The practical answer

- Short answer

- A diagnostic guide for cleaning up financial reporting before a services firm exit. Learn how to fix ASC 606 gaps, validate EBITDA add-backs, and survive the Quality of Earnings (QofE) audit.

- Best fit

- Industry: Professional Services. Function: Finance

- Operating path

- Process Documentation → Operational Excellence → Transaction Execution Services

- Key metric

- 15% Average valuation discount applied to services firms with 'messy' financial reporting during due diligence re-trades.

The 'Shoebox' Discount: Why Messy Books Kill Premium Multiples

In the high-stakes environment of 2026 M&A, the fastest way to change a deal isn't a declining sales forecast—it's low-quality financial reporting. According to recent data, 40% of CFOs do not completely trust their own organization's financial data. If your finance leader has doubts, your potential acquirer will have nightmares.

For professional services firms, this typically manifests as the "Cash Basis Trap." You run the business on bank balance and invoices sent, but buyers value it on accrual-based EBITDA. The gap between these two realities is where deals go to die. When a Private Equity (PE) firm initiates a Quality of Earnings (QofE) study, they aren't just checking your math; they are testing the integrity of your operations. A ledger riddled with uncategorized expenses, inconsistent revenue recognition, and aggressive personal add-backs signals to a buyer that they aren't buying a business—they're buying a cleanup project.

You can put a hard number on this negligence. In lower middle-market deals, a lack of financial clarity typically results in a 15% to 20% valuation haircut during the exclusivity period, often called the "re-trade." Buyers use every discovery of sloppy accounting as leverage to lower the purchase price, knowing you are already emotionally committed to the exit.

Financials that contain false or misleading EBITDA addbacks increase buyers' skepticism... likely to result in discounts to the financial projections and the buyer's ultimate valuation.

The Three Pillars of Financial Hygiene: A Cleanup Framework

To survive scrutiny and defend your multiple, you must transition your reporting from "tax-efficient" to "audit-ready." This requires a systematic cleanup across three critical vectors.

