The practical answer

- Short answer

- Generalist Palo Alto partners trade at 8x EBITDA. XSIAM specialists command 16x. Here is the diagnostic framework for valuing Cortex practices in 2026.

- Best fit

- Industry: Cybersecurity / MSSP. Function: Valuation & Exit Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 16x EBITDA multiple for partners with specialized XSIAM/MDR practices vs. 8x for generalists.

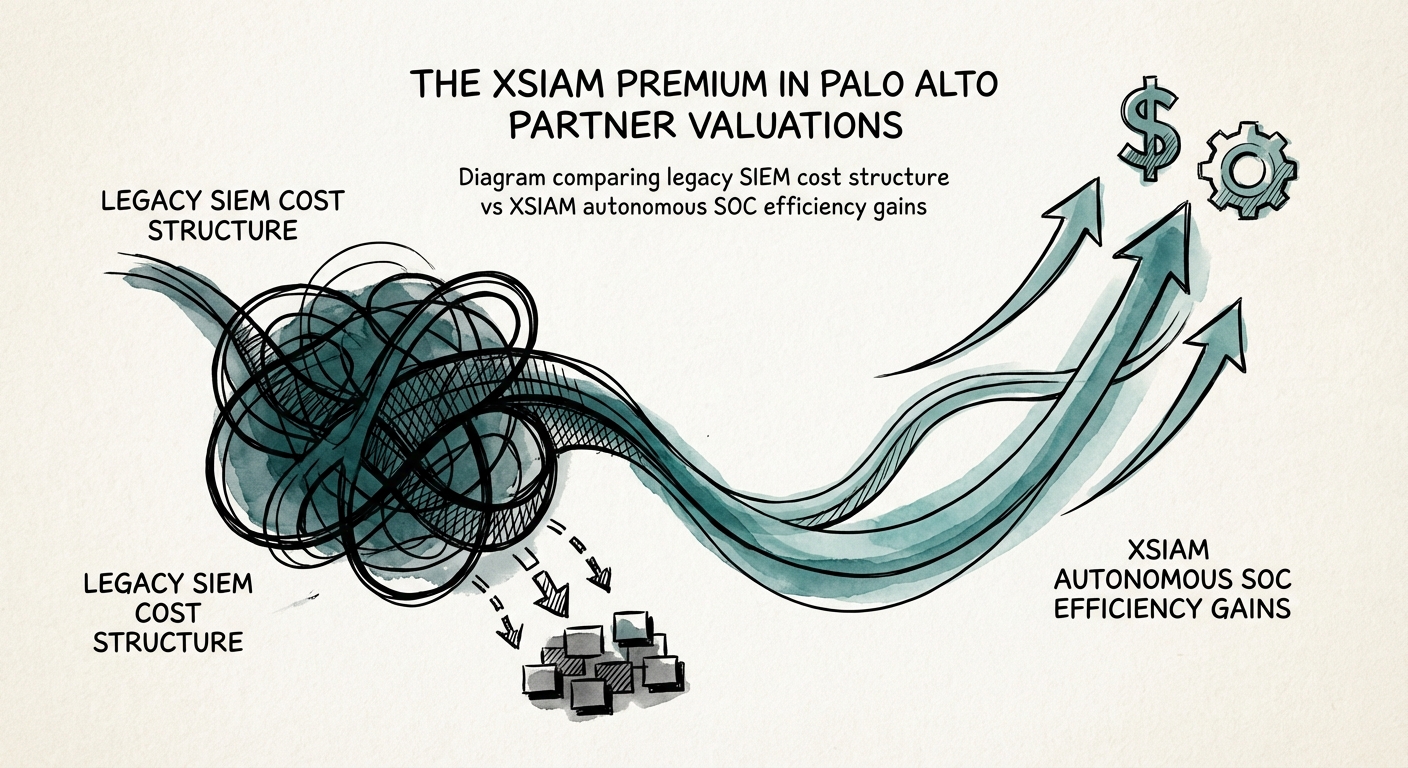

The Tale of Two Multiples: Firewall Shops vs. Autonomous SOCs

In the private equity ecosystem of 2026, not all Palo Alto Networks (PANW) partners are created equal. For the last decade, the valuation playbook for cybersecurity VARs and MSPs was relatively flat: if you sold hardware, you traded at 5x-7x EBITDA. If you wrapped managed services around it, you might stretch to 9x. That math has fundamentally broken with the rise of Cortex XSIAM (Extended Security Intelligence and Automation Management).

