The practical answer

- Short answer

- ServiceNow Elite status is no longer a differentiator. Learn the specific financial and operational metrics PE firms demand for premium exits in 2026.

- Best fit

- Industry: IT Services / SaaS Implementation. Function: Corporate Strategy / M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

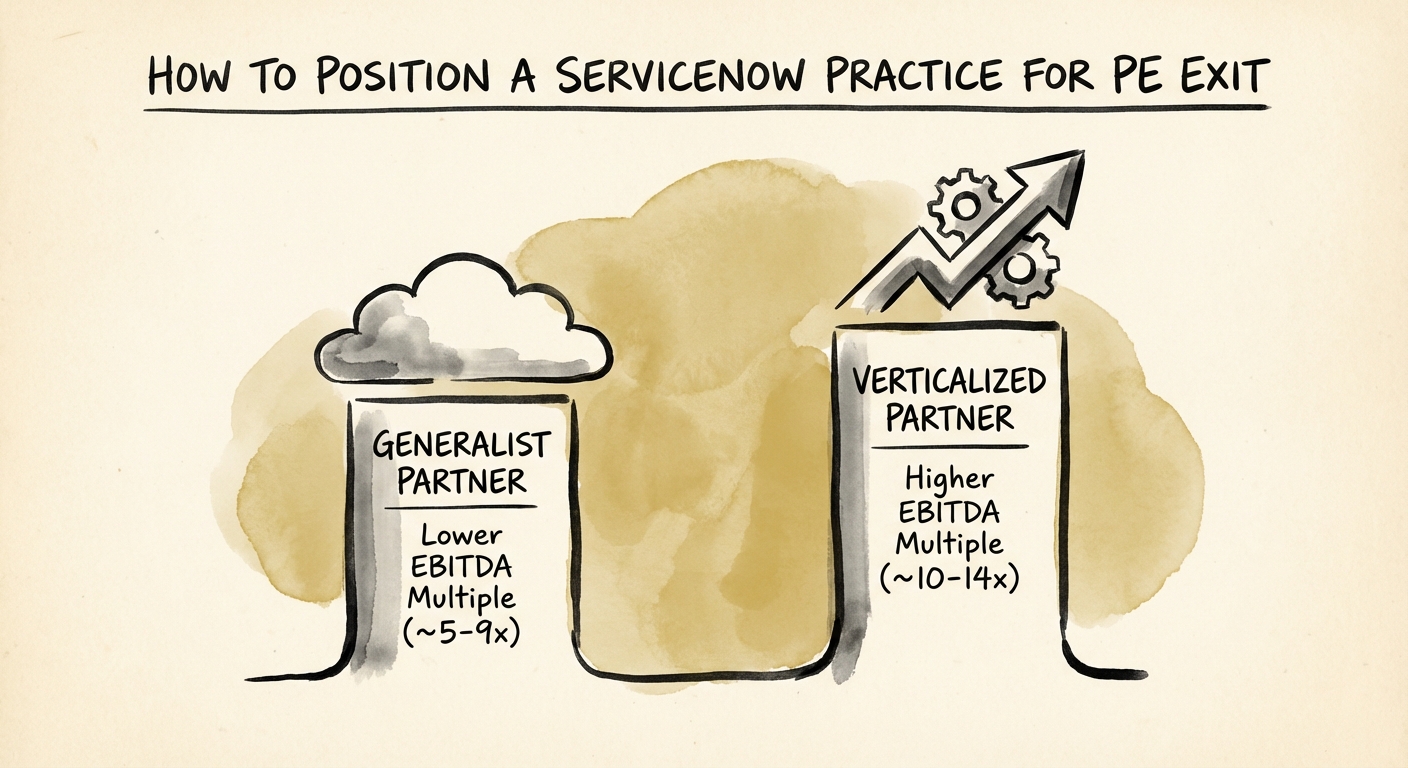

- 10-14x EBITDA multiple for 'Platform' partners with >30% recurring revenue vs. 6-8x for project-based firms.

