The practical answer

- Short answer

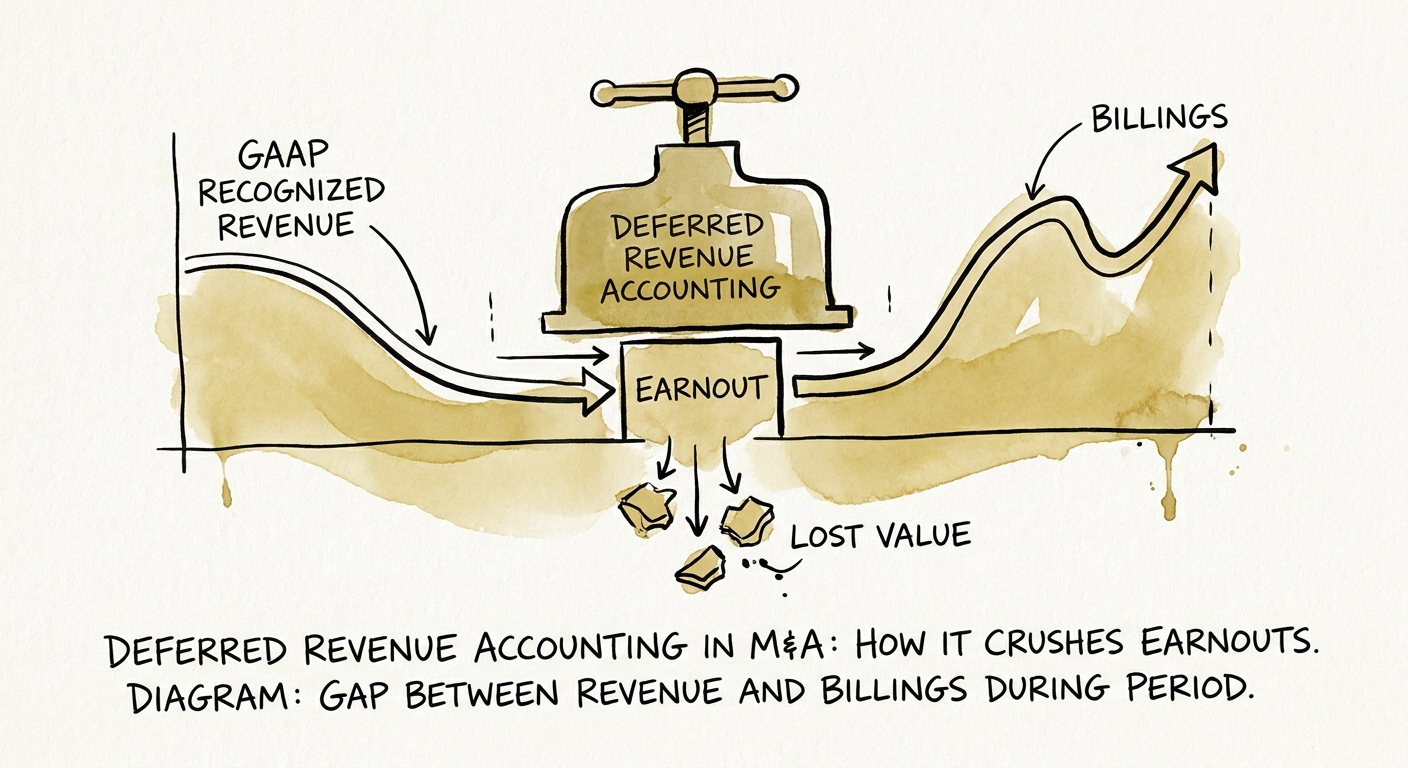

- Annual-upfront SaaS founders lose earnouts to a purchase-accounting write-down they never see coming. Here is the exact math, and the LOI language that stops it.

- Best fit

- Industry: B2B SaaS. Function: M&A Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 70% Of M&A transactions fail to achieve projected operational synergies due to complex integration.

Your best-collecting SaaS business is the one most exposed

Picture a 60-person vertical SaaS company billing annual contracts upfront. Cash machine. The founder collects twelve months in advance, deferred revenue swells on the balance sheet, and that prepayment discipline is exactly what made the company attractive to a buyer in the first place. Then the deal closes with a revenue-based earnout bridging the last turn of valuation, and the first post-close month the GAAP revenue line drops off a cliff. The founder calls me convinced the new owner is sandbagging the numbers. The new owner is doing no such thing. They are just following purchase accounting.

I walked one $40M SaaS exit through this line by line. The founder had a "guaranteed" two-year earnout pegged to recognized revenue, and I had to rebuild the entire post-close revenue model to show him the payout was mathematically unreachable before anyone made a single sales call. Not because the business slowed down. Because of how the buyer was required to value the deferred revenue he handed them at close.

