The practical answer

- Short answer

- Stop overpaying for 'ghost revenue.' This diagnostic framework helps PE investors stress-test IT consulting backlogs, calculate leakage rates, and adjust valuations before the deal closes.

- Best fit

- Industry: Private Equity. Function: Finance

- Operating path

- Process Documentation → Operational Excellence → Transaction Execution Services

- Key metric

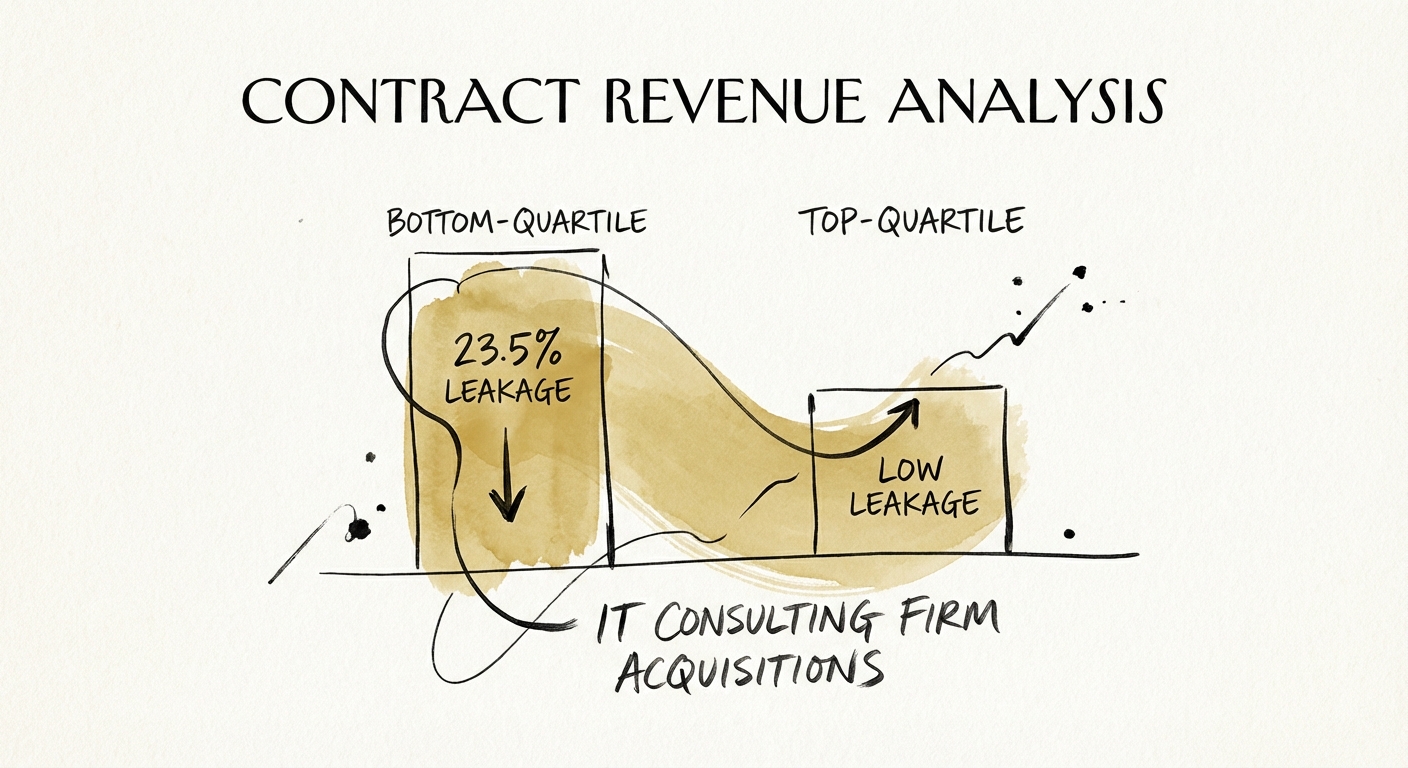

- 23.5% Average 'Backlog Leakage' for bottom-quartile services firms, representing signed value that never converts to revenue.

The Backlog Illusion: Hard Commitments vs. Soft Promises

In the high-stakes world of IT consulting acquisitions, backlog is often treated as a proxy for future revenue—a comforting bridge between the uncertainty of the pipeline and the solidity of the P&L. However, for private equity sponsors, treating all backlog as equal is a valuation error that can cost millions. Data from the 2024 Architecture & Engineering Business Benchmarks indicates that bottom-quartile firms suffer from a realization rate of just 76.5%, implying a 23.5% Backlog Leakage Rate. This means nearly a quarter of the signed, celebrated work in the data room will never convert to cash.

