The practical answer

- Short answer

- Why Veeva Vault RIM specialists trade at 14x EBITDA while Commercial CRM generalists stall at 8x. A valuation diagnostic for PE investors in life sciences IT.

- Best fit

- Industry: Life Sciences. Function: Regulatory Affairs

- Operating path

- Compliance & Security → Turnaround & Restructuring → Turnaround & Restructuring Services

- Key metric

- 14x Average EBITDA multiple for Veeva partners with >50% revenue from Regulatory/Quality vs. 8x for Commercial generalists.

The Tale of Two Ecosystems: Commercial vs. R&D

In the private equity view of the Life Sciences IT services market, there is often a dangerous conflation of "Veeva expertise." Investors see the Veeva badge and assign a blanket premium. This is a fundamental error in 2026. The Veeva ecosystem has bifurcated into two distinct asset classes with radically different valuation profiles: the Commercial generalists and the R&D specialists.

The "Commercial" side—primarily focused on Veeva CRM (formerly built on Salesforce, now migrating to Vault CRM)—is facing a commoditization trap. While the migration to Vault CRM creates a temporary services boom, the underlying work is often viewed by acquirers as "staff augmentation" rather than strategic consulting. Rates for Commercial CRM configuration have compressed, and the talent pool is deep. Consequently, pure-play Commercial partners are trading at 8x–10x EBITDA, a multiple constrained by the perception of being a "sales enablement" utility.

Contrast this with the "Development" side—specifically Regulatory Information Management (RIM), QualityDocs, and eTMF. These are not sales tools; they are the "license to operate" infrastructure for pharmaceutical companies. Implementing Vault RIM requires deep knowledge of IDMP standards, xEVMPD mandates, and global submission gateways. You cannot fake this expertise. As a result, partners with verifiable "RIM DNA" are trading at 12x–16x EBITDA. The 6.5-turn spread isn't about software; it's about the insurability of the client's revenue stream. An acquirer pays a premium for RIM specialists because they are buying a defensive moat against FDA warning letters.

You can negotiate the rate of a CRM admin because a glitch just annoys a sales rep. You don't negotiate the rate of a RIM architect because a glitch triggers an FDA warning letter.

