The practical answer

- Short answer

- Building on Microsoft Dataverse got you to $5M ARR fast. Now it caps your exit multiple. The BYOL pivot and MACC co-sell move that fix it.

- Best fit

- Industry: B2B SaaS / Tech Services. Function: Revenue Operations & Product Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 6.1x Median Public SaaS Revenue Multiple (2025)

The gross-margin line on your P&L is the whole conversation

Picture the diligence call. A buyer's analyst has your financials open, and before anyone says a word about growth rate, logo retention, or your slick Power Apps UI, their eyes go to one number: gross margin. For a SaaS business that number is supposed to start with an 8. Yours starts with a 5.

That's the Dataverse tax, and it's the bill coming due for the speed that got you here. You picked Microsoft Power Platform because it handed you identity, security, and a database on day one. You shipped in six months instead of eighteen. Genuinely smart. But every seat you sell carries a Microsoft license cost you've quietly parked inside COGS. Pay Microsoft $10 per user per month, charge your customer $20, and the spreadsheet doesn't see a software company at 80% margins. It sees a reseller with a 50% markup and a nice interface.

And the spreadsheet is right. Public SaaS trades around a 6.1x median revenue multiple, but that number assumes software economics. Drag a third of your revenue out the door to a platform vendor and a buyer doesn't pay you a software multiple on reseller margins. They discount you, hard.

The fix is structural, not cosmetic, and you can start it this quarter: separate the platform cost from your IP. Move new contracts to a bring-your-own-license (BYOL) model where the customer holds their own Microsoft licenses directly. Yes, it adds a step to the sale. But it lifts that ~30% platform cost off your P&L and onto the customer's balance sheet, where it belongs. Run the same revenue through a clean BYOL structure and your unit economics stop reading like a reseller's and start reading like a SaaS company's.

Microsoft doesn't care about your $5M ARR. They care about the Azure consumption your app drags behind it. Point your pipeline at their wallet, and they open doors you couldn't kick down in a thousand years.

Your Microsoft partnership is not a sales team. Here's what actually moves the field.

Every Dataverse ISV founder eventually tells me the same thing: "We're a Microsoft Partner, so their reps will sell for us." I have watched that hope die in a hundred QBRs. Microsoft's field organization is coin-operated, and in 2026 the coins are Azure Consumption Revenue and Copilot seats. Your $50K ACV deal, on its own, does not move a single seller's number. It is invisible to them.

