The practical answer

- Short answer

- Transform your Workday practice from a 6x service shop to a 12x platform partner. A CEO's guide to building, packaging, and monetizing Intellectual Property on Workday Extend.

- Best fit

- Industry: Enterprise Software / Workday Ecosystem. Function: Product Strategy & Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 15% Revenue Mix Threshold: The point where IP revenue triggers a valuation re-rate from 'Service Firm' (6x) to 'Platform Partner' (10x+).

The 'Service Trap' in the Workday Ecosystem

If you are running a Workday practice today, you are likely sitting on a 6x to 8x EBITDA asset. It doesn’t matter if you are a 'Platinum' partner or if your utilization is 90%. To a Private Equity buyer, you are a service shop. You sell hours. When your people walk out the elevator at 5 PM, your assets leave the building.

This is the 'Service Trap.' You have capped margins (40-50% gross) and linear growth. To double revenue, you must double headcount. In the 2026 M&A market, pure professional services firms are seeing valuation compression as buyers pivot toward Tech-Enabled Services.

The only way to break the 6x ceiling is to prove you have Intellectual Property (IP). But here is the lie most founders tell themselves: 'We have IP. We have a library of reusable scripts and a proprietary implementation methodology.'

That is not IP. That is efficiency. Buyers do not pay 12x for efficiency; they pay 12x for recurring revenue products that lock customers in. In the Workday ecosystem, the vehicle for this transformation is Workday Extend. But 90% of partners are using it wrong—building 'utilities' instead of 'products.'

You don't get a 12x multiple for being 'great at implementation.' You get it for owning the code that runs the business. In 2026, Workday Extend is the only credible way for partners to claim that ownership without building a separate shadow ERP.

