The practical answer

- Short answer

- The exact ASC 606 mistakes — SSP allocation, contract mods, capitalized commissions — that surface in QofE and reprice B2B SaaS deals. With the math.

- Best fit

- Industry: B2B SaaS. Function: Finance & Operations

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 41% Software firms can fail SSP allocation testing during M&A due diligence.

The number on the LOI was never your real ARR

Here is the moment that ends a clean process. A sponsor sends an LOI at 8x ARR. Three weeks into diligence, the Quality of Earnings team pulls your contract sample, maps invoices against performance obligations, and asks one question your controller can't answer cleanly: "How are you recognizing the implementation fees?" Two days later the deal is repriced — not because you committed fraud, but because the revenue you reported and the revenue you earned under ASC 606 were never the same number. The multiple gets applied to the smaller one.

Picture a $45M ARR enterprise software company — the kind where the controller has been amortizing every subscription in a single heroic Excel workbook for four years. Say they booked $2.8M of non-refundable implementation fees and recognized them ratably over the 12-month initial term, because that's how the invoices were structured. The trap: those implementation services have no standalone value outside the proprietary platform. They only matter because the customer is buying the subscription. Under ASC 606, that revenue stretches across the estimated customer life, not the contract term. If churn data says the average customer stays 42 months, jamming the recognition into 12 months overstated trailing-twelve-month revenue every single quarter — and at the deal's EBITDA multiple, correcting it produced a material purchase-price cut. Not an accounting footnote. A wire that came in smaller.

FASB built ASC 606 specifically to kill the old "recognize what you bill" reflex that software companies leaned on for years. As PwC's Software Revenue Recognition guide lays out, the hard part for SaaS isn't the five steps in the abstract — it's allocating one negotiated price across a license and a bundle of services that your sales team discounted to win the logo. Your invoicing schedule is not your recognition schedule. The day you internalize that is the day your Quality of Earnings exposure starts shrinking.

