The practical answer

- Short answer

- Stop blending Azure resale with professional services. Learn why Gross vs. Net revenue recognition impacts your valuation and how to fix your books before Due Diligence.

- Best fit

- Industry: Cloud Services / MSP. Function: Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 15-18% Average CSP Margin (Gross) for Azure Partners in 2025

The $20M Lie: Why Your Top Line Is a Hallucination

You think you are a $20M ARR company growing at 30% year-over-year. You have the dashboard to prove it. But when you hand that P&L to a Private Equity sponsor or a strategic acquirer, they don't see a $20M growth rocket. They see an $8M services firm hiding behind $12M of low-margin, pass-through Azure spend.

This is the Azure Revenue Illusion, and it is the single most common reason Series B founders and MSP owners get their valuation expectations crushed in the Letter of Intent (LOI) phase. In the Microsoft ecosystem, Cloud Solution Provider (CSP) revenue—selling Azure consumption or M365 licenses—is fundamentally different from Professional Services or Managed Services revenue. Yet, 60% of partners I audit blend these lines on their P&L, treating a dollar of Azure resale exactly like a dollar of high-margin IP.

Here is the brutal math of the market: Services revenue trades at 8x–12x EBITDA. Resale revenue trades at 0.5x–1x Revenue (or roughly 4x EBITDA).

When you present a $20M top line where 60% is pass-through Azure spend, you aren't impressing buyers. You are signaling two things: first, that you don't understand your own unit economics; and second, that your "growth" is fueled by low-calorie revenue that churns the moment a client finds a slightly cheaper distributor. If you want a premium exit, you must stop treating Microsoft's revenue as your own.

If you book $10M in Azure resale as revenue, you haven't built a $10M business. You've built a billing department for Satya Nadella.