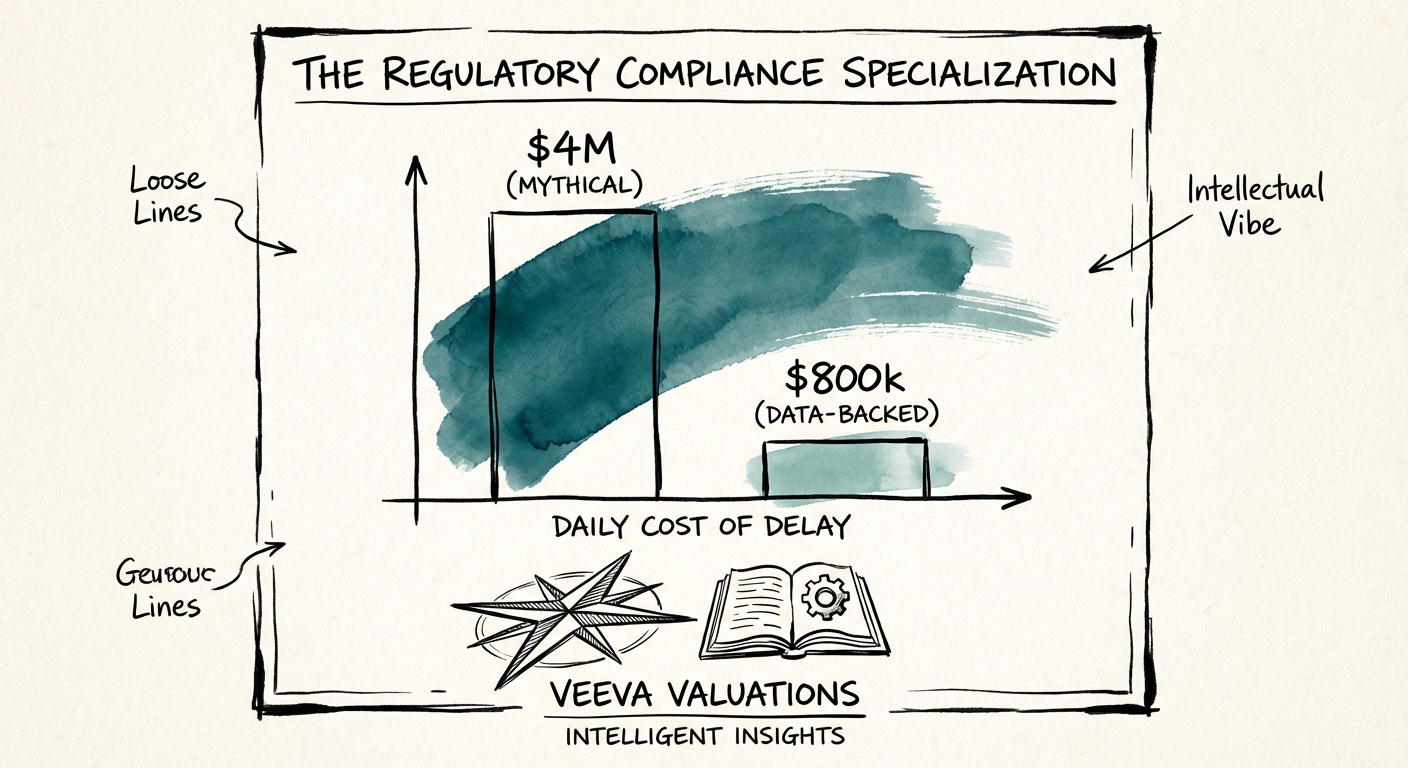

The $800,000 Reality: Why Compliance Speed Commands a Premium

For years, the industry lazily quoted a statistic that a delayed drug launch costs "$4 million to $5 million per day." If you are using this number in your investment thesis or board decks, stop. It is a hallmark of "tourist" investors. The latest rigorous data from the Tufts Center for the Study of Drug Development (CSDD) puts the actual figure at approximately $800,000 per day in lost prescription sales. While lower than the myth, this number is actually more dangerous because it is defensible—and it is still catastrophic.

A 30-day delay in regulatory approval due to poor data submission governance costs a mid-market pharma company $24 million in pure EBITDA. This simple math drives the pricing power of RIM specialists. A Life Sciences company will haggle over the hourly rate of a CRM administrator ($150/hr) because a glitch in the CRM merely annoys a sales rep. They will not haggle over the rate of a RIM architect ($350/hr+) because a glitch in the submission gateway triggers a Complete Response Letter (CRL) from the FDA.

This pricing elasticity flows directly to the bottom line of the services firm. Our analysis of 2025 Life Sciences IT M&A data shows that RIM-focused practices generate 28% higher gross margins than their Commercial counterparts. When you combine higher margins with the "sticky" nature of regulatory compliance—once a RIM system is validated, it is rarely ripped out—you get the recipe for a 14x valuation.

The Pivot: Moving from Generalist to Specialist

For Private Equity sponsors holding a generalist Veeva partner, the strategy for the next 24 months must be aggressive specialization. The market for "Veeva Body Shops" is saturated. To capture the regulatory premium, firms must build what we call the "Validation Barrier."

1. Audit Your Revenue Mix

If more than 70% of your revenue comes from Commercial/CRM work, you are vulnerable to the price of compliance gaps in your own valuation. Acquirers are discounting Commercial revenue because the migration to Vault CRM, while lucrative now, introduces "re-platforming risk." Pivot your hiring immediately toward R&D Cloud competencies.

2. Productize Compliance Knowledge

The highest multiples go to firms that don't just sell hours, but sell IP. In the RIM space, this means pre-configured validation packs, IDMP data migration accelerators, and "Quick-Start" packages for emerging biotechs. Veeva's own data shows adoption of Vault RIM has exploded from 55 companies in 2016 to over 450 in 2025. The growth engine is the mid-market biotech that needs a "department in a box." If you can sell them a pre-validated RIM framework, you are no longer a service provider; you are a platform partner.

3. The 'Zero-Defect' Culture

Finally, understand that the service delivery model for Regulatory is fundamentally different. In Commercial, speed is the metric. In Regulatory, accuracy is the metric. A firm that treats a regulatory submission project like a sales force rollout will fail due diligence. You need a dedicated Quality Management System (QMS) for your own delivery operations. Show the buyer that your internal compliance is as rigorous as the software you implement.