The practical answer

- Short answer

- Stop reporting 'vanity EBITDA' to your board. Learn the precise EBITDA calculation formula that survives due diligence and the add-backs PE firms actually accept.

- Best fit

- Industry: B2B SaaS & Services. Function: Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 7.4x Average EBITDA multiple for sellers with sell-side QofE vs. 7.0x without (2025 Data)

The 'GAAP Gap' That Kills Credibility

There is a dangerous delta between the number you show your board and the number a private equity buyer will eventually pay for. We call this the "GAAP Gap." Most founders operate their businesses based on cash balances or, if they are slightly more sophisticated, GAAP Net Income. Both are useless for high-growth valuation.

Cash tells you if you can make payroll Friday. Net Income tells you what your tax bill is. Neither tells an investor what your business is worth. To a PE sponsor, your value is a multiple of your sustainable, recurring cash flow capacity—your Adjusted EBITDA.

However, 2025 data reveals a harsh reality: Management EBITDA is routinely slashed by an average of 28% during Quality of Earnings (QofE) due diligence. That means for every $1M in EBITDA you think you have, a buyer only sees $720k. At a 10x multiple, you just lost $2.8M in enterprise value because your calculation methodology was flawed.

Why Your Board Does Not Trust Your Number

If you are reporting a different EBITDA margin every month based on how you "feel" about certain expenses, you have already lost the room. Board members—especially those from PE backgrounds—can smell "creative accounting" instantly. When you strip out "marketing experiments" one month but capitalize them the next, you aren't adjusting; you are hallucinating.

The goal of board reporting is not to make the quarter look good. It is to provide a reliable proxy for the eventual exit valuation. If your internal reporting does not mirror a rigorous Quality of Earnings (QofE) standard, you lack the operating visibility to steer.

Your board doesn't want to see your creative writing class project. They want to see your cash flow capacity. If you can't defend the add-back with an invoice and a contract, it stays in expenses.

