-through consumption.

The Three Drivers of the 15x Premium

What specifically pushes a partner from the 6x bucket to the 14x bucket? Our analysis of recent M&A activity and ecosystem data identifies three non-negotiable value drivers.

1. The "Multiplier" Economy: Beyond $1 for $1

The most sophisticated buyers are looking for partners who unlock the "ecosystem multiplier." According to IDC data, partners are now generating upwards of $5.49 to $7.74 in their own revenue for every $1 of Google Cloud technology they sell. This ratio is the litmus test for specialization. A partner generating only $2 for every $1 of consumption is a reseller with a services arm. A partner generating $7 is a strategic consultant leveraging the cloud to sell high-value IP and transformation. The latter commands the premium.

2. Marketplace Transactions as a Valuation Proxy

The Google Cloud Marketplace has evolved from a procurement tool to a valuation signal. Partners who transact significantly through the Marketplace are seeing 32% larger deal sizes and accelerated sales cycles. Why does this matter for valuation? Because it proves alignment. It shows the partner is embedded in the hyperscaler's own go-to-market motion, reducing customer acquisition costs (CAC) and increasing the likelihood of "co-sell" support from Google's own sales force. In due diligence, we now look at "Marketplace Attributable Revenue" as a proxy for the defensibility of the pipeline.

3. From "AI Experimentation" to "Production Revenue"

Every partner claims to do GenAI. The valuation premium belongs to those who have moved clients from sandbox to production. With 74% of organizations now reporting ROI from GenAI investments, buyers are scrutinizing the quality of AI revenue. Is it one-off "Proof of Concept" (POC) revenue, which is volatile and project-based? Or is it recurring "Managed AI" revenue, where the partner manages the models, the data pipelines (Dataflow/BigQuery), and the compliance layer? The former is worth 1x revenue; the latter is the engine of multiple expansion.

The Operator's Playbook: Grooming the Asset for Exit

If you are holding a GCP partner portfolio company today, your goal is to migrate revenue quality before you go to market. You cannot simply "grow" your way to a higher multiple if the growth is coming from low-margin resale or commoditized labor.

Fix the Margin Mix

Stop incentivizing your sales team on "Total Contract Value" (TCV) that is bloated with resale dollars. Shift the compensation plan to reward Services Gross Margin and Proprietary IP Revenue. We often see firms where 60% of the sales comms go to deals that generate 10% of the profit. Realigning this can improve your blended EBITDA margin by 400-500 basis points in 12 months, directly impacting your exit valuation.

The "Specialization" Pivot

Generalist "Premier Partners" are a dime a dozen. The badge no longer differentiates. To exit at a premium, you must narrow the aperture. Become the Google Cloud partner for Retail Analytics, or the partner for Financial Services Compliance on GCP. This verticalization allows you to productize your delivery (increasing margins) and creates a scarcity premium. A strategic buyer (like a global GSI) isn't buying capacity; they are buying a capability they cannot easily build. If you are just "smart people for rent," you will trade at a services multiple. If you are a "vertical solution platform," you trade like a tech company.

Ultimately, the difference between a 6x exit and a 14x exit isn't just growth—it's revenue composition. You need to speak fluent EBITDA to the buyers, but you need to speak fluent DevOps and Data Strategy to build the value.