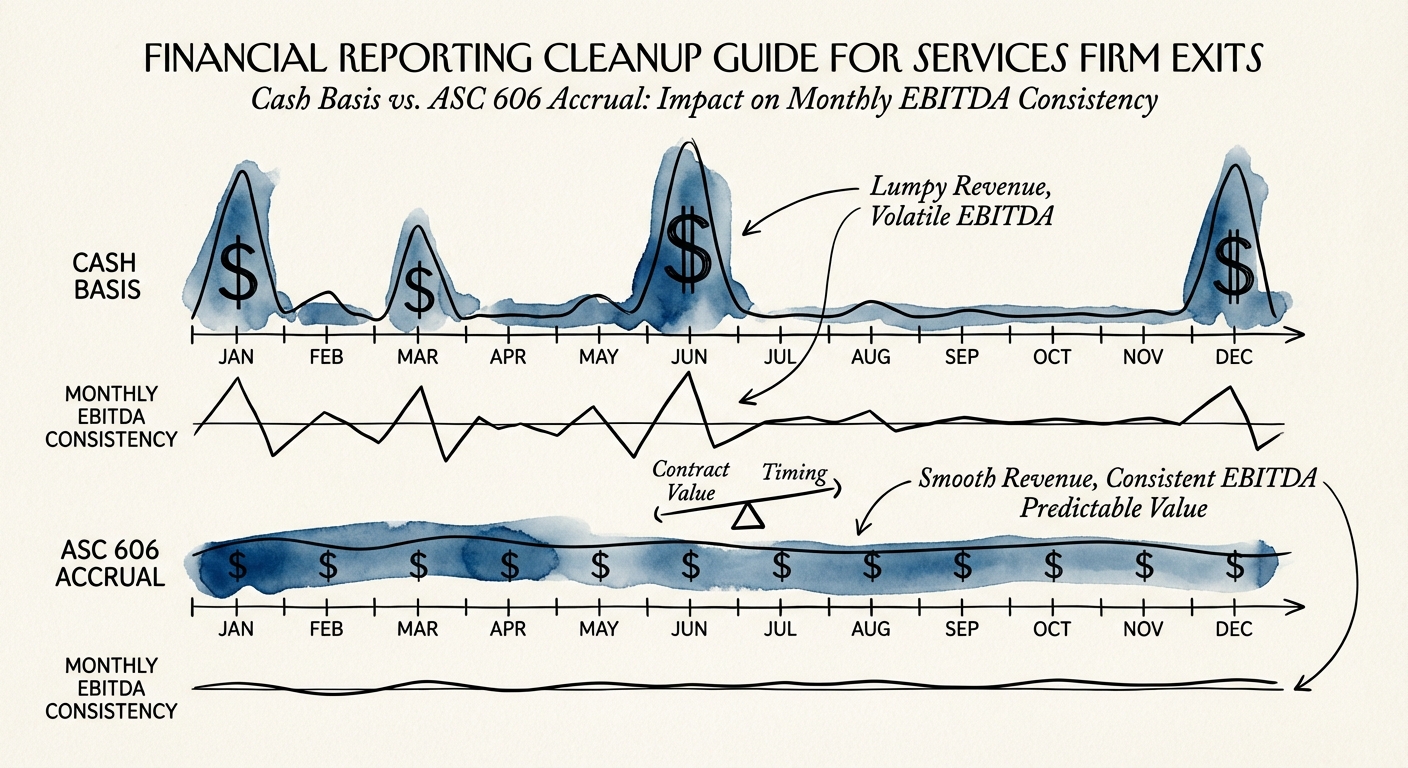

1. Revenue Recognition (ASC 606) Compliance

For services firms, the shift to ASC 606 is not optional. The old method of recognizing revenue when you invoice (or when you get paid) is unacceptable in M&A. Buyers demand to see revenue recognized as control transfers to the customer. If you bill $100,000 upfront for a 12-month implementation project, you cannot book $100,000 in Month 1. You must recognize it ratably or based on milestones. Failing to do this creates "lumpy" revenue charts that terrify investors and obscure the true run-rate EBITDA.

2. The 'Red Face' Test for EBITDA Add-Backs

Adjusted EBITDA is the currency of your exit, but aggressive add-backs counterfeit that currency. In 2026, buyers are rejecting the "kitchen sink" approach. Legitimate add-backs (one-time legal fees, non-recurring severance) are acceptable. But trying to add back the CEO's entire salary because they "plan to retire"—without accounting for the cost of a replacement—is a red flag. Apply the "Red Face Test": Can you explain this adjustment to a skeptical investment committee without blushing? If not, remove it before the QofE begins.

3. Gross Margin Purity (COGS vs. Opex)

Services firms often commingle delivery costs with operating expenses. If your delivery team's salaries are buried in SG&A rather than Cost of Goods Sold (COGS), your Gross Margin looks artificially high. A buyer will eventually reclassify these expenses, causing your Gross Margin to plummet overnight. This reclassification doesn't change EBITDA, but it destroys your narrative of being a "high-margin, scalable platform" and rebrands you as a "labor-intensive body shop."

The 'Mock Audit' Strategy: Pre-Empting the QofE

The most effective defense against a painful due diligence process is to conduct a "sell-side" QofE or a mock audit 6 to 12 months before going to market. This involves bringing in an external financial consultant to tear apart your books exactly as a buyer would.

This proactive step accomplishes two goals. First, it identifies the "skeletons" (like that forgotten software license liability or the undocumented verbal agreements with partners) while you still have time to fix them. Second, it produces a "Databook"—a structured, defensible set of financials that you can hand to a buyer on Day 1. This signals competence and transparency, shifting the power dynamic in your favor.

Remember, in M&A, time kills all deals. Every day a buyer spends untangling your QuickBooks file is a day they spend rethinking the valuation. Clean financials are not just compliance; they are a competitive advantage that accelerates the path to close.