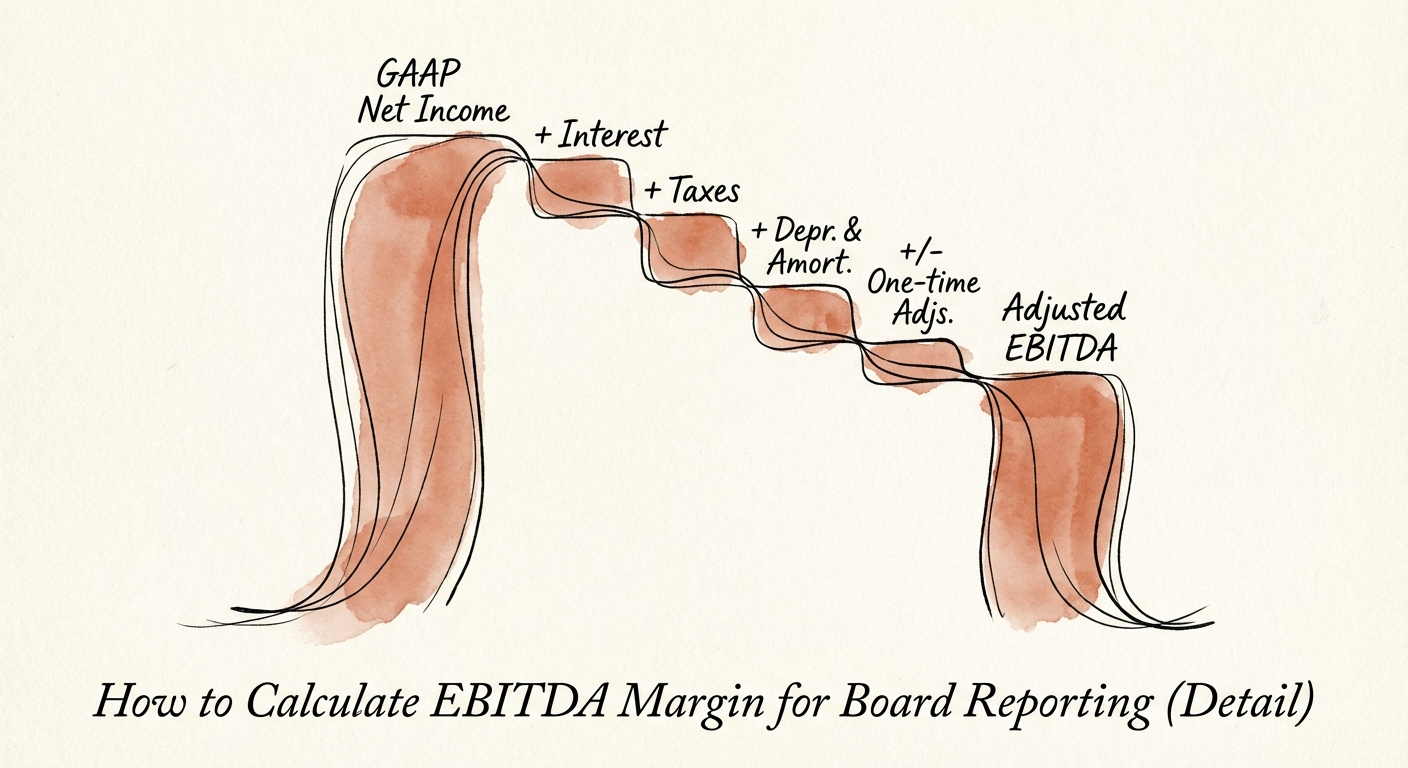

The Formula: Building an EBITDA Bridge That Holds Weight

You cannot just "eyeball" your adjustments. You need a defensible, mathematical bridge. This is the exact formula we use when preparing clients for exit, moving from the bottom of the P&L up to a valuation-ready number.

Step 1: The Baseline (Standard EBITDA)

Start with GAAP Net Income. Add back Interest, Taxes, Depreciation, and Amortization. This is your "unadjusted" EBITDA. It is the baseline, but it is rarely the valuation metric because it includes the "noise" of running a private company.

Step 2: The Three Buckets of Legitimate Adjustments

This is where deals die. Buyers will accept adjustments if—and only if—they fall into three specific, documentable categories:

- Non-Recurring Expenses (The "One-Timers"): This includes litigation settlements, expenses related to M&A (if you bought a company), or severance for a localized RIF. Note: A "failed marketing campaign" is NOT non-recurring. That is just the cost of doing business.

- Pro-Forma Adjustments (The "Run-Rate"): If you closed a money-losing division in June, you can add back the losses from Jan-May to show what the business looks like now. If you just raised prices, you typically cannot claim the full year impact unless it's contractually locked.

- Owner/Manager Normalization (The "Lifestyle" Add-Backs): If you pay yourself $500k but a replacement CEO costs $300k, you add back the $200k difference. If you run your personal vehicle or club membership through the P&L, add it back. Be warned: If you adjust for "market rate salaries" on the high end, buyers will also adjust your underpaid staff up to market rates, which lowers your EBITDA.

The Golden Rule of Adjustments: If you add it back, you must be able to prove it will never happen again. If you claim "implementation costs" are an add-back, but you have implementation costs every single year, that is not an add-back. That is COGS.

Presenting the Data: The 'Bridge Chart'

Stop sending your board a wall of numbers in Excel. Visualizing the journey from Net Income to Adjusted EBITDA builds confidence. Your board deck should include a "Waterfalls" or "Bridge" chart every quarter.

The Board Packet Hierarchy

Your finance section needs to answer three questions in this order:

- What is our GAAP Net Income? (The Audit View)

- What is our Unadjusted EBITDA? (The Cash View)

- What is our Adjusted EBITDA? (The Valuation View)

Below the Adjusted EBITDA figure, list your top 3 adjustments by dollar value. Transparency is your shield. If you explicitly state, "We added back $150k for the recruiter fees on the VP of Sales search," the board can debate the merit, but they cannot accuse you of hiding it.

The 2026 Reality: Profitability is the New Religion

In 2021, you could get away with "growth at all costs." In 2026, the Rule of 40 has bifurcated. Growth is still king, but unprofitable growth is now penalized. Recent benchmarks show that sellers who conduct a sell-side QofE (essentially doing this math rigorously before the buyer does) achieve an exit multiple of 7.4x compared to 7.0x for those who don't. That 0.4 turn on $5M EBITDA is $2M in your pocket—just for getting the math right.