The practical answer

- Short answer

- Generalist RPA firms are stalling at 6x EBITDA while healthcare automation specialists command 14x. Here is the valuation gap analysis for 2026.

- Best fit

- Industry: Healthcare Automation. Function: M&A Valuation

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Average EBITDA multiple for specialized Healthcare Automation firms in 2025/26.

The Great Bifurcation in RPA Valuations

In the early days of Robotic Process Automation (RPA), growth was the only metric that mattered. If you could show 50% year-over-year revenue growth implementing UiPath bots for finance and HR departments, you could command a premium multiple. That era is over. As we move through 2026, the market has bifurcated. Generalist RPA implementation firms—those building generic "invoice processing" bots for any industry—are seeing valuations compress to 6x-8x EBITDA. They are viewed as staff augmentation shops with low barriers to entry and high churn risks.

Conversely, UiPath partners that have pivoted to deep Healthcare Automation Specialization are trading at 12x-14x EBITDA. This is not a subtle shift; it is a fundamental re-rating of the asset class. Private Equity buyers and strategic acquirers (including large RCM platforms and payers) are no longer buying "capacity"; they are buying "capability." Specifically, the capability to navigate the complex, regulated, and high-stakes environment of healthcare operations.

The driver of this premium is the transition from "Task Automation" to "Outcome Automation." A generalist bot that saves 10 hours of work is a commodity. A specialized healthcare workflow that automates Revenue Cycle Management (RCM) denials, integrates bi-directionally with Epic or Cerner, and adheres to strict HIPAA/HITRUST standards is a strategic asset. Our analysis of 2025-2026 deal flow indicates that firms with proprietary healthcare IP (e.g., pre-built connectors for payer portals, automated clinical documentation improvement) are receiving LOIs with valuations nearly double that of their generalist peers.

Healthcare automation buyers are not only underwriting capacity. They are underwriting domain depth, compliance readiness, and repeatable workflows inside revenue cycle and clinical operations.