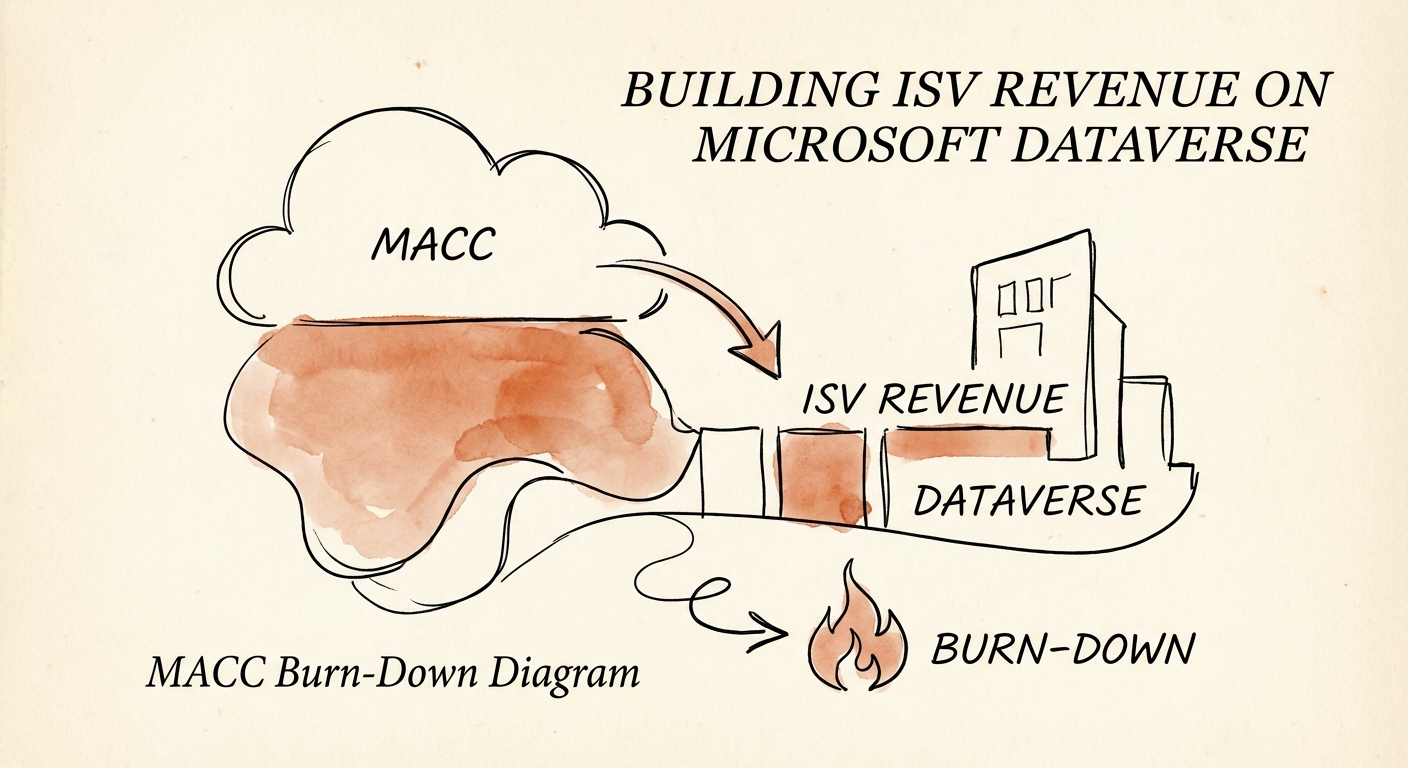

So stop trying to be liked and start being useful to their comp plan. The lever is the Microsoft Azure Consumption Commitment (MACC) — and it's the closest thing to free money in this ecosystem. Enterprise CIOs are sitting on multi-year Azure commitments they have to burn down or forfeit. When your offer is transactable on the commercial marketplace and IP co-sell eligible, that CIO can buy your software straight out of their pre-committed Azure budget. Microsoft's marketplace rules let qualifying purchases count against the customer's MACC, and the marketplace transaction fee on those deals is a flat 3%.

Think about what that does to your sale. The single longest step in an enterprise cycle is budget approval — finding the money, justifying it, getting sign-off. MACC deletes that step. The money is already spent. The CIO just decides where it lands. That's how a nine-month enterprise sales cycle collapses toward 60 days. If you're not transactable and co-sell eligible today, you are voluntarily bolting four extra months onto every enterprise deal you run — and handing the seller a reason to ignore you on top of it.

3x or 8x — Dataverse forces a binary, so pick on purpose

Building on someone else's platform makes your exit a coin with two faces and almost no middle. Which side lands depends on choices you make 18 months before anyone signs an LOI.

The 3x face is the trap. You're a tenant of Microsoft's roadmap. When they revise the Common Data Model, your engineers drop their roadmap to chase breaking changes. Your margins sit at 55% because the platform tax never left your P&L. A buyer adds all of it up under one label — "platform risk" — and prices you accordingly. There's no clever pitch that talks your way out of a number a CFO can see.

The 8x face is the prize, and it's earned, not argued. Here you're the sticky layer that keeps a customer locked into Dynamics 365 — pull your product out and their whole workflow breaks. You generate enough data gravity that switching is unthinkable. And you've used MACC to land Fortune 500 accounts a Series B company has no business winning, because you stopped selling software and started selling Azure consumption that happens to be wrapped in your software. Forrester's economic-impact analysis of Power Platform exists precisely because that ecosystem leverage is real and measurable when you build for it.

So here's your Monday: pick the metric your board reviews. If your pipeline is measured only in ARR, you're optimizing for the 3x face. Add ACR influence — the Azure consumption your product pulls behind it — to the top of the deck. That single reframe is what gets a board leaning forward instead of bracing for the platform-risk discount. Treat Microsoft as a vendor and you'll pay the tax. Treat them as a channel and you'll bill it to them.