The practical answer

- Short answer

- ServiceNow partners are trading at 15x EBITDA. Learn the market dynamics, valuation drivers, and due diligence red flags fueling the 2026 M&A consolidation wave.

- Best fit

- Industry: IT Services / Private Equity. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 15x EBITDA multiple for 'Elite' ServiceNow partners with proprietary IP and managed services revenue.

The 'New ERP' market opening: Why Capital is Chasing Capacity

If you are an Operating Partner looking at the IT services landscape in 2026, you have likely noticed a bifurcation in the market. Generalist IT consultancies are trading at a respectable 8x-10x EBITDA. Meanwhile, specialized ServiceNow partners are seeing term sheets at 12x, 15x, and even 18x EBITDA. Why the premium?

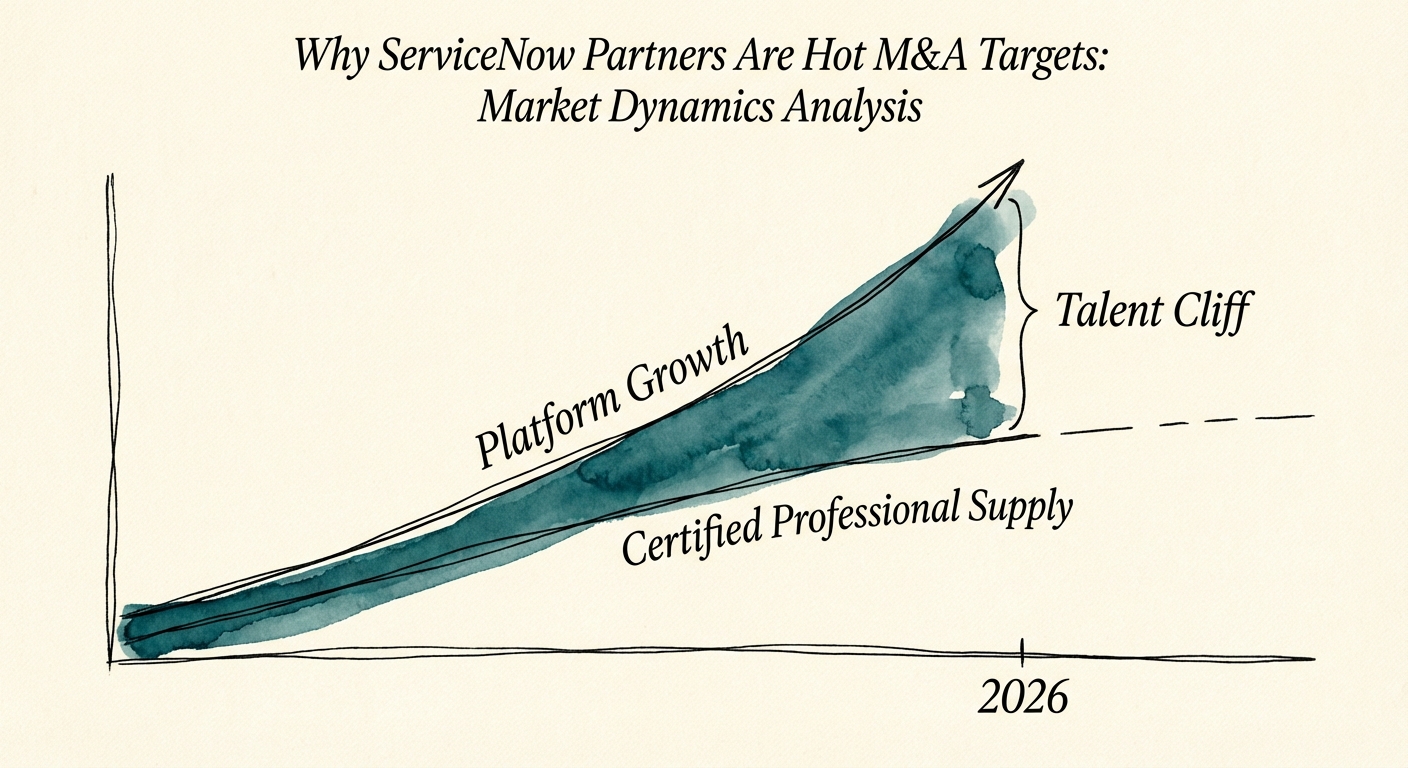

The answer lies in the supply-demand imbalance of competence. ServiceNow isn't just a ticketing system anymore; it has effectively become the "ERP for Work," spanning HR, CSM, Security, and Creator Workflows. With the platform projected to hit $15 billion in revenue by 2026 and 85% of the Fortune 500 locked in, the ecosystem is expanding faster than the talent pool can support.

We are currently facing a "Talent Cliff." Industry reports indicate that 90% of organizations will face critical digital skills shortages by 2025. For a PE sponsor, this changes the investment thesis. You aren't just buying a book of business; you are buying capacity execution. In a market where 51% of hiring managers cannot find qualified talent, an assembled, certified, and proven delivery team is a scarce asset worth a massive premium.

The Consolidation Wave

The market is fragmented, but the roll-up is aggressive. Global SIs are acquiring boutique firms not for their revenue, but to plug the gaping holes in their own delivery benches. If you own a portfolio company in this space, you are sitting on a winning lottery ticket—if you can prove the quality of your revenue.

In 2026, you aren't buying revenue in the ServiceNow ecosystem. You're buying the only asset that matters: proven, billable engineering capacity.

The Valuation Matrix: Staff Aug vs. Strategic Partner

Not all ServiceNow partners are created equal. In my experience advising on exits, I see founders confuse activity with value. They come to the table with $20M in revenue and expect a 15x multiple, only to get hammered down to 6x because 80% of that revenue is low-margin staff augmentation.

