The practical answer

- Short answer

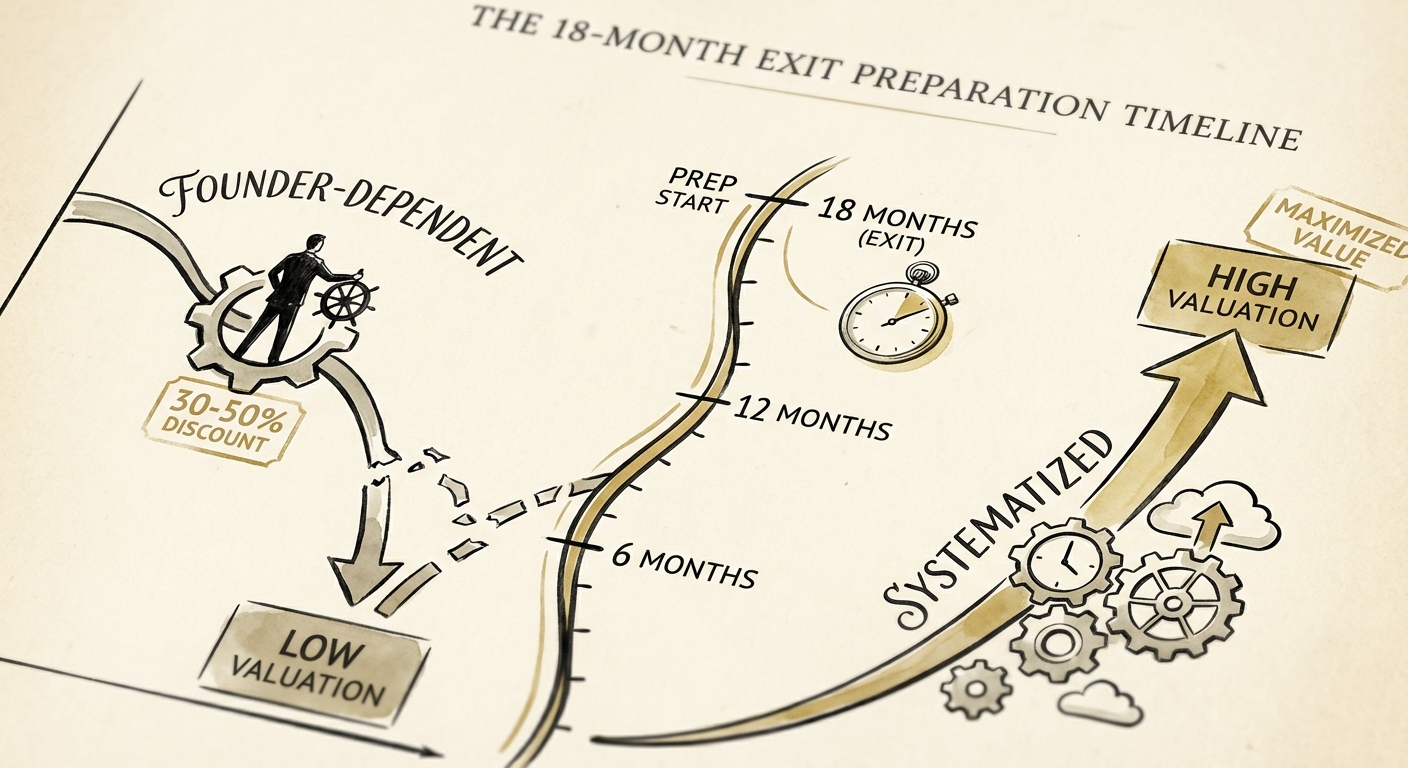

- Don't sell your company for a discount. This 18-month exit preparation timeline covers financial hygiene, founder extraction, and technical due diligence to maximize valuation.

- Best fit

- Industry: B2B SaaS & Tech Services. Function: CEO / Board Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 11.7x Median revenue multiple for SaaS companies with NRR > 120% (Source: Software Equity Group, 2025)

The Difference Between "Selling" and "Being Bought"

There is a fundamental misunderstanding among founders about how exits happen. You do not wake up one day, decide to sell, and hand the keys to a Private Equity firm for 10x ARR. That is an unsupported assumption. In the current 2025-2026 market, you are either prepared to be bought, or you are selling from a position of weakness.

The difference is mathematical. Data from 2025 shows that founder-dependent businesses—where the CEO is still the chief rainmaker or technical lead—trade at a 30-50% discount compared to their systematized peers. If you are doing $20M ARR, that dependency is costing you $40M-$60M in enterprise value. That is the "Founder Discount."

To erase that discount, you need time. Specifically, you need 18 months. Why 18? Because that is the minimum viable window to turn "tribal knowledge" into "transferable assets" and show 12 months of clean trailing-twelve-month (TTM) financial performance that matches your forecast. If you try to rush this process in 6 months, you will fail Quality of Earnings (QofE), and your deal will die on the table.

You do not sell your company. You position it to be bought. The difference is 18 months of deliberate engineering.

Phase 1: 18-12 Months Out (The "Clean Up")

Metric to Watch: Founder Extraction Score

Your first priority is not growth; it is Founder Extraction. Buyers pay for a business, not a job. If the revenue stops when you go on vacation, you don't own a business; you own a high-paying freelance gig.

- Operational Extraction: Document the "Company Brain." Buyers in 2025 are paying premiums for documented SOPs. If your sales process, code deployment, and customer onboarding exist only in your head, they are valueless assets in an M&A context.

- Financial Hygiene: Stop running the business for tax minimization and start running it for EBITDA maximization. You need to identify every personal expense, one-time cost, and non-recurring fee now so they can be defended as "add-backs" later. Waiting until the Letter of Intent (LOI) to explain why your country club membership is a business expense is a red flag that kills trust.

Phase 2: 12-6 Months Out (The "Scale Up")

Metric to Watch: Net Revenue Retention (NRR) > 110%

Once the foundation is stable, you must prove the engine works. In 2025, growth at all costs is dead. The new king is efficient growth. SaaS companies with NRR above 120% are seeing valuation multiples upwards of 11.7x revenue, while those below 100% struggle to find bids at 4x.

Use this window to fix your Customer Success function. A leaky bucket destroys valuation faster than slow growth. Implement quarterly business reviews (QBRs) that actually drive value, not just check a box. Ensure your "upsell" revenue is systematic, not accidental.

Phase 3: 6-0 Months Out (The "Dress Up")

Metric to Watch: Forecast Accuracy > 90%

This is the final sprint. You are now "pre-market." Your goal here is credibility. When you tell a banker or a PE associate that you will hit $5M in Q3, you must hit $5.0M or $5.1M. If you hit $4.2M, you look like you don't understand your own business. If you hit $8M, you look like you have no control over your pipeline.

- The Data Room: Do not wait for the request list. Build your Data Room now. Technical debt assessments, IP assignment agreements for every contractor you've ever hired, and clean cap tables must be ready.

- Technical Due Diligence (TDD): This is where 46% of tech deals fail. Buyers will scan your code. If they find high-severity vulnerabilities or massive technical debt, they will re-trade the deal or walk away. Run your own scan first and fix the critical issues.

The 18-month timeline is not about painting a pretty picture; it is about engineering a predictable asset. The market doesn't pay for potential; it pays for proof.