The practical answer

- Short answer

- Analysis of Databricks partner program economics for 2026. Why 'Elite' status costs $400k+ in soft costs and how specialized Data & AI firms trade at 13.5x EBITDA.

- Best fit

- Industry: Data & AI Consulting. Function: Partnerships & Alliances

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 22% Gross margin erosion seen in firms chasing 'Elite' status without a specialized rate card.

The Cost of the Badge: Analyzing the 'Elite' Premium

For many consultancy CEOs, the path to ‘Elite’ status in the Databricks ecosystem feels like a mandatory graduation. You start as Registered, grind to Select, and then view Elite as the gateway to enterprise deal flow. However, the unit economics of this ascent often tell a different story. In 2026, the ‘Elite’ tier isn’t just a revenue threshold; it is a certification tax that can erode 22% of your gross margin if not managed with surgical precision.

Achieving and maintaining top-tier status requires a density of certified resources that forces a choice: pull billable seniors off projects to study, or hire ‘paper tigers’ whose only value is the badge they carry. Our analysis of mid-market data consultancies ($10M-$50M revenue) shows that firms chasing Elite status purely for the logo often see a 15% drop in EBITDA margins during the qualifying year due to non-billable training time and certification fees. The program’s requirement for 200+ certifications (for top-tier global recognition) creates a ‘certification treadmill’ where your training budget becomes a fixed cost rivaling your rent.

The Brickbuilder Breakeven Point

The only mathematical justification for absorbing these costs is the ‘Brickbuilder’ accelerator program. Partners who simply resell and implement trade at 1x revenue. Partners who build repeatability via Brickbuilder Solutions—packaging IP like Unity Catalog migrations or industry-specific Lakehouse templates—unlock a different economic reality. The data shows that the ‘Elite’ badge only yields a positive ROI if it is paired with a proprietary solution that drives consumption revenue, not just service hours.

The 'Elite' badge is a vanity metric if it doesn't come with IP. In 2026, you aren't paid for the badge; you're paid for the consumption you drive.