Here is the valuation hierarchy we are seeing in 2026 term sheets:

- The Body Shop (6x - 8x EBITDA): Revenue is driven by seat-fill delivery. Low differentiation, high churn, zero IP. You are essentially a recruiting agency with a ServiceNow logo.

- The Project House (8x - 10x EBITDA): You deliver defined outcomes. Margins are better (40%+ gross), but revenue is lumpy. Every January 1st, you start at zero.

- The Managed Services Platform (12x - 14x EBITDA): You have multi-year contracts. You manage the instance, not just build it. Your staff augmentation vs. managed delivery mix leans heavily toward managed. Revenue is predictable; retention is high.

- The "Elite" IP Play (15x+ EBITDA): You have built proprietary apps on the Now Platform (Store Apps) or have deep vertical specialization (e.g., FedRAMP/DoD expertise). You have "productized services." This is where the multiple expansion happens.

The PE Playbook: Smart sponsors are buying "Project Houses" at 8x and transforming them into "Managed Services Platforms" to exit at 14x. That is the arbitrage. But it requires operational discipline that most founder-led firms lack.

Due Diligence Landmines: What Kills the Deal

When we conduct IT services M&A valuation assessments, we look for the skeletons that don't show up on the P&L. In the ServiceNow ecosystem, two specific red flags kill deals faster than anything else.

1. The "Paper Tiger" Bench

ServiceNow certifications are valuable, but they are also gameable. We see partners boasting "200 Certified Professionals," but due diligence reveals that 150 of them are juniors who memorized a test bank and have never touched a production instance. Technical due diligence red flags like this are fatal. Buyers act on billable competency, not badges. If your senior-to-junior ratio is out of whack, your gross margins are a mirage waiting to collapse under delivery failure.

2. The "Franken-Instance" Debt

Did you grow by over-customizing the platform? If your team built custom code instead of using out-of-the-box flow designers, you have saddled your customers with massive technical debt. When ServiceNow drops a major release (Xanadu, Yokohama, etc.), those custom scripts break. Acquirers know this. If your revenue is dependent on maintaining bad code, it's not recurring revenue—it's recurring liability.

The Verdict

The window is open. The multiples are historic. But the buyers are sophisticated. They are speaking fluent EBITDA and fluent DevOps. Ensure your house is in order before you invite them in.