The practical answer

- Short answer

- Building on ServiceNow App Engine? Learn the valuation multiples, exit risks, and strategic benchmarks for 'Built on Now' ISVs in 2026.

- Best fit

- Industry: B2B SaaS / Enterprise Software. Function: Corporate Strategy / M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- CAC Buyers will compare customer acquisition efficiency against platform dependency.

The Platform Trade-Off in the ServiceNow Ecosystem

You didn't have to build a billing engine. You didn't have to get SOC 2 Type II certified in month one. You didn't even have to hire a massive sales team because the ServiceNow store put you in front of large enterprise buyers. Building on the ServiceNow App Engine can accelerate enterprise distribution. But there is a catch that most founders don't see until they sit across from a Private Equity sponsor: The Platform Discount.

When you build 'Built on Now,' you are trading autonomy for velocity. In the early days, this is a brilliant trade. You leverage ServiceNow's trust, their security framework, and their data model to close enterprise deals that a standalone startup wouldn't touch for five years. But as you scale past $10M ARR, the math changes. Buyers—especially PE firms—look at your 25% revenue share to ServiceNow not just as a cost of goods sold (COGS), but as a structural cap on your EBITDA margin. Worse, they see Platform Concentration Risk. If ServiceNow changes their API, their pricing, or decides to build your feature natively, your business can lose leverage quickly.

However, the narrative that ServiceNow ISVs are not valuable is too simplistic. The smartest buyers in 2026 know that a well-architected ServiceNow ISV is actually more efficient than a standalone SaaS peer. The key is proving that your Net Revenue Retention (NRR) and CAC Efficiency outweigh the platform tax. If you are paying 25% to ServiceNow but saving 40% on Sales and Marketing because you draft off their field reps, you are winning. You just need to show the math.

A platform relationship only improves valuation when the distribution advantage outweighs the dependency risk and revenue-share burden.

Valuation Benchmarks: The 'Feature vs. Platform' Test

In valuation depends less on the badge and more on revenue durability, ownership of workflow, and platform concentration risk. Why the gap? It comes down to the Total Addressable Market (TAM) Ceiling. Investors worry you can only sell to existing ServiceNow customers. To break this ceiling and command a premium multiple, you must pass the 'Feature vs. Platform' test.

1. The Workflow Penetration Metric

Are you just a UI layer on top of ITSM, or do you own a proprietary workflow? High-value ISVs use App Engine to solve problems outside of IT—in Legal, Manufacturing, or Healthcare (Vertical solutions). If 80% of your usage is just 'reporting on ServiceNow data,' you are a feature. If you are originating data that doesn't exist elsewhere, you are a platform. Benchmark: Premium ISVs see customer concentration where no single customer (other than the platform itself) exceeds 5% of revenue.

2. The 'Agentic AI' Premium

With ServiceNow's aggressive push into 'Agentic AI' in 2025, the valuation goalposts have moved. Buyers are paying more attention to ISVs that have integrated Now Assist skills natively. If your app is 'AI-Ready'—meaning it feeds structured, clean data into ServiceNow's generative models—you command a higher multiple. Why? Because you make the core platform stickier. ISVs that demonstrate measurable AI adoption, such as deflected tickets or automated resolutions, can tell a stronger buyer story than legacy workflow apps.

Strategic Exit Readiness: Escaping the 'Lifestyle Business' Trap

To get a strategic exit, you must structurally de-risk the business for the buyer. This means attacking the three biggest objections in due diligence:

- Objection: 'What if ServiceNow kills the partnership?'

Defense: Secure the 'Built on Now' certification and maintain the partner standing partner tier. This isn't just a badge; it often comes with joint go-to-market protections. More importantly, diversify your influence. Don't just rely on the ServiceNow Store. Build relationships with the GSIs (Global Systems Integrators) like Deloitte and Accenture. If they are recommending you, you have a defensive moat against the platform itself. - Objection: 'Your margins are fake.'