We are now observing a bifurcation in the market that is leaving generalist partners behind. The “Strata Generalists”—partners primarily focused on firewall refreshes (NGFW) and basic network security—are seeing valuations compress toward traditional VAR multiples (6x-8x). Their revenue is lumpy, project-based, and increasingly commoditized as hardware cycles lengthen.

Conversely, partners with proven XSIAM specializations and active managed SOC (MDR) practices are trading at 14x-16x EBITDA. This is not a speculative premium; it is driven by the “platformization” economics that XSIAM enforces. Unlike a firewall, which sits at the perimeter, XSIAM displaces the nerve center of the enterprise—legacy SIEMs like Splunk or QRadar. Once a partner anchors a customer on XSIAM, they aren't just selling a license; they are taking over the entire security operation, often displacing 3-4 legacy vendors in a single stroke. PE buyers are paying double for this stickiness.

The legacy SIEM era is giving way to something fundamentally different. For our partners, XSIAM represents a shift from 'managing tools' to 'delivering outcomes.'

The Economics of Displacement: Why XSIAM Drives Valuation

The valuation premium isn't just about the technology; it's about the unit economics of the customer relationship. Legacy SIEM deployments were notorious for high churn and low margins due to ingestion costs and alert fatigue. XSIAM changes the partner's P&L structure in three specific ways that acquirers value highly.

1. The “Platformization” Wedge

When a partner wins an XSIAM deal, they rarely win just the SIEM. Data from 2025 indicates that XSIAM deployments drive a 4x attach rate for other high-margin Cortex modules (XDR, XSOAR, Expander). For an acquirer, this means the Customer Lifetime Value (CLTV) of an XSIAM client is 300% higher than a firewall-only client. The partner is no longer fighting for a renewal every three years; they are embedded in the daily workflow of the SOC.

2. Service Margin Expansion

Traditional MSSPs struggle to break 40% gross margins because they rely on armies of Level 1 analysts to stare at screens. XSIAM’s AI-driven automation allows specialized partners to run leaner SOCs. By automating the triage of Tier 1 alerts, partners can shift their labor mix toward high-bill-rate Threat Hunters and Incident Responders. This operational leverage pushes gross margins on managed services from the industry average of 45% toward 60%+, a profile that commands SaaS-like multiples.

3. The Splunk Replacement Cycle

The market is currently washing through a massive replacement cycle of legacy Splunk and QRadar implementations. Partners who have codified the process of migrating data lakes and detection rules from legacy SIEM to XSIAM possess a transferable IP asset. Due diligence teams are specifically looking for this “migration factory” capability. If your firm builds custom connectors and automation playbooks, that code is valued as IP, not just services revenue.

The Diagnostic: Are You an XSIAM Player or a Paper Tiger?

For Founders and PE Operating Partners, the danger lies in the “badge trap.” Palo Alto Networks has aggressively pushed certifications, leading to a surplus of partners who claim XSIAM expertise but lack delivery depth. In a sale process, sophisticated buyers will pressure-test this claim. If you want the 16x multiple, you must pass the following diagnostic.

1. The Production vs. Lab Ratio

Red Flag: You have 10 certified engineers, but only 2 active production deployments.

Green Flag: You have migrated >50,000 endpoints to XSIAM and handle >1TB of daily ingestion volume. Buyers value data gravity, not badge counts.

2. The “Outcome” Contract Mix

Red Flag: Your XSIAM revenue is 80% resale/implementation and 20% support.

Green Flag: Your contracts are structured as “Managed Detection and Response” (MDR) with SLAs on Mean Time to Respond (MTTR). This recurring revenue stream is the primary driver of the valuation premium.

3. The Proprietary Content Library

Red Flag: You rely 100% on out-of-the-box Palo Alto content packs.

Green Flag: You have a repository of proprietary XQL (Cortex Query Language) detection rules and custom XSOAR playbooks that you deploy to every new customer. This demonstrates that you own the “intelligence” layer, making your practice harder to replicate and harder to fire.

The window to establish this premium is narrowing. As the GSI (Global Systems Integrator) giants like Accenture and Deloitte aggressively pivot into the XSIAM space, mid-market partners must prove deep specialization to maintain their valuation lead. The 16x multiple is available, but only for those who have moved beyond selling licenses to selling autonomous security outcomes.