Run the math on a single $100,000 contract

Under FASB's ASC 805 business combinations standard, an acquirer records assumed liabilities at fair value. Deferred revenue is a liability — you owe service to a customer who already paid. And in purchase accounting, "fair value" of that obligation is not the cash you collected. It is the buyer's remaining cost to deliver the service, plus a thin profit margin. BDO's analysis of these adjustments notes the write-down routinely erases 20% to 40% of the deferred balance outright.

For SaaS specifically the cut is brutal, because your gross margins are the reason. Say you collected $100,000 on an annual contract that's half-consumed at close. The buyer estimates the cost to fulfill the rest — hosting, baseline support — at $20,000, adds a 10% margin, and books the obligation at $22,000. The other $78,000 of revenue you would have recognized over the year simply ceases to exist on the post-close P&L. During your earnout window, that contract contributes $22,000 of GAAP revenue instead of $100,000. Stack that across a renewal book and the target you signed for becomes unreachable arithmetic. The healthier your collections, the bigger the hole.

The buyer isn't cheating you. They're following the accounting standard to the letter. That's what makes the deferred revenue haircut so dangerous: by the time you feel it, everyone involved can honestly say they did nothing wrong.

"But didn't ASU 2021-08 fix this?" — yes, and that answer can still cost you the payout

A sharp CFO will stop me here. The Financial Accounting Standards Board did issue ASU 2021-08 to align acquired deferred revenue with ASC 606 recognition rules, letting U.S. GAAP acquirers carry the balance over without the classic haircut. True. But treating that update as armor for your earnout is how founders lose money while believing they're protected. Three things the relief does not cover:

It's a U.S. GAAP rule, and your buyer may not report under U.S. GAAP. Sell to a global strategic or an internationally-managed PE platform reporting under IFRS 3 and the original fair value haircut is alive and well. CBIZ's purchase-accounting guidance confirms international standards never adopted the same relief, so cross-border SaaS deals stay fully exposed to the write-down.

Carryover doesn't mean clean recognition. Even when the balance survives, it lands inside someone else's books. Once your standalone revenue gets merged into a platform company's ERP, attribution turns to mud — deals get re-allocated across entities, discounts applied inconsistently, recognition timing shifts to match the parent's policy. McKinsey's integration research finds roughly 70% of transactions miss their projected operational synergies, largely from this kind of internal disorder. If your payout rides on GAAP recognized revenue, you've tied it to the acquirer's accounting policies, their auditor's interpretation, and an integration timeline you can't control.

You handed over the scoreboard. That's the real exposure. A recognized-revenue earnout means the party that owes you money also keeps the books that decide whether you get paid. No founder would design it that way on purpose — but it's the default if you don't fight the definition early.

Fix it in the LOI, not the purchase agreement

The window to win this is the Letter of Intent. Try to renegotiate the earnout definition once lawyers are drafting the definitive agreement and you'll be accused of re-trading the deal. PwC's deal-risk analysis flags earnouts as a leading source of post-close litigation precisely because these definitions get left vague while everyone's still shaking hands. Four pieces of language, in priority order:

1. Measure billings or ARR, not GAAP revenue

This single change neutralizes the haircut. Peg contingent consideration to billings, cash collections, or ARR growth — operational metrics that purchase accounting can't touch. Close a $100,000 annual contract after the deal, you get credit for $100,000. It is the most important move in negotiating earnout terms that actually pay out, and it makes the next three less load-bearing.

2. If they insist on recognized revenue, demand a stand-alone calculation exhibit

When a buyer won't move off recognized revenue, force a mathematical exhibit into the agreement that computes earnout revenue on a stand-alone basis — explicitly excluding ASC 805 fair value adjustments, purchase accounting effects, and any post-close changes to recognition policy. Spell out the formula. Ambiguity always resolves in the bookkeeper's favor.

3. Lock operational covenants around your engine

Accounting protection is worthless if the buyer starves the business. Restrict them, in writing, from gutting your top reps' comp plans, cutting marketing spend, or forcing destructive bundle pricing during the earnout without your consent. A revenue target you can't fund is a target you've already missed.

4. Don't let deferred revenue get double-counted in working capital

Watch the net working capital peg. Buyers love to treat deferred revenue as a dollar-for-dollar liability there, making you leave excess cash at close to "fund" future delivery — after they already wrote the same balance down elsewhere. Argue hard that the real liability is the cost to fulfill, not the full collected amount. A clean sell-side Quality of Earnings report that isolates that fulfillment cost is your sharpest tool for winning the argument.

Monday, pull your three largest annual-upfront contracts and ask one question: if the buyer recognized only their cost to fulfill, what would each contribute to my earnout? If that number scares you, you've found the clause to write before you sign the LOI. An earnout shifts operational and market risk onto the seller by design — your job is to make sure it doesn't quietly shift the buyer's accounting risk onto you too.