The practical answer

- Short answer

- Turn one-off NetSuite customizations into 8x revenue Intellectual Property. A diagnostic guide for Service Founders looking to capture the SaaS multiple arbitrage.

- Best fit

- Industry: B2B Tech Services & SaaS. Function: Product Strategy & Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 40k+ Global NetSuite customers, representing the Total Addressable Market (TAM) for any certified SuiteApp.

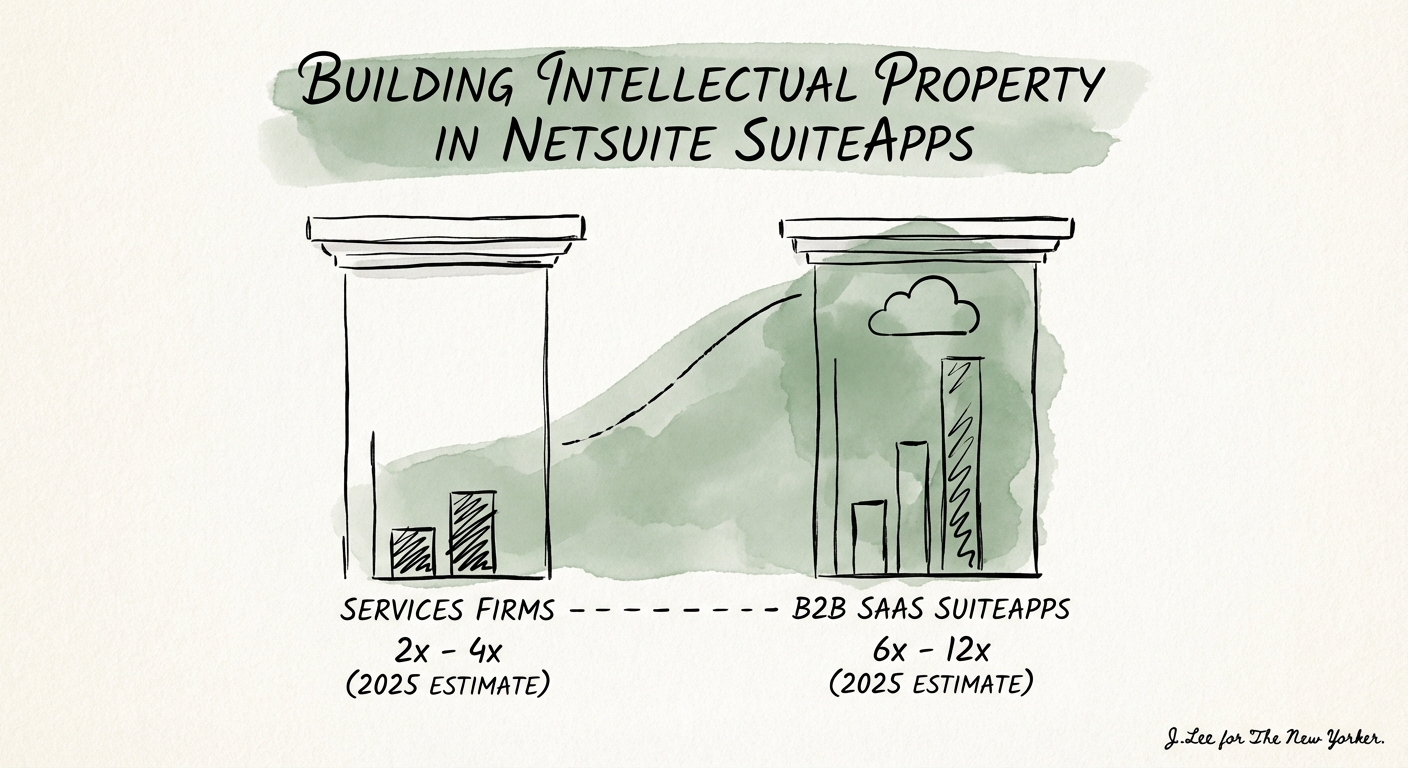

The Great Valuation Arbitrage: Services vs. IP

If you are running a NetSuite implementation practice or a tech-enabled services firm, you are likely trapped in the linear growth cycle: to make more money, you need more people. You sell hours. You trade time for money. And when private equity comes knocking, they value you like a services firm.

