The practical answer

- Short answer

- Analysis of the true costs and valuation impact of ServiceNow Elite Partner advancement. Benchmarks on certification costs, margin erosion, and the valuation gap.

- Best fit

- Industry: IT Services. Function: Partner Ecosystem

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- $17k Direct cost per CMA certification, before travel and lost billable time.

The Velvet Rope is Now a Razor Wire

For years, the playbook for ServiceNow partners was simple: hire warm bodies, get them their Certified System Administrator (CSA) badges, and ride the implementation wave to a 20% margin. That era is dead. The 2025 restructuring of the ServiceNow Partner Program didn’t just raise the bar; it effectively closed the door on "body shop" operations.

We recently analyzed the consolidation of the partner ecosystem. The number of recognized Elite partners dropped from ~134 to 79 worldwide in the latest program update. This isn’t an accident; it’s a purge. ServiceNow is actively filtering out firms that trade on capacity rather than capability. For a Founder sitting at the Premier tier, the message is brutal: Advance or become irrelevant.

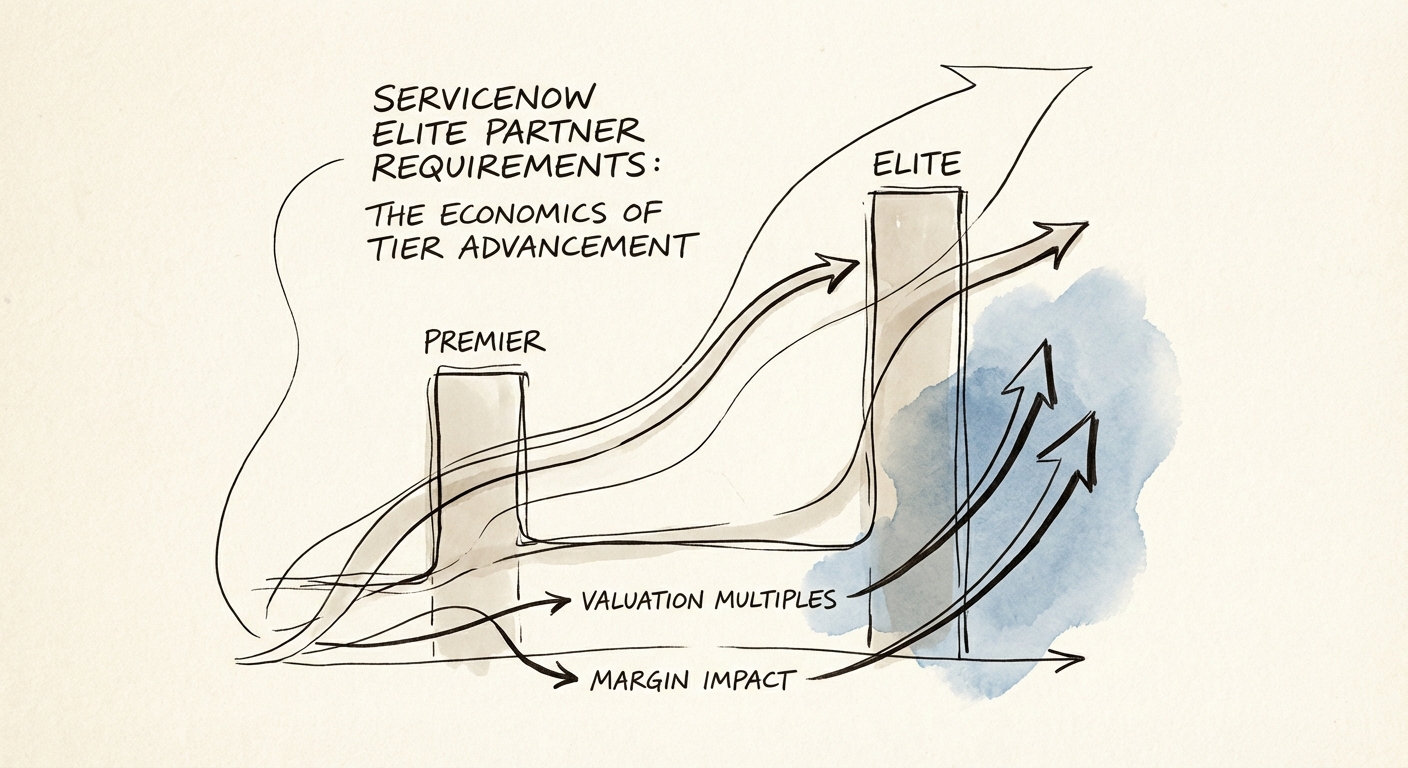

But here is the math the channel managers won’t show you. The jump from Premier to Elite isn’t just about closing more ACV (Annual Contract Value). It requires a fundamental restructuring of your unit economics. You aren’t just buying badges; you are accepting a temporary 8-12% EBITDA suppression to fund the "capability tax" required to enter the room where enterprise deals happen.

The jump from Premier to Elite is not a sales challenge; it is a balance sheet challenge. You are trading 18 months of margin for a 4x turn on your exit multiple.

The "Capability Tax": Calculating the True Cost of Ascent

Let’s break down the actual cost of the "4 Cs" (Capacity, Competency, Customer Success, Capability) required for Elite status. The most painful line item isn’t the program fee—it’s the Certified Master Architect (CMA) requirement.

To secure Elite status, you need demonstrable expertise that goes beyond basic implementation. A single CMA designation costs $17,000 in direct program fees. But that’s a rounding error compared to the operational cost:

- Lost Billable Hours: The CMA program is a 22-week sprint requiring roughly 20% of your top architect’s time. That’s ~$50,000 in lost revenue capacity per candidate.

- Salary Inflation: Once your architect gets that CMA badge, their market value jumps instantly. Our data shows a $40,000 annual premium for CMAs vs. standard Senior Architects. If you don’t pay it, a Global Elite partner (like Accenture or Deloitte) will.

- The Retention Trap: We see a 30% attrition rate for newly certified CMAs within 12 months at firms that don’t adjust comp plans before the certification is awarded.

For a firm doing $15M in revenue, the "Sprint to Elite" costs roughly $250,000 to $400,000 in direct costs and margin erosion over 18 months. If your Board expects linear EBITDA growth during this phase, you are setting yourself up to fail.

The Payoff: Why the Multiple Justifies the Pain

If the costs are so high, why do it? Because the valuation gap between "Premier" and "Elite" is widening into a canyon. In 2025, we are seeing Premier partners trade at 6x-8x EBITDA, treated largely as staffing augmentation firms. Elite partners are trading at 10x-14x EBITDA.

The "Elite" badge signals to Private Equity buyers that you have:

- Recurring Revenue Quality: Elite partners typically have 30%+ higher managed services attach rates.

- Deal Registration Priority: Access to the "Big Room" deals where ServiceNow field sales bring you in, reducing your CAC by 40-50%.

- Defensibility: The consolidation to ~79 global Elite partners means you are in a scarcity asset class.

The Verdict: If you are stuck at $15M revenue, you have two choices. Stay Premier, optimize for 25% EBITDA, and sell for a modest multiple. Or bite the bullet, accept 18 months of compressed margins, invest in the CMAs, and build a platform worth 12x. Just don’t try to do both at the same time.