The practical answer

- Short answer

- Your SaaS dashboard says $15M ARR. Your bank says otherwise. Here's where the days leak in the order-to-cash cycle, and how to claw each one back.

- Best fit

- Industry: B2B SaaS. Function: Finance & RevOps

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 7 Days of DSO reduction required to free up cash equivalent to 2% of annual revenue.

Picture the all-hands slide: $15M in ARR, up and to the right. Now picture the operating account behind it. If your Days Sales Outstanding sits at 68 days, roughly $2.8M of that "revenue" is not money — it is paper sitting in the gap between a signature in Salesforce and a wire that clears NetSuite. The dashboard is telling you a story about a business that does not yet have the cash that business claims.

I see this pattern most clearly at Series B and C SaaS companies that have learned to optimize bookings and never learned to optimize collection. They run beautiful cohort analyses on net revenue retention and CAC payback, and they cannot tell me, to the day, how long it takes a Closed-Won deal to become spendable cash. That number — booking-to-bank — is the one that funds payroll, and it is almost never on a slide. Teams in this spot usually think they have a burn rate problem. Often they don't. They have a collection problem wearing a burn-rate costume.

The reason this gap is lethal right now is the cost of acquiring the booking in the first place. Per Benchmarkit's 2025 SaaS Performance Metrics, the New CAC Ratio rose 14%, with companies spending a median of $2.00 in sales and marketing to land $1.00 of new ARR. When you front two dollars to win one dollar of revenue, every extra day that dollar spends trapped in receivables compounds against you. For enterprise-facing B2B SaaS specifically, the LedgerUp 2026 B2B SaaS DSO Benchmarks put top-quartile DSO under 45 days and the bottom quartile north of 90. That 45-day spread is not a finance nuance. It is the difference between funding next quarter's roadmap from your own collections and walking into your existing investors for a flat bridge round you did not need to raise.

A booking is an uncollateralized promise to pay. The day it lands in your bank is the only day that funds payroll.

