The practical answer

- Short answer

- Most ServiceNow partners are stuck in the 'services trap,' trading at 1.5x revenue. Learn how to harvest Intellectual Property (IP) to unlock 6x+ multiples and exit readiness.

- Best fit

- Industry: IT Services / SaaS Ecosystem. Function: Product Strategy & Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 1.5x Typical Revenue Multiple for Pure Services Firms

The 'Elite' Partner Valuation Paradox

You have hit $20M in revenue. You have achieved Elite Partner status. You have 150 certified engineers and a steady stream of implementation projects. In the eyes of the ecosystem, you are a success story. In the eyes of a Private Equity buyer, you are a liability.

Here is the hard truth about the 2025 ServiceNow ecosystem: Capacity is a commodity; Capability is the asset.

If your revenue growth is linearly tied to headcount—meaning to add $1M in revenue, you must hire 4 more engineers—you are building a low-margin services firm. These firms trade at 1.0x to 1.5x revenue in the current M&A market. Why? Because you are selling hours, and hours don't scale. You have built a job, not an asset.

Conversely, ServiceNow partners that have successfully productized their intellectual property (IP)—converting repetitive custom code into "Built on Now" store applications or repeatable accelerators—are trading at 4x to 6x revenue. They have broken the linear link between revenue and headcount. They don't just implement; they license.

The market signal is straightforward: buyers pay more for revenue that can scale without adding delivery headcount at the same rate. ServiceNow partners with packaged accelerators, scoped applications, and reusable implementation IP look materially different from firms that only sell project hours. If you want a valuation that reflects a software company rather than a staffing agency, you must stop treating IP as an afterthought.

Services revenue is only the starting point. The valuation premium appears when repeatable implementation knowledge becomes packaged, transferable IP.

The Diagnostic: Are You Building Reusable IP?

Most partners are sitting on millions of dollars of potential IP, but they bury it in one-off project work. Every time your team writes a custom script for a client to integrate Workday with HRSD, or builds a custom portal widget for a healthcare client, that code typically lives and dies with that single project. That is waste.

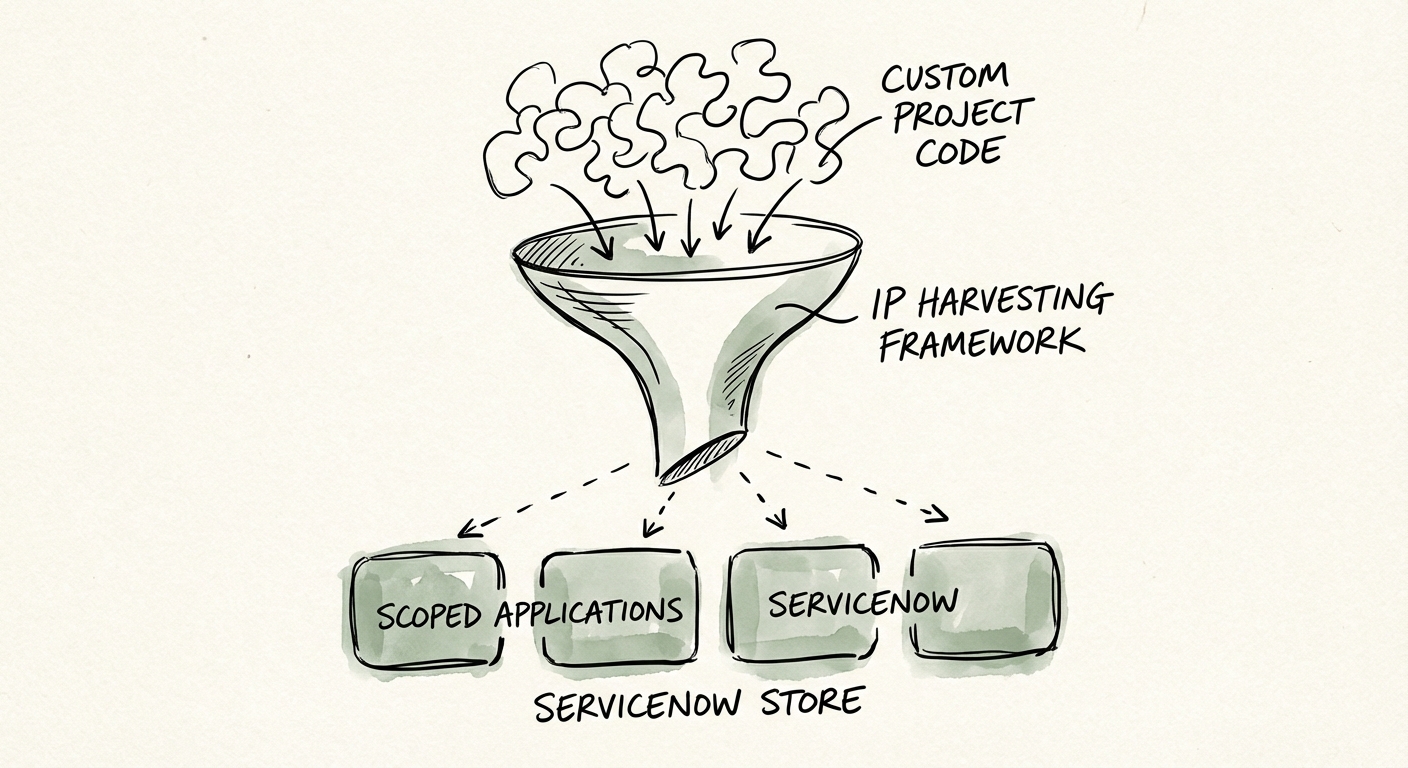

The IP Harvesting Framework

To pivot from services to IP, you don't need to halt operations and build a R&D lab. You need to implement Active Harvesting.

- The Audit: Look at your last 50 projects. Identify the "Common Customizations." Where did you write similar code 3+ times? (e.g., specific HIPAA compliance workflows, manufacturing floor incident reporting).

- The Abstraction: Pull that code out of the customer instance. Strip the hardcoded client data. Generalize the logic.

- The Packaging: Wrap it in a scoped application. Document the installation process. This transforms "tribal knowledge" into a transferable asset.

This shifts your margin profile. A pure implementation project runs at ~40-45% gross margin. A project that leverages your proprietary IP accelerator can run at 65-70% gross margin because you are charging for the value of the solution, not the hours it took to deploy it.

Execution: The Hybrid Services-and-IP Strategy

You do not have to become a pure ISV (Independent Software Vendor) overnight. In fact, the most valuable partners in 2025 are hybrids. They use their IP to win services deals.

Imagine competing for a $500k HR transformation deal.

Competitor A pitches: "We have smart people, we'll figure it out in 6 months."

You pitch: "We have a pre-built 'Healthcare Onboarding Accelerator' certified on the ServiceNow Store. We start at 60% complete on Day 1. We spend the remaining time tailoring it to your specific needs."

You win the deal. You charge the same $500k. But you deliver it in half the hours. Your EBITDA margin on that project doubles. And crucially, you retain the IP.

This is how you escape the technical debt of one-off customizations and build a scalable, defensible moat. When a PE firm looks at your books, they won't just see a services backlog; they will see a library of proprietary assets that generate high-margin revenue. That is the difference between a 1.5x exit and a 6x exit.