Here is the math that should keep you awake at night: In 2025, professional services revenue trades at 1.2x to 1.5x revenue. Intellectual Property (SaaS) revenue trades at 6x to 10x ARR.

Consider two firms, both doing $10M in revenue:

- Firm A (Services): $10M revenue × 1.5x multiple = $15M Enterprise Value.

- Firm B (Hybrid): $5M services + $5M SuiteApp ARR.

Firm B's valuation looks like this: ($5M × 1.5) + ($5M × 8.0) = $47.5M Enterprise Value.

Same total revenue. Triple the exit value.

Most NetSuite partners are sitting on "warehoused code"—scripts written for one client that solved a universal problem (e.g., complex commission calculations, inventory allocation, or connector APIs). You charged the client $15,000 once. If you packaged that script into a licensed SuiteApp, you could charge 500 customers $5,000 every year. That is not just revenue; that is transferable value.

Services revenue pays the bills today. IP revenue builds the wealth for tomorrow. The moment you stop selling your time and start selling your code, you change the economic gravity of your business.

The 'Built for NetSuite' (BFN) Gauntlet: It's Not Just a Badge

You cannot simply zip up a bundle of SuiteScripts and call it a product. To command a SaaS multiple, your IP must be defensible, scalable, and verified. In the Oracle ecosystem, the gold standard is the Built for NetSuite (BFN) verification.

For an acquirer, the BFN badge is a proxy for technical due diligence. It tells them:

- Security: The code meets security standards and doesn't open backdoors.

- Compatibility: It won't break when NetSuite updates (which happens twice a year).

- Governance: You have a documented development lifecycle, not just a cowboy coder making changes in production.

The BFN process is rigorous. It involves submitting a questionnaire, providing customer references, and performing a live product demonstration to the NetSuite SuiteCloud Developer Network (SDN) team. Crucially, this badge must be renewed with every major NetSuite release (e.g., 2025.1, 2025.2). If you fail to renew, you lose the badge.

The Trap: Many founders try to sell "IP" that is really just a library of copy-paste code snippets. Buyers see right through this. If it requires an engineer 20 hours to deploy and customize for each new client, it is not a product; it is a service accelerator. Service accelerators improve margins, but they do not expand multiples.

The M&A Reality: What Buyers Actually Pay For

I have sat on the buy-side of these deals. When we look at a "Productized Service" firm, we are hunting for three specific proof points to validate the valuation lift:

1. The Separation of Church and State

Your IP revenue must be tracked separately from your services revenue. If they are commingled in the P&L, a Quality of Earnings (QofE) provider will reclassify it all as services revenue. You need separate SKUs, separate contracts (MSAs vs. License Agreements), and ideally, a separate P&L.

2. The 'Stickiness' Metric

True SuiteApps have incredibly low churn (often <3%) because they are embedded in the ERP workflow. If your churn is 15%, you don't have a product; you have a consulting gig that ended. We look for Net Revenue Retention (NRR) above 110%.

3. Transferability Without The Founder

If the "product" breaks when your lead developer goes on vacation, it has zero enterprise value. Documentation is the difference between a tool and an asset. The code must be clean, annotated, and deployable by a junior resource.

The Strategy: Don't try to build the next Salesforce. Look for the "unsexy" gaps in the NetSuite ecosystem—industry-specific compliance, niche logistics, or tax localizations. With 40,000+ NetSuite customers, capturing just 1% of the market with a $10k/year app generates $4M in pure EBITDA. That is an asset worth selling.