The Taxonomy of Ghost Revenue

The first step in contract revenue analysis is dismantling the monolithic definition of 'backlog' found in the CIM (Confidential Information Memorandum). In many founder-led IT services firms, the definition of backlog is loose, often conflating three distinct categories:

- Hard Backlog (Funded & Scheduled): This is the only true asset. These are signed Statements of Work (SOWs) with allocated budget, a defined start date, and a penalty-laden cancellation clause.

- Soft Backlog (Contracted but Unfunded): This is where the 'ghost revenue' lives. These are Master Services Agreements (MSAs) with 'intended' spend but no purchase order, or IDIQ (Indefinite Delivery, Indefinite Quantity) contracts where the vendor is merely eligible to compete for work.

- Phantom Backlog (Verbal & Projected): Founders often include 'verbal commits' or 'automatic renewals' in their backlog calculations. In a downturn or post-acquisition integration, these evaporate instantly.

For a PE buyer, the danger lies in applying a standard EBITDA multiple (typically 11-13x for IT services) to revenue that has a 23.5% probability of vanishing. If you acquire a firm with $10M in backlog, and $2.35M of that is 'soft,' you haven't just lost revenue—you've potentially overpaid by $25M+ in Enterprise Value.

Realization Rate is a clear indication of whether you are earning the right revenue compared to effort. Bottom quartile firms see an average Realization Rate of 76.5%, highlighting massive leakage in the transition from signed contract to billed invoice.

The 5-Point Backlog Diagnostic

To determine the true quality of a target's backlog, you must move beyond the spreadsheet and audit the underlying contract structures. This diagnostic process separates the 'Hard' backlog from the 'Soft' and calculates a defensible Adjusted Backlog Value for the Quality of Earnings (QofE) report.

1. The Cancellation Clause Audit

Review the 'Termination for Convenience' clauses in the top 20 contracts. A contract that allows the client to cancel with 30 days' notice without penalty is not backlog; it is a 30-day recurring revenue stream. Benchmark: Hard backlog requires a termination fee equal to at least 20% of the remaining contract value or 90 days of guaranteed billing.

2. The 'Start Date Drift' Analysis

Measure the historical gap between the scheduled start date in the SOW and the actual first billable hour. In many IT consultancies, this 'drift' averages 45-60 days due to client-side delays (provisioning, access rights, onboarding). If the target's forecast assumes Day 1 billing for all backlog, they are overstating Year 1 revenue by 12-16%. Revenue recognition delays are a primary driver of post-close misses.

3. The Realization Rate Test

Calculate the firm's historical Realization Rate (Revenue / Contract Value) for closed projects. If the firm consistently burns 100% of the budget but only recognizes 85% of the revenue due to write-offs, scope creep, or 'investment hours,' apply that same discount to the current backlog. Do not accept the founder's assurance that 'we fixed those delivery issues.'

4. The 'Inactive Project' filter

Identify contracts in the backlog that have had no billable hours logged in the last 90 days. These are 'Inactive Projects'—technically active, but practically dead. They should be removed from the valuation model entirely or discounted by 90%.

5. The Concentration Risk Stress Test

If 40% of the backlog sits with a single client, apply a Concentration Discount. In the event of an acquisition, large enterprise clients often pause or review vendor relationships, putting this specific tranche of backlog at the highest risk of 'convenience' termination.

Valuation Impact: From Analysis to Adjustment

Once you have diagnosed the quality of the backlog, the final step is to adjust the valuation. This is not about being punitive; it's about accuracy. A rigorous contract revenue analysis allows you to present a Backlog Quality Scorecard to the investment committee, justifying a lower multiple or a structured earnout.

The 'Haircut' Model

Instead of a flat discount, apply tiered risk weightings to the backlog:

- Tier 1 (Signed SOW + PO + Active): 100% Valuation Attribution.

- Tier 2 (Signed SOW + No PO): 75% Valuation Attribution.

- Tier 3 (MSA + Verbal Start Date): 25% Valuation Attribution.

- Tier 4 (Projected Renewals): 0% Valuation Attribution (Treat as Upside/Earnout only).

This nuanced approach protects your downside while still rewarding the seller for high-quality, committed revenue. It also aligns the seller's incentives: if they want full value for Tier 3 backlog, they need to get it signed and funded before close.

Defending the Multiple

In a market where IT services firms trade at high multiples, the quality of the backlog is the only true defense against overpaying. By exposing the 23.5% leakage risk, you not only negotiate a better price but also build a Quality of Earnings defense that holds up under scrutiny. Remember, you are buying the future cash flows, not the past promises. Ensure those flows are contractually secured before you sign the check.