The practical answer

- Short answer

- New 2026 Azure Partner Program rules have killed the resale margin. Learn why the $1M CSP Direct cliff and MACC incentives mean you must pivot to IP and consumption now.

- Best fit

- Industry: Cloud Services / MSP. Function: Finance & Operations

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 70% Increase in Azure outcome-based incentives for FY26, shifting profit pools from resale to consumption.

The $1 Million Revenue Cliff: Forced Migration is Here

If you are a CSP Direct Bill partner generating less than $1M in trailing twelve-month (TTM) revenue, your business model just received an eviction notice. Microsoft’s FY26 program updates have raised the Direct Bill requirement from $300,000 to $1,000,000. This isn't a suggestion; it is a hard floor.

For years, boutique MSPs clung to Direct Bill status to own the billing relationship and capture that extra 2-4% of margin that otherwise goes to Distributors (Indirect Providers). That era is over. If you miss this threshold, you will be forcibly offboarded to Indirect Reseller status. The financial impact is immediate:

- Margin Compression: You lose the direct incentive spread, typically handing over 3-5% of top-line revenue to a Distributor like Pax8, TD SYNNEX, or Ingram Micro.

- Valuation Impact: Direct Bill status was a hallmark of maturity. Losing it signals to acquirers that you are a "sub-scale" asset, potentially compressing your revenue multiple by a full turn.

However, the real danger isn't the billing change—it's the distraction. While you fight to retain a low-margin billing function, your competitors are pivoting to where the new money is: Azure Consumed Revenue (ACR) and Marketplace IP.

Microsoft is no longer paying you to sell the car. They are paying you only when the customer drives it. If your P&L is built on parking fees, you're finished.

The New "Consumption King" Reality

Stop looking at your resale margin line item. In 2026, it is irrelevant. Microsoft has aggressively pivoted its incentive structure to reward consumption and specialization over transaction volume. The headline number you need to know is 70%. That is the year-over-year increase in Azure outcome-based incentives for FY26.

The message is brutal but clear: Microsoft does not pay you to sell a license; they pay you to ensure the customer uses it. This shift exposes a critical weakness in most MSP financial models. If your P&L relies on the spread between wholesale and retail licensing, your EBITDA is effectively on a timer. The new incentives favor partners who hold advanced specializations (Data & AI, Digital & App Innovation) and drive actual workload consumption.

The "25-Point" Trap

There is a deceptive "win" in the new rules: Indirect Resellers can now earn backend rebates with just 25 points in a solution area (down from the full 70-point designation). Do not celebrate this. It is a consolation prize for the sub-scale market. The premium incentives—the ones that actually move the needle on net income—are reserved for partners hitting the full Solution Partner designations and driving specific high-value workloads like AI and Fabric.

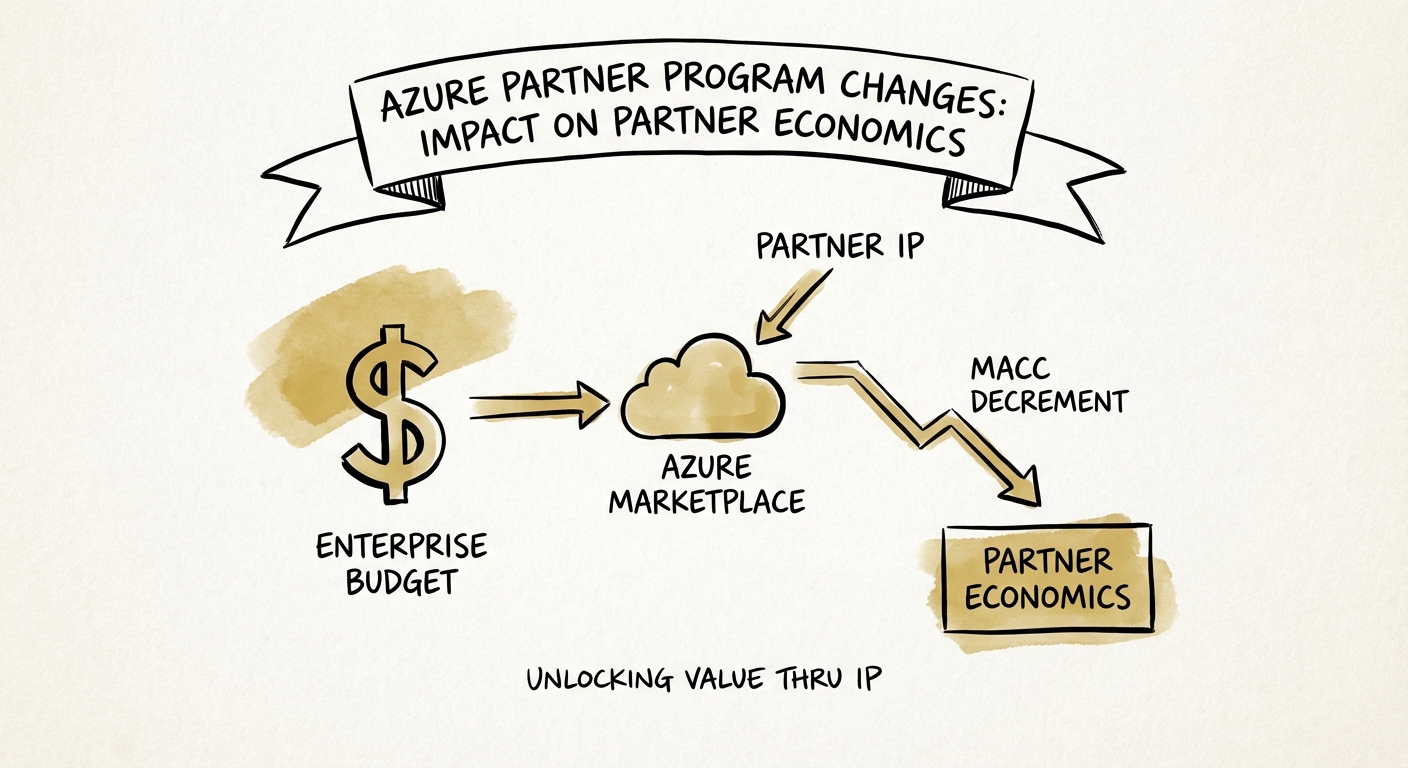

The Marketplace Multiplier: Tapping the MACC

If you do not have a transactable offer on the Azure Marketplace, you are invisible to enterprise buyers. The single most powerful economic lever in the Microsoft ecosystem right now is the Microsoft Azure Consumption Commitment (MACC).

Enterprise CIOs are sitting on millions in committed Azure spend that they must use or lose. Microsoft has changed the game by allowing 100% of eligible partner solution costs to count toward this commitment (MACC decrement). This effectively makes your software or managed service "free" to the budget holder, as they are paying with pre-committed dollars.

The economics of this channel are superior to traditional resale:

- Fee Reduction: The standard marketplace fee is 3% (compared to 20% legacy), and for renewals, Microsoft has introduced a 50% discount on agency fees.

- Deal Velocity: Marketplace deals close 40% faster because legal and procurement hurdles are bypassed via the standard Microsoft commercial contract.

- Co-Sell Gravity: Microsoft sellers are now compensated on MACC consumption. If your deal burns down MACC, the Microsoft rep becomes your unpaid sales champion.

The Verdict: The "Reseller" is a dying breed. The "Owner of Workloads" is the new king. If you are not pivoting your financial infrastructure to track ACR and MACC burn-down, you are optimizing for a business model that expired in 2024.