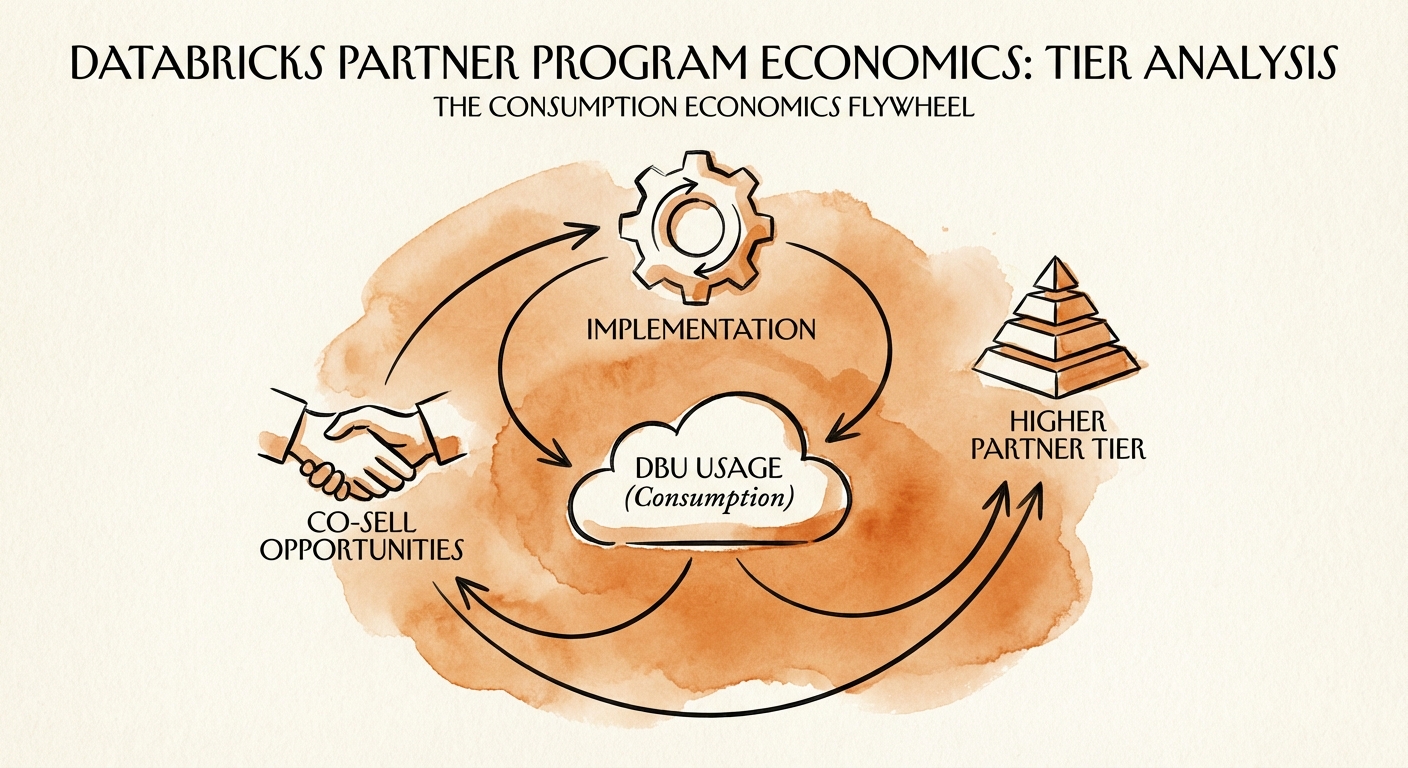

The Great Pivot: From Implementation to Consumption

The Databricks partner economy has fundamentally shifted from ‘billable hours’ to ‘Databricks Units’ (DBUs). In the old model, your value was defined by the complexity of the implementation. In the 2026 model, your value is defined by how much compute your client burns after you leave. This ‘Consumption Economics’ shift is why legacy System Integrators are struggling to maintain margins while agile, data-native firms are soaring.

Databricks’ growth—targeting $3.7B in revenue with 140% NRR—is fueled by consumption. Consequently, the partner program rewards firms that drive DBU usage. If your business model is ‘lift and shift’ migration with no managed service tail, you are misaligned with the vendor’s incentives. You might get the project, but you won’t get the co-sell support for the next one.

The DBU Multiplier

We are seeing a bifurcation in partner valuations based on this metric. ‘Project-based’ Databricks partners are seeing deal flow slow down as their ‘land’ motions fail to ‘expand.’ Conversely, partners with a Managed DataOps offer—who contractually commit to optimizing their client’s DBU spend—are seeing 30% higher retention rates. The math is simple: Databricks account executives get paid on consumption. If your firm builds efficient pipelines that scale usage (even while optimizing unit cost), you become the AE’s best friend. If you deliver a static warehouse and walk away, you become invisible.

Valuation Implications: The 13.5x Specialist Premium

The most critical metric for a founder isn’t the partner tier; it’s the exit multiple. The market has definitively split. Generalist IT consultancies adding Databricks to a laundry list of capabilities are trading at 6x-8x EBITDA. They are viewed as ‘staffing’ businesses with low barriers to entry. In stark contrast, specialized ‘Data & AI’ firms that have achieved ‘Elite’ status and own Brickbuilder IP are trading at 12x-15x EBITDA.

This ‘Specialist Premium’ exists because acquirers (both PE and strategic) are not buying headcount; they are buying competency depth and customer intimacy within the Lakehouse ecosystem. A firm with 50 certified Databricks engineers and three validated Brickbuilder solutions is worth significantly more than a firm with 200 generalist cloud engineers.

The ‘Generalist’ Discount

Beware the trap of the ‘Generalist’ approach. We frequently audit firms that claim ‘Elite’ status across AWS, Azure, Snowflake, and Databricks. While impressive on a slide, these firms often suffer from the ‘Generalist Discount’ in due diligence. They lack the depth to command premium bill rates ($250+/hr for architects) and their utilization suffers from context switching. To maximize your Databricks partner ROI, go deep. Build IP. Focus on DBU consumption. And treat the ‘Elite’ badge as a lagging indicator of excellence, not a leading generator of revenue.