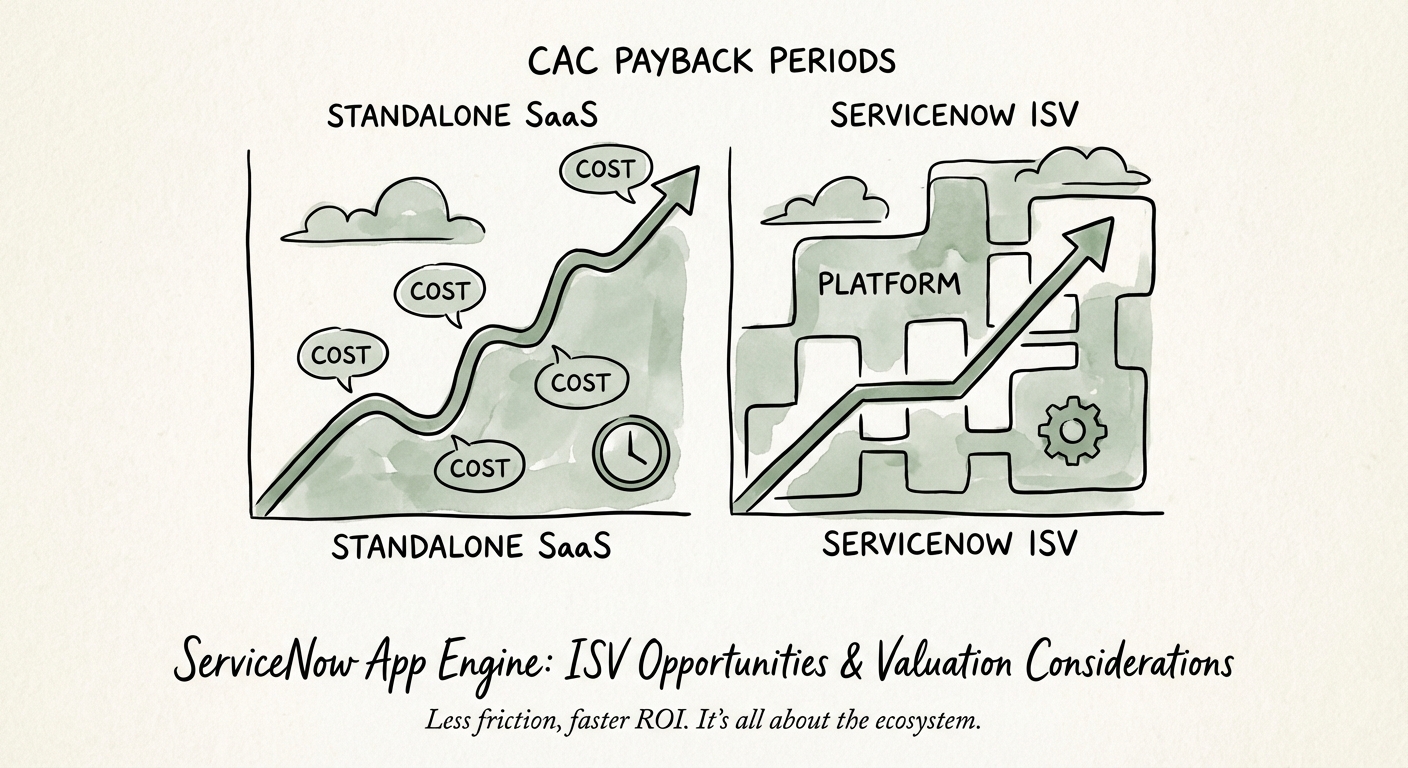

Defense: Buyers will treat the 25% revenue share as a permanent tax. Do not try to add it back to EBITDA. Instead, showcase your CAC Payback Period. A healthy standalone SaaS has a payback of 12-18 months. A ServiceNow ISV should be under 9 months. If you aren't hitting that efficiency, you are paying the tax without getting the benefit. - Objection: 'You have no IP.'

Defense: Document your 'Code Moat.' Show how much custom logic, industry-specific compliance (like FDA or FedRAMP), and proprietary data models you have built on top of App Engine. The more 'Vertical' you are, the less 'General' risk you carry.

Ultimately, a ServiceNow ISV needs to prove that it dominates a niche the platform is unlikely to absorb, solves an important workflow, and owns enough implementation knowledge to remain defensible. The difference is not just code; it is positioning.