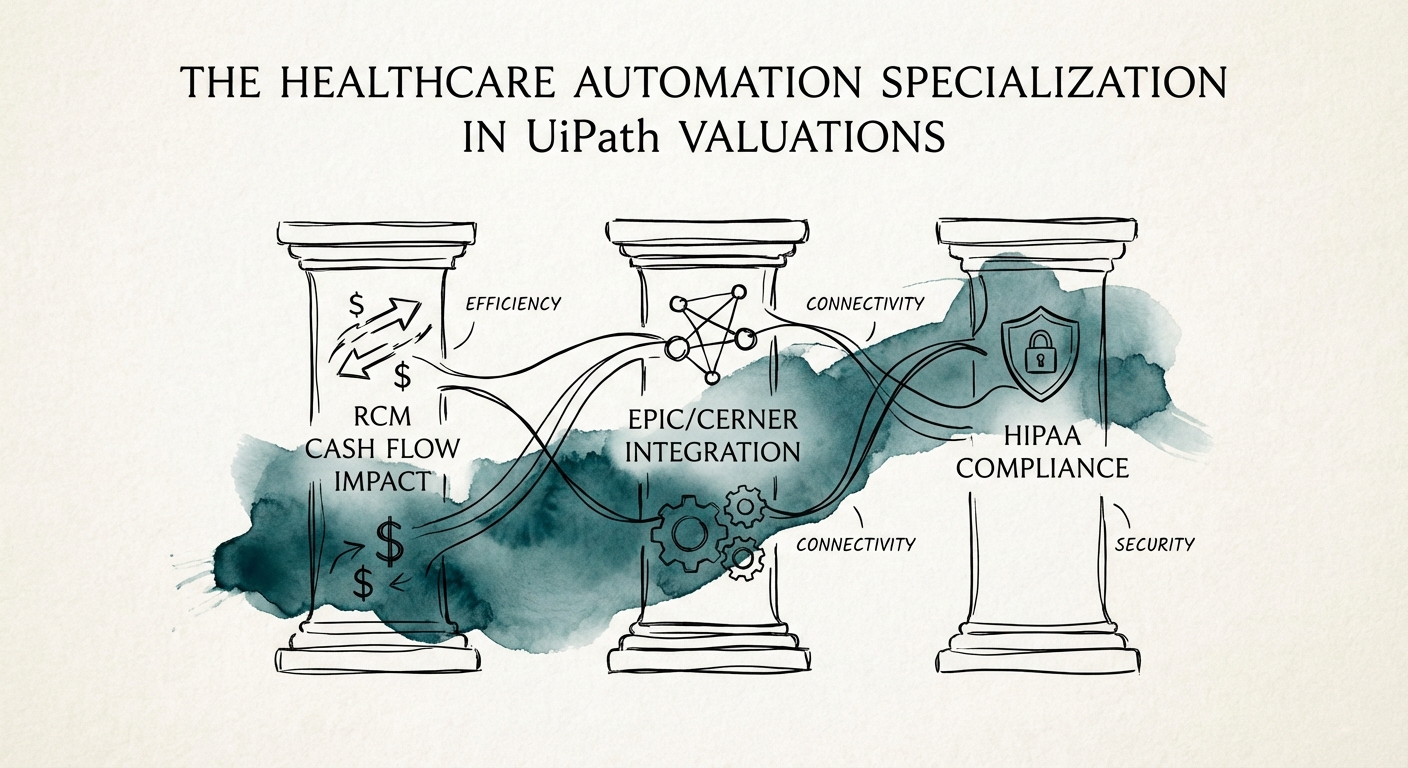

The Three Pillars of the 14x Multiple

Why does a healthcare focus drive such a dramatic valuation delta? It comes down to defensibility and revenue quality. A generalist UiPath partner competes with every other generalist and, increasingly, with offshore delivery centers. A healthcare specialist builds a moat that is difficult to cross. This moat is constructed of three specific components that due diligence teams scrutinize.

1. The RCM "Cash Flow" Engine

Healthcare providers are facing unprecedented margin pressure. The "must-have" automation solutions are those that directly impact cash flow. Partners specializing in Revenue Cycle Management (RCM)—automating claims processing, eligibility verification, and denial management—are effectively selling money. Automating a claims appeal process doesn't just save labor; it recovers revenue that would otherwise be lost. Multiples for tech-enabled RCM services have surged to 17x EBITDA for high-growth platforms, dragging specialized UiPath partners up with them.

2. The Integration Barrier (Epic/Cerner)

Generalist RPA relies on surface-level UI automation. Healthcare specialists leverage deep, often API-level integrations with Electronic Health Records (EHRs) like Epic and Oracle Health (Cerner). Building these integrations requires specialized talent and expensive sandbox environments. A partner that has pre-built, validated connectors for extracting patient data or updating charts without breaking clinical workflows commands a massive premium. It turns a "services" business into a "productized services" business.

3. The Compliance Moat

In healthcare, compliance is a competitive advantage. Generalist firms often fail healthcare vendor risk assessments due to a lack of HITRUST certification or insufficient data handling controls. Specialized partners that have embedded HIPAA compliance into their bot architecture and delivery models reduce the acquirer's risk profile. In M&A, risk reduction equals multiple expansion.

Strategic Pivot: From Generalist to Specialist

For PE operating partners and PE sponsors holding generalist automation firms, the path to a higher exit involves a deliberate pivot. You cannot simply market your way to a 14x multiple; you must re-architect your revenue mix. The 2026 playbook for maximizing exit value involves three steps:

- Stop Selling Horizontal: Cease investment in generic finance/HR automation sales. While these projects pay the bills, they dilute your valuation story. Redirect all GTM resources toward healthcare verticals.

- Productize Your IP: Do not just build bots for clients; build a library of reusable assets. If you solve "Prior Authorization" for one hospital, package that logic into a solution accelerator. Buyers pay for the IP that makes the next implementation 50% faster.

- Focus on "Agentic" AI: The future is not just scripted bots but AI agents that can reason. UiPath's push into agentic automation is most valuable in complex environments like healthcare. Partners demonstrating AI-driven clinical coding or autonomous patient scheduling are seeing the highest interest from strategic buyers.

The window to claim this premium is open, but the bar is rising. As RCM platforms consolidate, they are looking for the "missing piece"—the automation capability that unlocks the next 10% of margin. Position your firm as that high-precision key, and you move from being a commodity vendor to a strategic acquisition target.