The "Elite" Status Is No Longer a Differentiator

If you are a ServiceNow Elite Partner generating $15M to $50M in revenue, you have built a successful business. But if you are planning an exit in 2026, you are walking into a trap. Five years ago, achieving "Elite" status was a golden ticket to a high-multiple exit. Today, it is merely the price of admission.

The market has bifurcated. On one side, we see generalist implementation firms trading at standard professional services multiples (6x–8x EBITDA). These firms are viewed by Private Equity as "capacity shops"—highly dependent on headcount, susceptible to wage inflation, and constantly hunting for the next project. On the other side, we see "Platform" partners trading at premium multiples (10x–14x EBITDA). These firms have cracked the code on recurring revenue, verticalization, and intellectual property.

For a founder, the difference between these two outcomes is not just a rounding error; it is often the difference between a "life-changing" exit and an "earn-out heavy" acqui-hire. Private Equity sponsors are no longer buying capacity; they are buying specialization and efficiency. As noted in recent market intelligence, the top-quartile ServiceNow partners are now delivering 40-55% gross margins and 15-20% EBITDA margins while growing at 25%+ annually. If your firm is running at 10% EBITDA because you are over-servicing clients to maintain retention, you are not ready for a premium exit.

You can't sell a 'hero culture' to a private equity firm. They can't scale your intuition. They can only scale your systems.

The Financial Engineering of a Premium Exit

To move from the "Body Shop" bucket to the "Platform" bucket, you must re-architect your P&L before you ever speak to an investment banker. The most critical metric PE buyers scrutinize is your Revenue Mix.

1. The Managed Services Pivot

Pure project-based revenue is lumpy and unpredictable. It terrifies buyers because it resets to zero every January 1st. Premium valuation requires a layer of recurring revenue—specifically, Managed Services. Your goal should be to shift at least 30% of your revenue into multi-year Managed Services contracts. This isn't just about "support hours"; it's about selling outcomes (e.g., "We manage your HR Service Delivery module for $25k/month"). This creates the transferable value that drives multiple expansion.

2. The Verticalization Multiplier

Generalists compete on rate; specialists compete on value. A "ServiceNow Partner for Everyone" is a commodity. A "ServiceNow Partner for Regional Banks" or "ServiceNow Partner for Life Sciences Manufacturing" is a strategic asset. PE firms are actively consolidating the ecosystem, looking for specific puzzle pieces to add to their platform investments. If you can demonstrate deep, defensible expertise in a regulated industry, you command a premium because you reduce the buyer's customer concentration risk and integration friction.

3. The "IP" Hallucination

Be careful with "Intellectual Property." Many founders claim they have IP because they wrote some code accelerators. Buyers only value IP if it is monetized separately. If your IP is just a tool your consultants use to work faster, that shows up in your Gross Margin, not as a separate revenue line. If you can show a separate SKU on your invoices for a proprietary app or connector, that is true SaaS revenue, and it pulls your blended multiple upward.

Founder Extraction: The Final Hurdle

The final and most painful diagnostic for a ServiceNow practice is the "Key Person Dependency." In many $20M firms, the founder is still the Lead Architect on the largest accounts or the Closer on the biggest deals. This is a deal-killer.

In a PE transaction, the buyer is underwriting the future cash flows of the business, not the heroics of the founder. If you leave, does the revenue churn? You need to systematically fire yourself from sales and delivery at least 12 months before an exit. This means installing a VP of Sales who can close without you and a Delivery Head who owns the utilization metrics.

Documenting your "Tribal Knowledge" into Standard Operating Procedures (SOPs) is the only way to prove to a buyer that your margins are sustainable. When a PE firm conducts Operational Due Diligence, they are looking for the "Playbook"—the documented process that ensures a junior consultant can deliver the same quality as a senior architect. Documented processes are the bridge between a founder-led practice and a scalable platform.