The practical answer

- Short answer

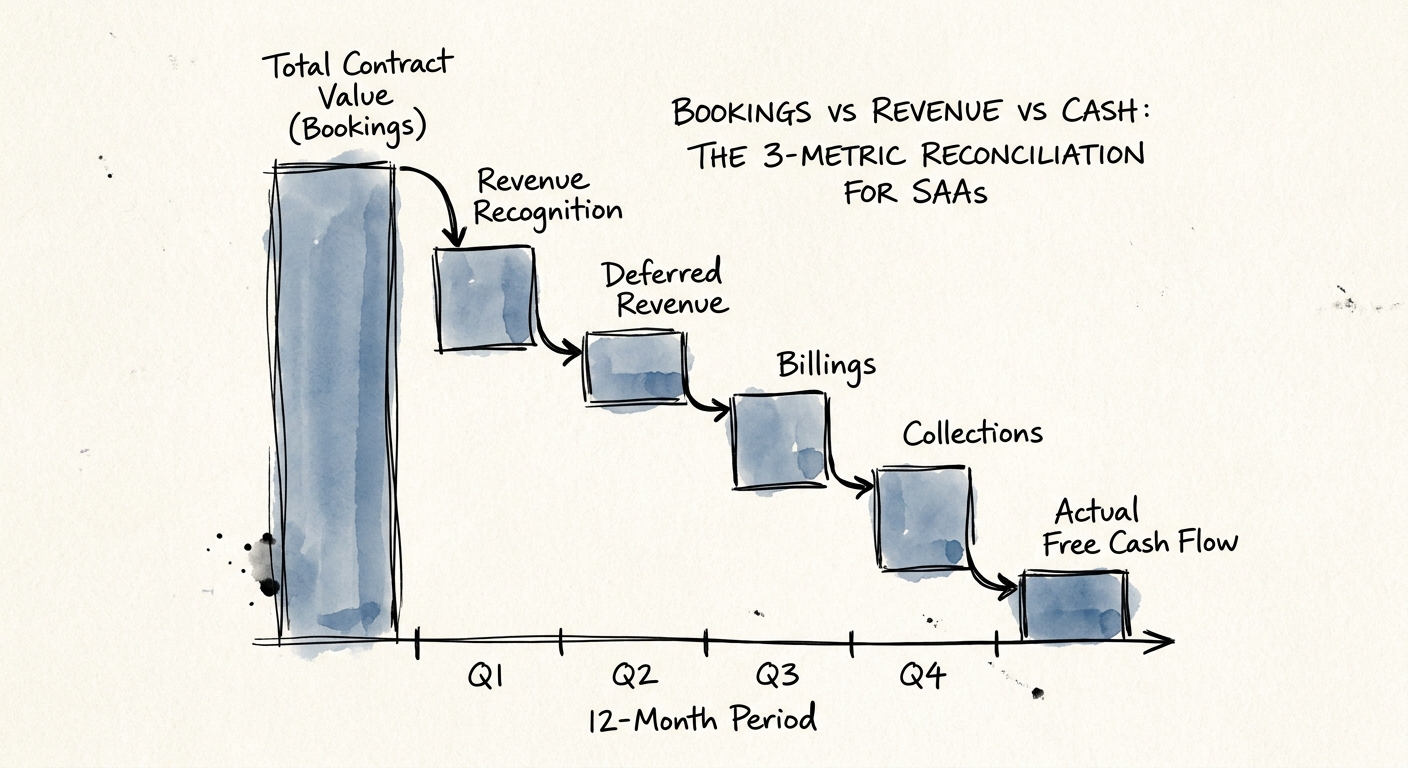

- A signed $300K SaaS deal can show full contract value, a sliver of revenue, and negative cash in the same week. Here's how to reconcile bookings, revenue, and cash before diligence does it for you.

- Best fit

- Industry: Software as a Service. Function: Finance & Operations

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 72 Average Days Sales Outstanding (DSO) in B2B SaaS for Q1 2026, up from 58 days in 2023.

The same quarter, three different companies

Pull three reports for the quarter you just closed. Open the pipeline view in your CRM: it says you did $12 million. Open the income statement your accountant prepared: it says you earned $2.1 million. Open the bank app on your phone: cash is down for the period. Three documents, one quarter, and they describe three companies that share nothing but a logo. The CRM company is winning. The income-statement company is fine. The bank-statement company is quietly running out of air.

That divergence is not an error to be cleaned up later. It is the structural reality of selling multi-year software on enterprise terms, and the day a buyer's Quality of Earnings team sits down with your numbers, the only question that matters is which of the three companies they decide is real. They always pick the smallest one. Your job, long before the data room opens, is to be able to walk any one of those numbers to the other two without flinching.