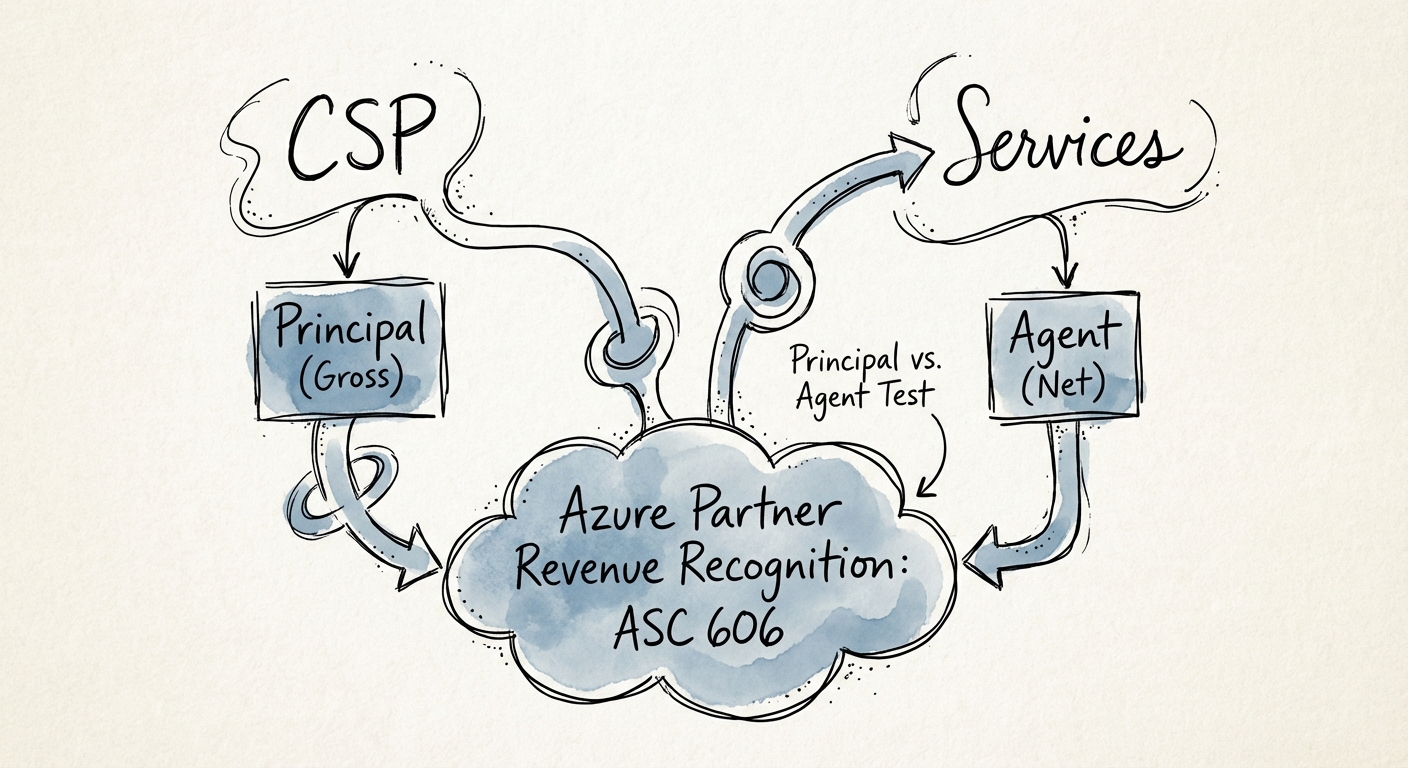

The ASC 606 Guillotine: Principal vs. Agent

The valuation haircut is painful, but the accounting correction is fatal. Under ASC 606 (Revenue from Contracts with Customers), the distinction between recognizing revenue on a Gross basis (the total bill to the client) versus a Net basis (your margin only) hinges on one concept: Control.

To recognize Gross revenue (Principal), you must control the good or service before it is transferred to the customer. Ask yourself these three questions about your Azure CSP business:

- Primary Responsibility: If Azure goes down, are you responsible for bringing it back up, or is Microsoft? (Hint: It's Microsoft).

- Inventory Risk: Do you purchase the Azure capacity before the client orders it? (No, it's consumption-based).

- Pricing Discretion: Can you set the price, or are you bound by Microsoft's MSRP and margin caps? (Mostly bound).

For 95% of partners, the answer is clear: You are an Agent. You do not control the Azure cloud. Therefore, under GAAP and IFRS, you should only be recognizing the Net margin (the ~15% spread), not the full billing amount.

The "Quality of Earnings" Nightmare

When a PE firm conducts a Quality of Earnings (QofE) analysis, they will restate your revenue from Gross to Net. Suddenly, your $20M company "shrinks" to $9.8M overnight. While your EBITDA dollars remain the same, your revenue metrics collapse, destroying your "Rule of 40" narrative and revealing that your actual operating margins are likely far lower than you claimed. This often triggers a deal re-trade, shaving millions off the purchase price.

The Operational Pivot: From Reseller to Value-Add

You cannot accounting-trick your way out of this. The solution is operational. To command a premium multiple, you must decouple your low-value resale from your high-value services in both your contracts and your P&L.

1. Restructure Your P&L: Stop commingling funds. Create a distinct "Pass-Through Revenue" line item below the Gross Margin line or separate it entirely in management reporting. Your Board deck should show "Net Revenue" (Services + CSP Margin) as the primary growth metric, not Gross Billings.

2. The "Managed Azure" Wrapper: If you want to recognize Gross revenue legitimately, you must change the nature of the deliverable. You aren't selling Azure; you are selling a "Managed Cloud Platform" where the underlying compute is just one cost of goods sold (COGS) component of a larger, bundled service that you take responsibility for. This requires a contractual pivot where the client buys a service level agreement (SLA) from you, not just licenses.

3. Audit Your NCE Exposure: With Microsoft's New Commerce Experience (NCE), you are now on the hook for the term of the license even if the client goes bust. If you are recognizing Gross revenue without accounting for this credit risk liability, your books are a latent risk. Smart CFOs are moving low-margin, high-risk NCE clients to direct billing, happily sacrificing the 15% margin to remove the liability from their balance sheet. It’s better to be an $8M high-margin services firm than a $20M low-margin bank for Microsoft.