The practical answer

- Short answer

- ServiceNow's 2025 partner program overhaul reduces Elite tiers and demands AI specialization. Here is the revenue impact diagnostic for founders.

- Best fit

- Industry: IT Services. Function: All

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

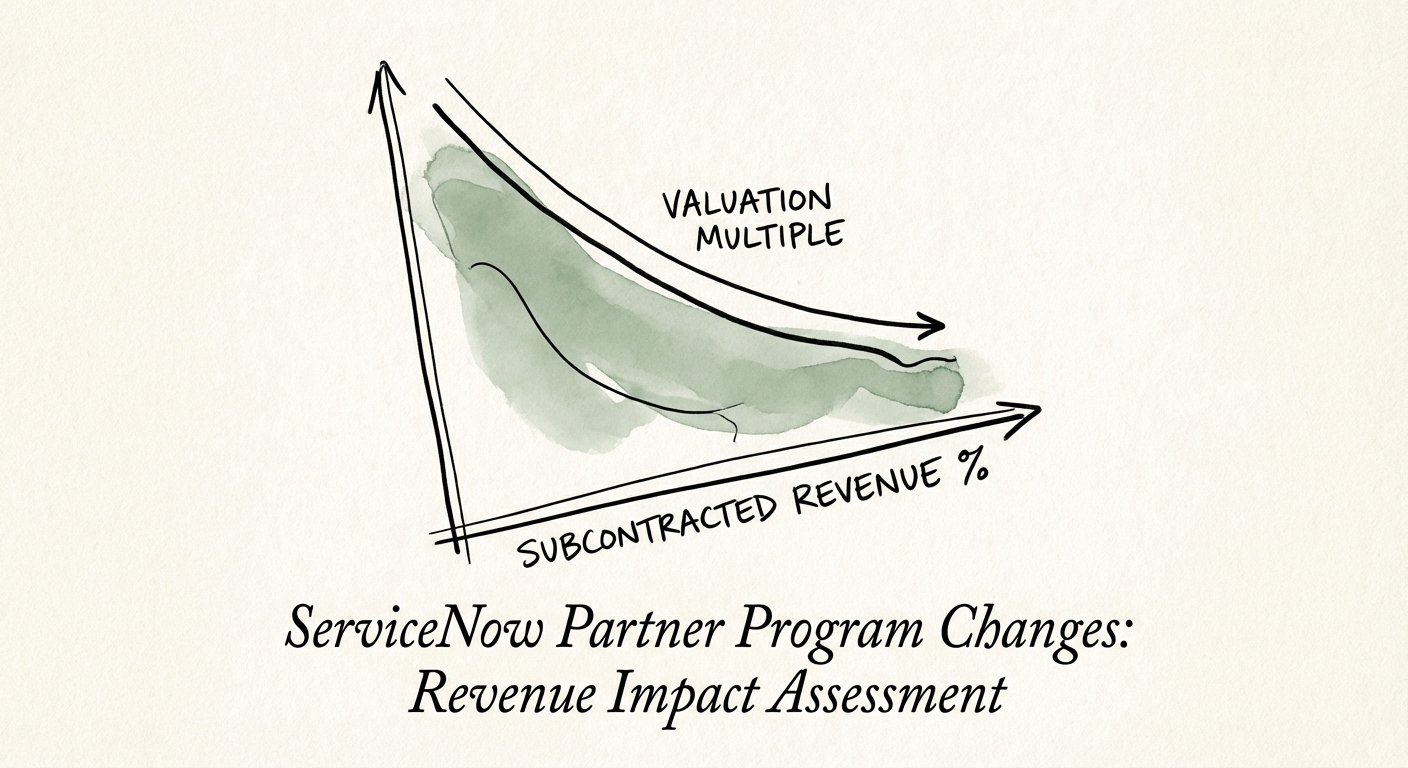

- 35% Valuation discount for partners with >40% subcontracted revenue

The 'Middle Class' of Partners Is Being Evicted

If you are a ServiceNow partner generating between $10M and $50M in revenue, you are standing on a burning platform. For years, the playbook was simple: stack certifications, hit your ACV (Annual Contract Value) sourcing targets, and claw your way to 'Elite' status. That ladder has been pulled up.

In early 2025, ServiceNow announced a restructuring that drastically reduces the number of partners in the Elite tier—reports indicate a drop from roughly 134 to fewer than 80 globally. This isn't just a badge change; it's a market clearing event. The ecosystem is bifurcating into two distinct species: Global Elites (like Infosys and Cognizant, who can invest millions in 'Now Assist' GenAI practices) and Niche Specialists.

The danger zone is the middle. If you are a generalist implementation firm without a specific industry vertical or a verified GenAI product line achievement (PLA), you are now invisible to the new AI-driven partner matchmaking engine. You aren't just losing status; you are losing the algorithmic war for deal flow.

You can't 'relationship' your way into a deal when the AI matchmaking engine excludes you for lacking a GenAI badge. The algorithm doesn't care about your golf game.

The Subcontracting Trap: Revenue vs. Valuation

One of the most seductive changes in the 2025 program is the new Subcontracting Credit. ServiceNow now formally recognizes and rewards Global Elite partners for utilizing smaller partners to deliver work. On the surface, this looks like a lifeline: you don't have to source the ACV, you just deliver the hours.

Do not fall for this if you want an exit.

When you shift your revenue mix from 'Prime' (direct customer paper) to 'Sub' (papering through a GSI), you trigger a valuation collapse. In the eyes of a PE buyer or strategic acquirer, you are no longer a consulting firm with 12x EBITDA potential; you are a staffing agency with 4x EBITDA potential. You typically lose:

- Account Control: The GSI owns the renewal and the C-suite relationship.

- Margin: You are taking a rate card haircut to fit under the Prime's margin stack.

- IP Attribution: Your innovative work gets badged as the Prime's success story.

Our data shows that services firms with >40% subcontracted revenue trade at a 35% discount compared to those with direct customer relationships.

Diagnostic: Is Your Practice Underwater?

You need to run a 'Program Economics' audit immediately. Stop looking at your top-line revenue growth and look at your Cost of Partner Compliance (CoPC). The new program requires 'Product Line Achievements' in GenAI, which means expensive talent and non-billable training hours.

The 5-Point Health Check:

- PLA Ratio: Do you have at least one 'Now Assist' Product Line Achievement? (If no, your win rate will drop ~35% in 2025).

- Source vs. Influence: Is your Partner-Sourced ACV dropping while your 'Influence' stays high? This indicates you are being pushed out of the deal cycle.

- Subcontracting Mix: Is your sub-revenue exceeding 20% of total revenue? (Warning zone).

- CSAT Velocity: Is your CSAT strictly above 4.2? The new program rigorously cuts anyone below this line.

- Impact Attachment: Are you wrapping services around the 'ServiceNow Impact' product? This is the only 'safe harbor' for high-margin advisory work right now.

If you fail more than two of these checks, you need to restructure your GTM motion immediately. You cannot 'deliver' your way out of a structural programmatic disadvantage.