The practical answer

- Short answer

- Stop hiding technical debt in due diligence. Learn how to position legacy code as a 'shovel-ready' modernization opportunity that drives higher exit multiples.

- Best fit

- Industry: Private Equity / Technology. Function: Engineering / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 30% Higher acquisition costs incurred by companies with unaddressed, strategic technical debt.

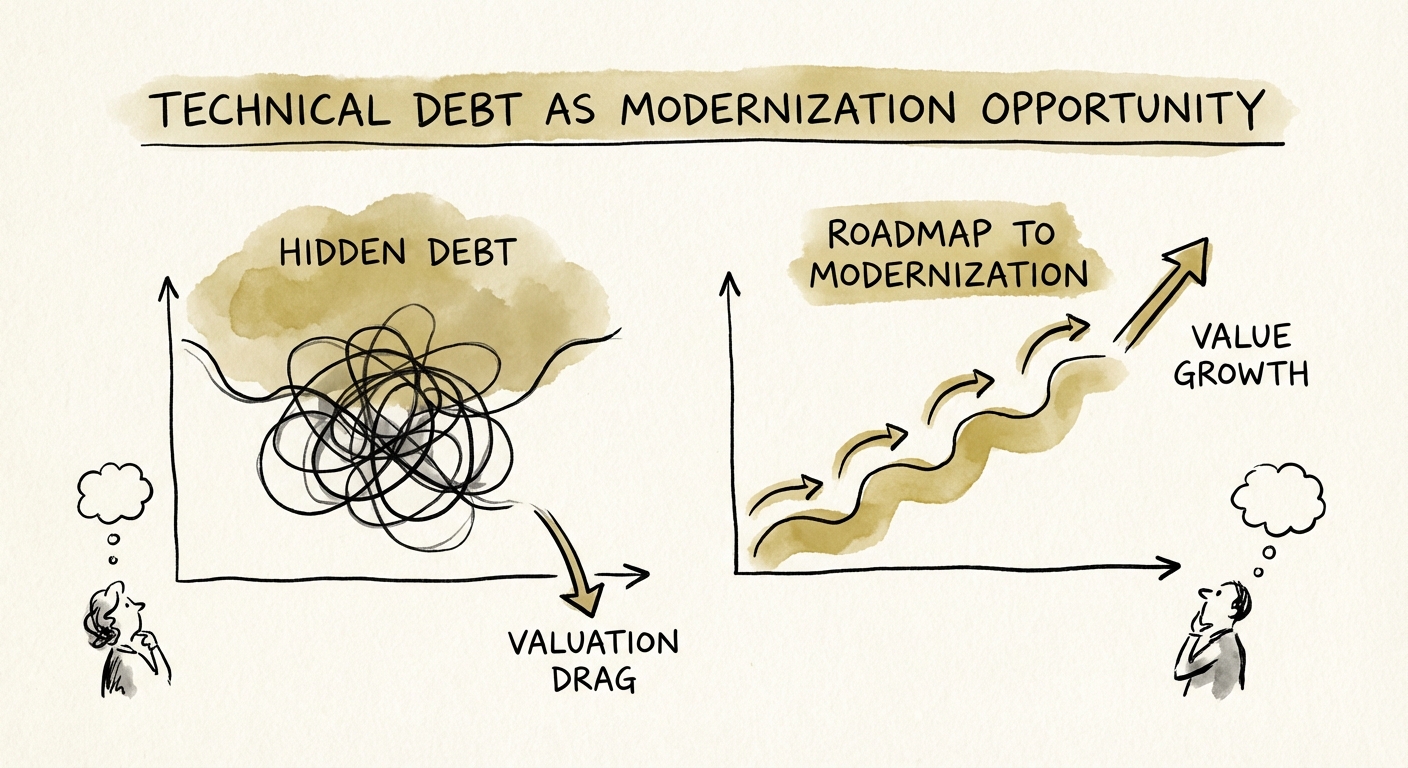

The Liability Mindset vs. The Opportunity Thesis

In the disciplined valuation environment of 2026, where software EBITDA multiples have corrected to roughly 12.4x from their 2021 peaks, technical debt is no longer just an engineering headache—it is a direct deduction from Enterprise Value. Research indicates that companies with significant unaddressed technical debt can see valuation haircuts of up to 20% during due diligence. The buyer’s logic is simple: they calculate the "cost of remediation" (hiring consultants, rewriting code, pausing features) and subtract it dollar-for-dollar from the deal price.

However, savvy founders and CTOs can flip this narrative. The difference between a 20% discount and a "value creation" premium lies in how the debt is categorized. "Sloppy Debt" (undocumented hacks, lack of tests) is a liability. "Strategic Debt"—conscious decisions to defer modernization in favor of growth—can be positioned as a Deferred Modernization Opportunity. If you present a legacy monolith not as a "mess" but as a "pre-microservices asset" with a validated, scoped, and costed roadmap for refactoring, you transform the conversation. You are effectively handing the Private Equity buyer a "shovel-ready" value creation plan.

The Psychology of the PE Buyer

Private Equity operating partners are hunting for margin expansion levers. A pristine tech stack offers little "alpha"—it is priced in. A stack with identifiable inefficiencies that can be fixed to reduce cloud costs by 30% or accelerate feature velocity by 2x is an investment thesis. Your goal is to prove that the heavy lifting—the discovery and architecting of the solution—is already done.

Private Equity doesn't buy 'perfect' companies; they buy companies with 'fixable' problems that generate returns. Your technical debt isn't the problem—the lack of a priced plan to fix it is.

The 'Shovel-Ready' Roadmap: A Documentation Strategy