Here is where the gap actually opens. A rep closes a three-year, $300,000 contract — call it a 40-person logistics-software company landing a mid-market account. Bookings register $300,000 the instant the signature lands; that is Total Contract Value, a legal promise to pay, nothing more. Then the cash side fires in the wrong direction. KeyBanc Capital Markets data puts standard SaaS commissions at roughly 10–12% of annual contract value, paid out inside the first 30 days. So you wire the rep their commission this month. If that customer negotiated quarterly or annual-in-arrears billing — and enterprise buyers always do — your cash for the deal is negative before a single dollar of theirs clears. You just financed your own customer's purchase, at a rate they set.

The reason this stays hidden is that board decks are built to hide it. Bookings growth gets the title slide; the working-capital hole it digs gets buried three pages into the appendix, if it appears at all. Founders are not lying — they genuinely believe a signed TCV is money in the building. It is the opposite: a multi-year deal with a great-looking contract value and semi-annual billing in arrears is you operating as an interest-free lender to a company larger than yours. The fix starts with refusing to let one number stand in for the other three.

Pull three reports for the same quarter — your CRM, your income statement, your bank balance — and you get three different companies. A buyer will pick the smallest one and call it the truth.

What the income statement is actually allowed to say

Of the three companies, the income-statement one is the most misunderstood, because revenue does not track either of the events founders assume it does. You do not earn it when the contract is signed. You do not earn it when the cash arrives. Under ASC 606 you earn it only as the software is actually delivered, month by month, as the customer uses what they paid for. That single rule is what tears the CRM number away from the audited number.

Run it concretely. A $120,000 annual contract is signed and paid in full on December 1. Your CRM logs $120,000 in bookings. Your bank shows $120,000 in. But the December 31 income statement is permitted to recognize exactly $10,000 — one month of service. The other $110,000 lands on the balance sheet as deferred revenue, which is a liability, because you now owe the customer eleven months of software. Notice what just happened to your cash: it is highest at the exact moment your recognized revenue is lowest. The bank looks fantastic and the P&L looks thin, and both are correct simultaneously. A buyer pays a multiple on the thin number. Nobody pays 10x on a liability.

This is where the deferred-revenue mechanics turn into a deal problem, and it compounds with how commissions get expensed against the wrong period. If your implementation go-live dates are not wired directly to your billing schedule and your revenue schedule, your historicals are not conservative — they are fiction, and a diligence team will treat them that way. The same disconnect that creates the revenue recognition trap is what hands a private-equity buyer the lever to restructure an earnout or shave the valuation in the last week.

The numbers on this are not gentle. Per EY's M&A tech analysis, 54% of SaaS acquisitions take a downward purchase-price adjustment specifically traced to ASC 606 misalignment surfaced during Quality of Earnings. Conflating multi-year bookings with recognized revenue routinely overstates EBITDA by something on the order of a third — and EBITDA is the number the multiple multiplies. The move is to run a clean, monthly quality of earnings check on yourself, every month, so the first time anyone reconciles your bookings to your recognized revenue, it is you, in a quarter where the stakes are zero.

Cash is the one you can't talk your way out of

You can goose bookings with a discount and an aggressive close. You can smooth revenue with a generous reading of when "delivery" happens. You cannot argue with the balance in your operating account — it is the one company of the three that does not negotiate. The distance between recognizing a dollar of revenue and actually banking it is your cash conversion cycle, and right now your largest customers are using that cycle as a weapon. Procurement teams have learned to stretch Net 30 into Net 60 and Net 90, knowing your payroll runs every two weeks regardless.

Watch what that does at scale. Bessemer's State of the Cloud benchmarks put average B2B SaaS Days Sales Outstanding at 72 days, up from 58 in 2023 — collection now takes two and a half months while your cloud-infrastructure invoices and salaries clear on a two-to-four-week clock. The deficit between those two timelines does not shrink as you grow; it grows faster than you do, because every new enterprise logo enlarges the float you are extending. You cannot make payroll out of deferred revenue, and you cannot fund a launch out of accounts receivable.

So make the three companies reconcile on a fixed cadence instead of once, under duress, in a data room. Two moves do most of the work. First, run a standing three-way trace every month: follow one representative dollar from the day it posts as closed-won in your CRM, to the month it shows up as recognized revenue in your ledger, to the day it actually clears the bank — and put the lag, in days, on the same slide as the bookings number, not in an appendix. Second, gate the commission. Pay the rep 50% on the booking and the remaining 50% on cash collection. That one change quietly realigns your most expensive cash outflow with the cycle that actually funds it, and it turns your sales team into people who care when an invoice gets paid.

The payoff is defensive and it is large. A buyer reads your cash discipline through your net working capital target at close. Bloated receivables and a sluggish conversion cycle let them demand a higher working-capital peg, and that peg comes straight out of your closing wire — real money, gone, on the way out the door. Reconciling bookings, revenue, and cash is not accounting hygiene. It is how you keep the three companies you actually run from being valued as the worst one.