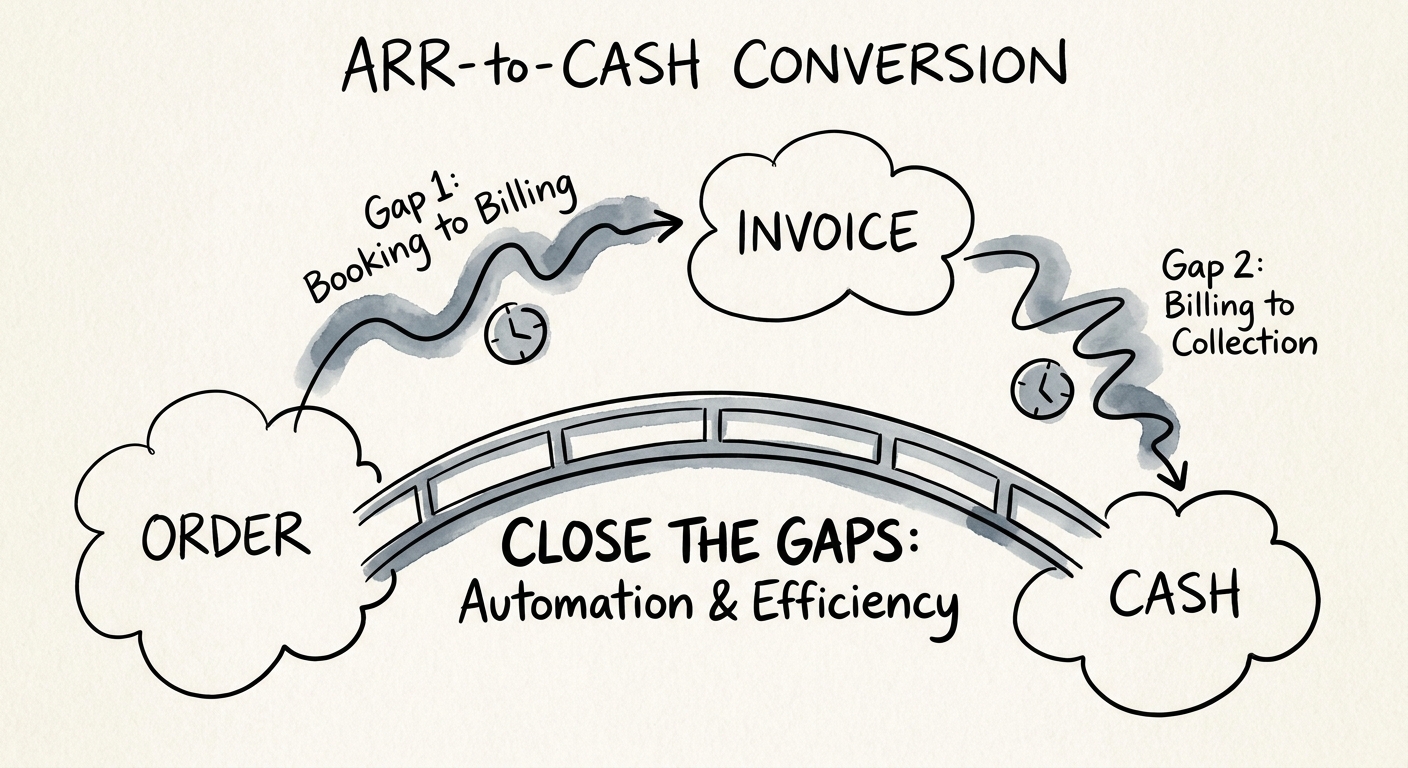

Trace one deal and watch the days leak

The booking-to-bank number is not a single delay. It is the sum of three handoffs, each owned by a different team, each invisible to the others. Take a hypothetical Net-30 enterprise deal — say a $180K annual contract signed on day zero — and follow the clock.

Days 0–14: the invoice that doesn't exist yet

Net-30 implies the meter starts at signature. It doesn't. It starts when the customer receives a correct invoice, and in most scaling SaaS shops that takes 10 to 15 days. The CRM record is structurally incompatible with the ERP: the rep sold a custom SKU finance has never seen, promised a quarterly billing schedule nobody configured, and never captured the actual accounts-payable contact or the PO requirement. Finance is reverse-engineering the deal before they can bill it. A billing-aware CPQ layer that enforces real financial fields at quote time is what collapses this window — it stops the rep from selling something the system cannot invoice.

Days 14–60: Net-30 is a suggestion, not a term

The invoice finally goes out on day 14. The customer's procurement team reads "Net-30" and pays on their cadence, not yours — which for large buyers routinely means 45 to 60 days from receipt. Now your contractual 30 has quietly become 50-plus on the clock, and you are floating an interest-free loan to a Fortune 500 balance sheet off the back of yours. If your stated terms say 30 and your measured DSO says 55, the delta is not the customer being difficult. It is your collections running on hope instead of a schedule.

Day 60: dispute purgatory resets everything

This is the cut that hurts most, because it erases all prior progress. The invoice lands in AP and bounces — missing PO number, wrong legal entity, a subscription tier that doesn't match the signed order form. The clock does not pause; it resets. You re-issue and start another 30-to-45-day cycle from scratch. The exact same line-item sloppiness that strands this cash is what revenue recognition issues surface during PE due diligence, where they quietly compress your multiple. A messy order-to-cash process is not just a liquidity problem today; it is a valuation problem at exit.

Close the gap at the source, not at the invoice

The instinct is to throw collectors at the back end. That treats the symptom. Booking-to-bank is a revenue-architecture problem — the leak is upstream, in the silos between Sales, RevOps, and Finance — so the fixes have to start there. Three moves, in order of leverage.

Make Closed-Won fire the invoice automatically. The moment an opportunity flips to Closed-Won, the invoice should generate with no human in the loop. That single automation is what kills the 10-to-15-day front-end delay, and the payoff is concrete: a JPMorgan working capital analysis found that cutting DSO by just 7 days frees cash equal to 2% of annual revenue. On a $15M business, that is $300K of runway you already earned, sitting in receivables, waiting for someone to ask for it.

Put the financial guardrails at the point of sale. You cannot bill cleanly off a structurally broken contract, so reject the broken contract before it is signed. Required PO field, validated legal entity, billing contact, a SKU finance can actually invoice — enforced in the quote, not patched after. A RevOps On-Demand case study documented a scaling B2B SaaS company cutting order-to-cash time by 75% almost entirely by removing manual handoffs and gating qualification at the CRM. Most of the win was prevention, not collection.

Then, and only then, automate dunning. Stop letting your Customer Success Managers moonlight as debt collectors. An AR system that nudges 7 days before due, on the due date, and escalates on a fixed schedule after collects more cash and protects the relationship better than a CSM sending an awkward email. Here is the Monday move: pull your last 20 Closed-Won deals and timestamp each one — signed, invoiced, paid. The spread between your median and your slowest will tell you exactly which of the three handoffs is bleeding you, and you fix that one first. Because quality of earnings is never measured by what you booked. It is measured by what cleared the bank.