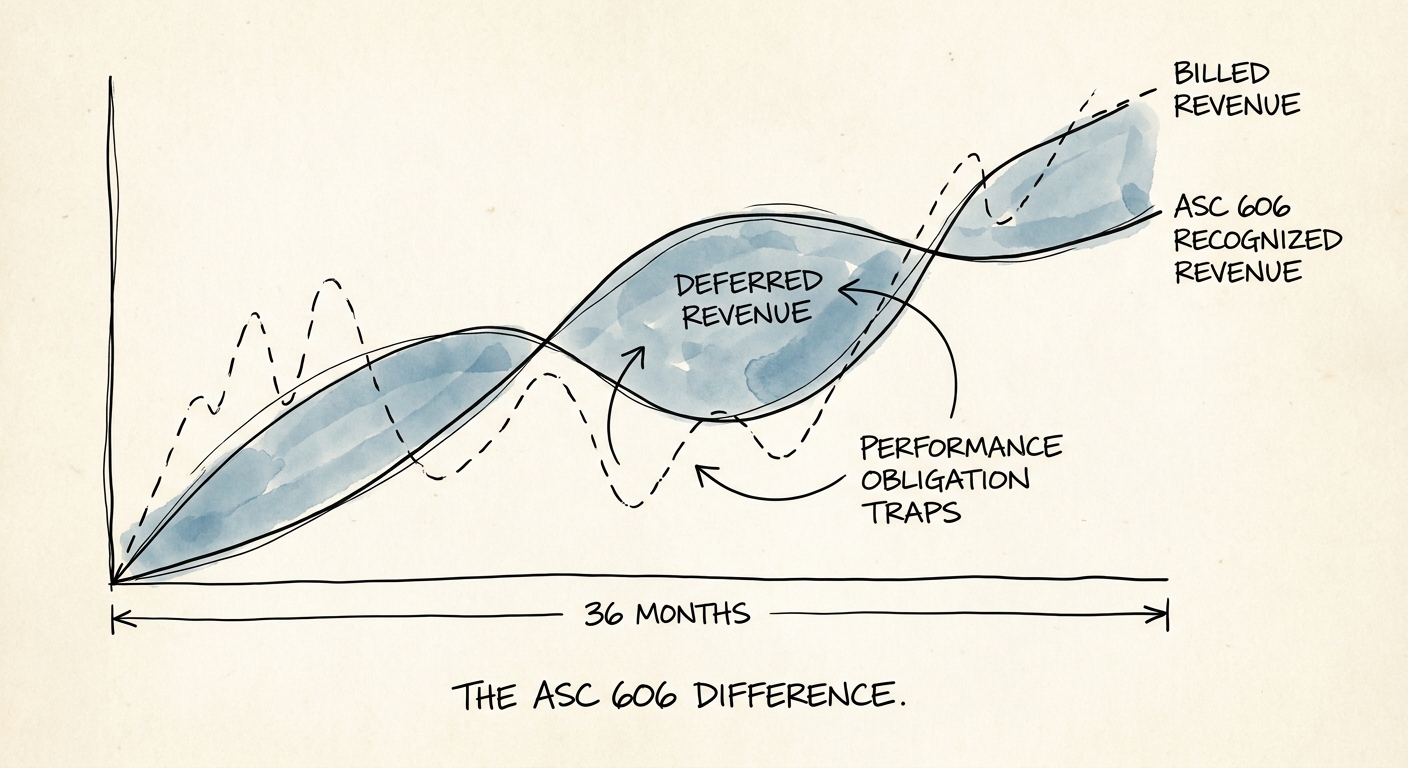

In a SaaS deal, the buyer doesn't pay for the revenue you billed. They pay for the revenue ASC 606 says you actually earned — and a Big 4 QofE team will find the gap in a week.

Run the SSP math before a buyer runs it for you

Step 4 — allocating the transaction price by Standalone Selling Price — is where subscription businesses get cut deepest, because it's the step where the sales motion and the accounting motion openly disagree. Reps discount services to nothing to land a big subscription. Your billing reflects that distortion. ASC 606 says you can't recognize against those distorted line items at all.

Do the arithmetic on a typical bundled deal. A $200,000 contract lists a $180,000 license and $20,000 of implementation. But your historical SSP analysis shows the software actually clears around $150,000 standalone and the services around $50,000 — a $200,000 SSP total. You don't recognize the contract the way you invoiced it. You re-weight: services are 25% of the SSP, so $50,000 gets recognized as services revenue when delivered; the software is 75%, so $150,000 recognizes ratably over the term. The free-looking implementation isn't free in your ledger — it pulls real dollars out of your subscription line and into a point-in-time bucket.

Now scale that error. Picture a late-stage SaaS company throwing in "$60,000 implementation, on the house" to close $250,000 ACV enterprise deals, then recognizing the full $250,000 ratably over twelve months. Every closed deal silently overstated the subscription ARR — the exact metric the multiple keys off. The fix is to carve out the implementation at its SSP, recognize it at milestone delivery, and defer the rest. KPMG's Revenue Recognition handbook is blunt that list price alone won't defend your allocation. You need a data-driven SSP matrix built from a tight band of actual historical discount rates, refreshed on a rolling 12-month basis. Hand auditors a static 2023 pricing sheet instead, and you've earned what compounds into the revenue recognition trap: a full substantive test of your entire revenue population, a blown timeline, and audit fees that detonate mid-process.

Two places Excel quietly breaks: mid-term mods and commissions

Step 5 — when you actually recognize — is where B2B SaaS gets genuinely messy, because SaaS customers never sit still. They add seats in March, downgrade a module in June, co-term a renewal in September. Each modification forks three ways: treat it as a separate contract, as a termination-and-new-contract, or as a cumulative catch-up against revenue already recognized. A spreadsheet can't reliably carry that branching logic across hundreds of accounts. Get it wrong on an upsell that doesn't add distinct goods at their standalone prices, and you owe a catch-up adjustment in the current period — the kind of restatement that shows up precisely when a buyer is watching your trailing numbers.

The second quiet killer lives in ASC 606's sister standard, ASC 340-40, on the cost of obtaining a contract. I've watched founders expense sales commissions on day one to trim taxable income — and unknowingly torch their own EBITDA. If you pay a 10% commission on a one-year deal but your customers actually stay four years, the standard says capitalize that commission and amortize it over ~48 months, matching how the service transfers. Expense it all up front and you depress today's EBITDA against the same multiple a buyer is about to apply. You're paying real exit value to save marginal tax. EY's technical line on the revenue standard spells out why software entities need a documented capitalization policy — the same discipline gap that drives the recognition issues that kill deals on the services side.

What to do Monday: pull your ten largest bundled contracts and check whether implementation is recognized at its SSP or buried in ratable subscription — that one test predicts most of your QofE exposure. Then decide your migration line. Somewhere around $15M ARR, the manual ledger stops being thrift and becomes a liability; a real sub-ledger (NetSuite ARM, Zuora RevPro, or equivalent) is exit preparation, not overhead. Document the SSP matrix, align commission amortization to actual retention, and make sure your invoicing data can survive being mapped against your performance obligations. The difference between a 10x clean close and a repriced 6x is rarely the product. It's whether your revenue can withstand the read.