The practical answer

- Short answer

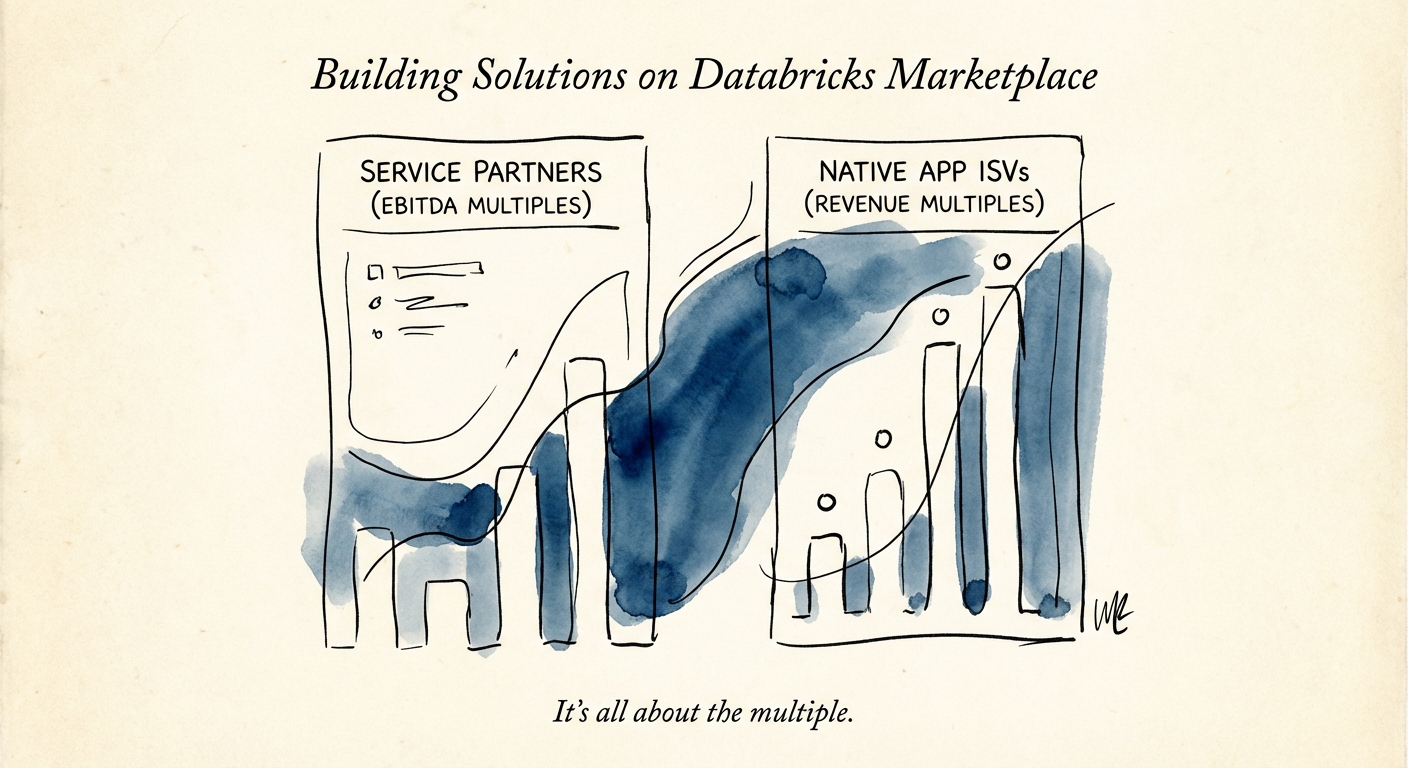

- Why building a Native App on Databricks Marketplace is the fastest path to a 12x exit. Analysis of valuation premiums, MACC burn-down, and the 'Data Intelligence' shift.

- Best fit

- Industry: B2B Tech / Cloud Ecosystems. Function: Product Strategy / Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 40% Reduction in sales cycle length for transactable Marketplace solutions vs. direct paper.

The New Center of Gravity for AI Exits

For the last decade, the 'modern data stack' was a fragmented collection of tools. You had your warehouse (Snowflake), your processing (Databricks), and a dozen SaaS tools extracting data to analyze it elsewhere. In 2026, that architecture is a liability. The market has shifted decisively toward the Data Intelligence Platform—a unified operating system where data, AI models, and applications coexist.

For Founders and CEOs, this shift creates a binary outcome in valuation. If your product requires customers to export data (egress) to your cloud, you are fighting an uphill battle against InfoSec teams and 'data gravity.' You are a foreign object in the enterprise. Conversely, if you build a Lakehouse App that runs native compute directly on the customer's data, you are infrastructure.

The valuation gap is widening aggressively. Recent M&A data from Q4 2025 indicates that 'Native App' ISVs on Databricks are trading at 8x-12x Revenue, while traditional SaaS vendors requiring data replication are stalling at 4x-6x. The market isn't just paying for software anymore; it's paying for proximity to the data. If you are a founder looking at a $50M exit, pivoting your architecture to the Lakehouse isn't just a technical decision—it's the single highest-ROI move you can make for your cap table.

In 2026, if your software requires data egress, you've already lost the InfoSec war. Lakehouse Apps aren't a feature; they are the new standard for enterprise trust.

The Commercial Moat: MACC Burn-Down

The technical advantage of 'zero egress' is clear, but the commercial advantage is what actually closes deals. We are in an era of scrutiny where every net-new software contract requires CFO sign-off. However, enterprises are sitting on billions of dollars in committed cloud spend (MACC for Azure, EDP for AWS) that they must use or lose.

By listing a transactable solution on the Databricks Marketplace, you convert your software cost into cloud consumption. You are no longer a 'new line item' in the budget; you are a mechanism for the CIO to utilize their pre-committed Databricks Units (DBUs). This structural arbitrage accelerates sales cycles by an average of 40% and increases average contract value (ACV) by 30%.

The 'Brickbuilder' Accelerator

Private Equity firms are increasingly using the 'Brickbuilder' designation as a proxy for technical due diligence. A standard partner badge is table stakes. A 'Brickbuilder' solution, validated for specific industry verticals (like Financial Services or Healthcare), signals to acquirers that your IP is defensive. It proves your solution isn't just a generic wrapper, but a validated extension of the Databricks platform. When we advise on ecosystem exits, we see a distinct premium for partners who have crossed this validation threshold.

Strategic Pivot: From Service to Solution

Many partners we speak with are trapped in the 'Service Trap'—selling time for money at 1.5x revenue valuations. The Databricks Marketplace offers a bridge to escape this gravity. You don't need to become a full-blown SaaS company overnight. You can start by packaging your most repeatable service workflows—data quality checks, industry-specific models, or governance rules—as a 'Solution Accelerator' or a Native App.

This 'IP-wrapping' strategy does two things:

- It creates recurring revenue (ARR): Even if it's a small component, it shifts your revenue mix.

- It increases 'stickiness': Services can be fired; embedded apps that manage data pipelines are rarely ripped out.

The window to claim your vertical on the Lakehouse is closing. Databricks' ecosystem grew by 31% last year alone, with over 230 new partners entering the fray. The winners of 2026 won't be the generalists; they will be the specialists who built the definitive 'Native App' for their specific domain. For a deeper dive on how specialized IP drives valuation, review our analysis on data product valuations.