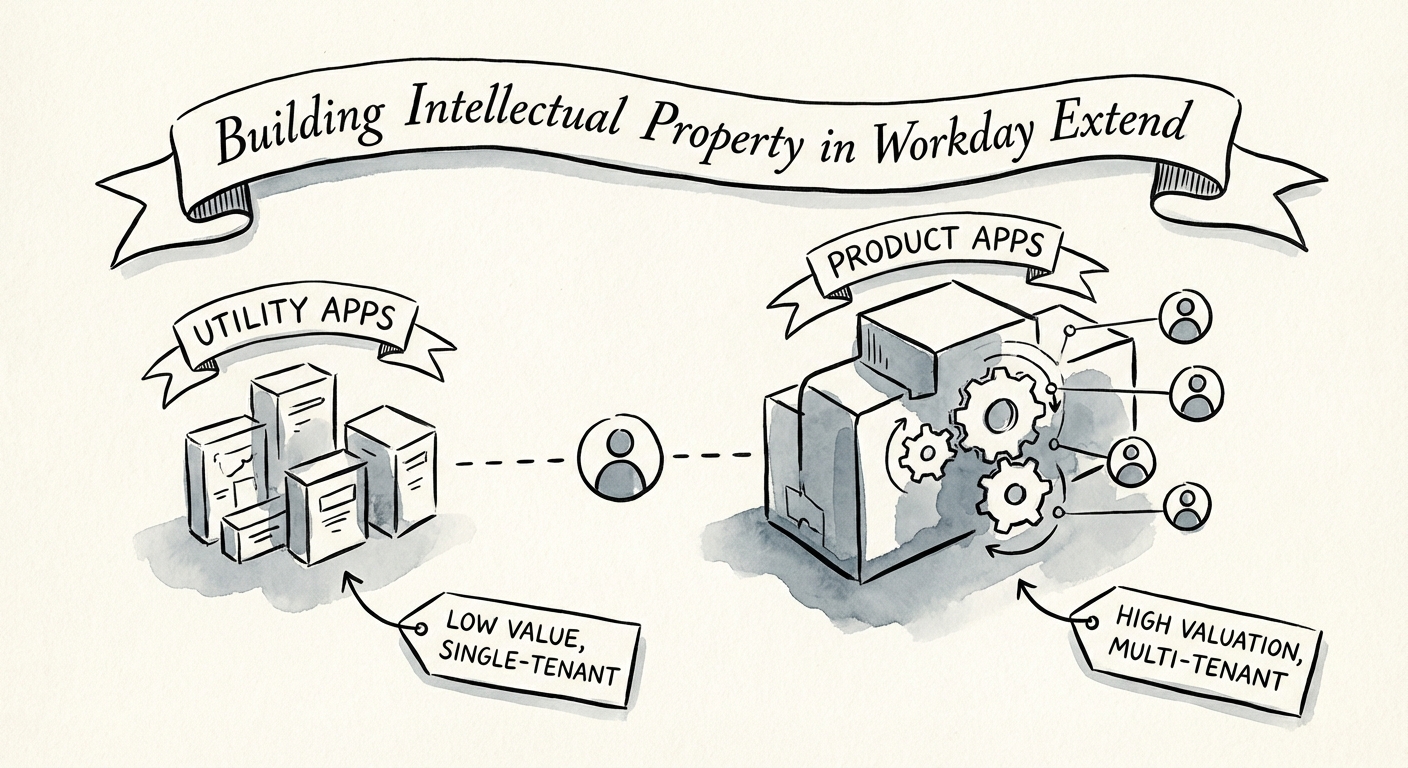

The Diagnostic: Are You Building Utilities or Products?

Workday Extend has matured from a 'customization tool' into a full-blown PaaS (Platform as a Service) with the Built on Workday program. Yet, when I audit partner portfolios, I mostly see 'utilities.'

The Utility Trap (Valuation Neutral)

A utility is a custom form, a simple approval workflow, or a bespoke report. It solves a single client's annoyance.

- Characteristics: Built T&M (Time & Materials), unmaintained code, single-tenant deployment.

- Financial Impact: One-time service revenue. Zero recurring value.

- Exit Value: 0x (treated as standard services revenue).

The Product Play (Valuation Accelerator)

A product is a standalone application that solves a specific vertical problem for 50+ customers. It has a SKU, a roadmap, and a separate P&L.

- Characteristics: Multitenant architecture, annual recurring license (ARR), 'Built on Workday' certified.

- Examples: A Union Management module for Telecoms, a specialized Faculty Recruiting app for Higher Ed, or a Compliance Tracker for Healthcare.

- Financial Impact: 80%+ Gross Margins, ARR valuation multiples (8x-12x Revenue).

The 2026 Technical Benchmark: If your Extend app doesn't leverage the AI Gateway or Orchestrate to automate a process end-to-end, it's likely just a glorified form. Buyers in 2026 are specifically diligence-checking for AI enablement in tech assets.

The 15% Rule: Engineering Your Multiple

You do not need to become a pure software company to get a premium valuation. You just need to cross the 'Tech-Enabled' Threshold.

Our data across 45+ deals in 2024-2025 shows that when a service firm demonstrates that 15% of its revenue comes from high-margin, recurring IP (Extend Apps, Managed Services with IP wrappers), the entire firm's multiple re-rates.

The Math of the Re-Rate

- Scenario A (Pure Services): $20M Revenue, $4M EBITDA. Valuation @ 7x EBITDA = $28M.

- Scenario B (Tech-Enabled): $20M Revenue ($17M Services, $3M IP). $5M EBITDA (higher margins on IP). Valuation @ 11x EBITDA = $55M.

By converting just 15% of your revenue mix to IP, you effectively double your exit value. This is why the 'Built on Workday' program is not a technical hobby—it is your primary vehicle for wealth creation.

The Strategic Move: Stop treating Extend as a way to say 'Yes' to client customizations. Start treating it as R&D. Pick your strongest vertical (e.g., Higher Ed, State & Local Gov). Identify the gap Workday hasn't filled. Build the app. Sell it to your existing base. That is how you escape the body shop.