The practical answer

- Short answer

- The 2026 EdTech M&A playbook for PE operating partners. How to spot phantom ARR, adjust for school-year seasonality, and navigate the ESSER funding cliff.

- Best fit

- Industry: Education Technology. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 1.6x Median Revenue Multiple for low-retention EdTech firms in Q4 2025 (down from 7.2x peaks).

The ESSER Hangover: Identifying 'Stimulus-Bloated' Revenue

The party is officially over. For the last four years, K-12 EdTech revenue has been artificially inflated by the $190 billion Elementary and Secondary School Emergency Relief (ESSER) fund. But as of late 2024, the obligation deadline passed, and the liquidation window closes in early 2025 (with rare extensions to 2026). This has created a massive "Revenue Quality" problem for PE buyers and sellers alike.

We are seeing portfolios reporting "growth" that is actually just the final drawdown of federal stimulus. When you strip out ESSER-funded contracts—money that school districts literally cannot renew because the budget line item no longer exists—true organic growth is often flat or negative.

The Diligence Adjustment: You must segregate ARR into "Core Operating Budget" vs. "Stimulus-Funded." If a district paid for a 3-year license upfront with ESSER III funds in 2023, that revenue stream hits a hard cliff in 2026. In our recent audits, we found that an average of 28% of reported ARR in K-12 SaaS deals was tied to expiring stimulus funds with zero probability of renewal. If you apply a standard 6x-8x revenue multiple to that phantom ARR, you are overpaying by millions.

In EdTech, renewals aren't a contract decision. They're a utilization decision. If the teachers aren't logging in, the district won't log the payment.

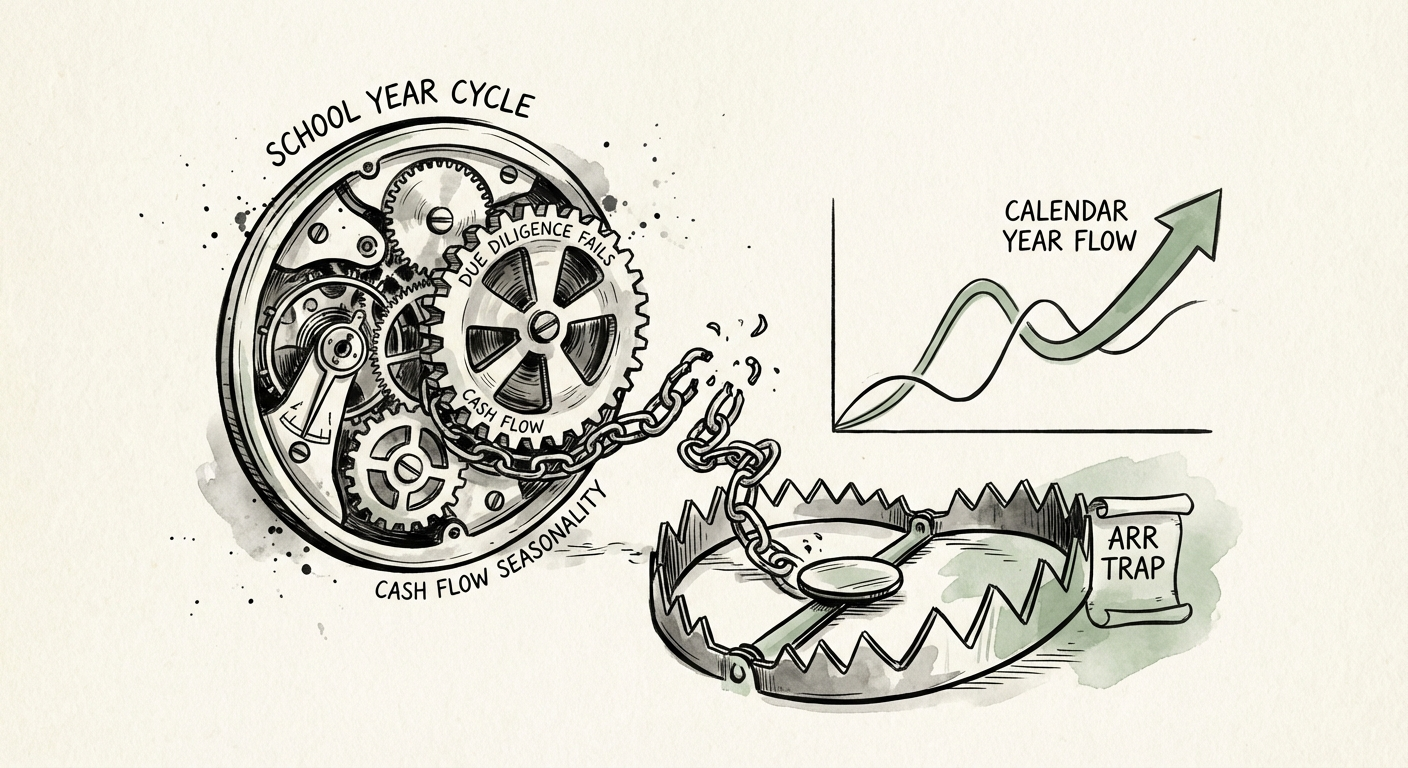

The Seasonality Trap: Why Q3 Bookings Hide Q1 Burn

EdTech has the most violent seasonality of any B2B vertical. The "Back-to-School" (BTS) season in Q3 creates a cash and bookings spike that can mask profound operational inefficiencies during the rest of the year. Founders love to present "Calendar Year" financials, but savvy Operating Partners demand "School Year" (July 1 - June 30) analysis to normalize these distortions.

The most dangerous metric in EdTech is the "implied renewal rate" calculated in Q4. Why? Because districts often make non-renewal decisions in April or May (budget season), but the churn doesn't technically hit the books until the contract expires in June or July. This creates a "churn lag." You might be looking at a dashboard in November showing 95% retention, while 30% of the customer base has already decided to leave next summer.

The 'Summer Melt' Adjustment

In your Quality of Earnings (QofE), you must accrue churn based on notification dates, not contract end dates. If a district notifies of non-renewal in May, that ARR should be written off immediately for forecasting purposes, even if cash was paid through August. Failure to do this leads to the classic EdTech surprise: a Q3 forecast miss because "unexpected" churn hit right before the school year started.

Stale Licenses: Usage as the Only Truth

In Enterprise B2B, a signed contract is usually a safe proxy for value. In EdTech, it is not. District administrators often buy "district-wide site licenses" (e.g., 10,000 seats) that see actual utilization by only 500 teachers. This is "Inactive ARR." It looks like high-quality recurring revenue on the P&L, but it is actually a churn event waiting to happen at the next budget committee meeting.

Valuation multiples in 2026 are bifurcating based on this metric. Companies with high Active User Adoption (>60% of licensed seats active monthly) are trading at premium multiples (8x+ Revenue). Those with "shelfware" metrics (<20% utilization) are seeing multiples compress to 1.5x-2x, regardless of their current ARR.

The Fix: Implement a "Health Score" based on teacher activation, not just administrator logins. If a product isn't embedded in the weekly workflow of the classroom, it will be the first item cut when the district CFO looks for savings to plug the post-ESSER budget gap.