To successfully position technical debt as an asset, you must move beyond vague admissions of "we need to refactor" to a rigorous, quantified roadmap. Buyers fear uncertainty more than they fear cost. A $2M rewrite is a known quantity; a "spaghetti code" black box is an infinite risk.

1. Vertical Modernization vs. The 'Grand Rewrite'

Avoid presenting a "Big Bang" rewrite, which PE firms view as high-risk execution failure. Instead, present a Vertical Modernization strategy. Show how you have decoupled specific high-value domains (e.g., billing, auth, reporting) into independent services. This demonstrates that you have already established the pattern for modernization. Data shows that incremental, domain-driven refactoring reduces risk and accelerates time-to-value compared to horizontal layer rewrites.

2. Quantify the 'Modernization Arbitrage'

Attach a dollar value to the modernization. Do not just say "this will improve code quality." Say: "Executing this 12-month containerization roadmap will reduce Azure spend by $150k annually and decrease customer onboarding time from 3 weeks to 4 days." This converts technical debt from an abstract concept into an EBITDA bridge. By quantifying the ROI, you allow the buyer to model the modernization as a post-close synergy rather than a pre-close price reduction.

Execution Proof: Metrics That Validate Capability

A roadmap is only as good as the team's ability to execute it. In due diligence, you must prove that your engineering organization has the "metabolic rate" to handle modernization while maintaining commercial growth. Use specific metrics to evidence this capability.

The Developer Coefficient

Highlight your Cycle Time and Defect Escape Rate trends over the last 18 months. If your tech debt is high, but your cycle time is stable or improving due to better CI/CD practices, you prove that the debt is contained. Conversely, if cycle times are blowing out, the buyer will assume the asset is "frozen."

Strategic Debt vs. Interest Payments

Finally, categorize your engineering spend. Show exactly what percentage of effort goes to "keeping the lights on" (KTLO) versus "innovation." A high KTLO is acceptable if you can show a trend line where recent modernization efforts have begun to drive it down. This trajectory is the "growth story" the buyer is buying. You are selling them the bottom of the curve, allowing them to capture the upside of the efficiency gains.