Asset Deal vs. Stock Deal: Technology M&A Decision Guide

A board-level decision guide for choosing asset deal, stock deal, or hybrid structure in technology middle-market acquisitions.

Private equity sponsors, founder-sellers, CFOs, counsel, and operating partners structuring technology acquisitions.

Use this before LOI or during confirmatory diligence when contract assignment, IP ownership, customer concentration, tax exposure, or technical debt could change the deal structure.

Asset deal

The buyer wants selected assets, contracts, IP, customer relationships, and operating capabilities without inheriting the full liability stack.

Customer consent, employee transfer mechanics, IP assignment gaps, data portability, and business interruption between signing and Day 1.

Asset schedule, consent map, Day 1 continuity plan, and liability exclusion memo.

Stock deal

The operating entity, contracts, data rights, permits, and customer continuity are worth preserving intact.

Hidden liabilities, revenue recognition issues, cap table defects, technical debt, security exposure, and customer concentration.

Risk-adjusted purchase price bridge, indemnity issue list, and post-close cleanup roadmap.

Hybrid or pre-close cleanup

The strategic answer is clear but the company is not yet clean enough to support it.

IP held by contractors, software licenses that do not transfer, messy revenue schedules, and undocumented intercompany dependencies.

Pre-close remediation sprint with owner, deadline, and value-at-risk for each issue.

How to make the call

- Step 1

Map what the buyer must own

List the contracts, IP, employees, systems, data, and customer relationships that carry the acquisition thesis. Anything outside that operating perimeter should not drive structure.

- Step 2

Separate continuity risk from liability risk

Asset deals reduce inherited liabilities but can create Day 1 continuity risk. Stock deals preserve continuity but import the full operating and legal history.

- Step 3

Convert diligence issues into value-at-risk

Translate contract consent, IP assignment, revenue quality, security, and technical debt findings into purchase price, escrow, indemnity, or remediation implications.

- Step 4

Test Day 1 execution

A structure that wins on paper can lose customers if systems, support, data, or account ownership break on Day 1.

- Step 5

Choose the structure with an operating plan

The right structure is the one that the management team can execute without destroying the value the buyer is paying for.

Technology acquisitions are not just legal structures. They are operating structures. A buyer can win the liability argument and still lose the customer base if assignment, support, data, or platform continuity breaks after close.

The asset-deal-versus-stock-deal decision should start with the operating thesis: what must the buyer own, what must remain uninterrupted, and what risk is cheaper to remediate than to avoid.

The operating test

Use an asset deal when selection matters more than continuity. Use a stock deal when continuity matters more than liability isolation. Use a hybrid or pre-close cleanup sprint when the right structure is obvious but the company is not yet clean enough to support it.

The decisive questions are practical:

- Which contracts require consent?

- Where is the IP actually owned?

- Which systems must keep running on Day 1?

- Which employees carry customer, platform, or delivery continuity?

- Which liabilities are unknowable before close?

Where diligence changes structure

Financial diligence tells you what the company reports earning. Technical and operating diligence tells you whether the buyer can keep earning it after close.

For software and tech-enabled services firms, structure often changes when diligence finds contract assignment limits, third-party license restrictions, contractor-created IP, undocumented data dependencies, SOC 2 or security gaps, or revenue quality issues that change the risk profile.

Operator rule

Do not choose the structure that only looks clean in the purchase agreement. Choose the structure that preserves the value driver, prices the residual risk, and gives the post-close team an executable Day 1 plan.

Where the decision turns into work

Transaction Advisory Services

Operator-led buy-side and sell-side diligence for technology middle-market deals. Financial rigor, technical diligence, and integration risk in one workstream.

Valuations

Credible valuation work for SaaS, services, IP, ARR/MRR, cap tables, and exit readiness in technology middle-market transactions.

Investment Banking

Sell-side readiness, capital raise preparation, data-room cleanup, and operating narrative for technology companies preparing for buyers or investors.

Frequently asked

- Is an asset deal always safer for a buyer?

- No. Asset deals can reduce inherited liabilities, but in technology companies they can also create customer-consent, IP-transfer, data-rights, and operating-continuity risk.

- When does a stock deal make more sense?

- A stock deal often fits when customer contracts, data rights, permits, and operating continuity are central to the acquisition thesis and the diligence issues can be priced or remediated.

- What should be decided before LOI?

- The buyer should know which assets and contracts carry the thesis, which liabilities must be excluded or priced, and which Day 1 dependencies could disrupt revenue.

Articles that support the decision

BRIEF · TECHNICAL DEBT

The Margin That Wasn't There: Auditing AI Vendor Dependency Before You Sign

A SaaS target's 82% gross margin can hide a single-vendor API bill that quietly halves it. How to diligence AI dependency, model drift, and COGS before LOI.

349% Increase in AI Infrastructure COGS

BRIEF · EXIT READINESS

Your AI Model Is Worth $0 If You Can't Trace the Training Data

Acquirers discount AI IP up to 60% when data provenance is murky. How to prove lineage on your models and training sets before a PE deal team arrives.

60% Valuation haircut on undocumented AI IP

BRIEF · TECHNICAL DEBT

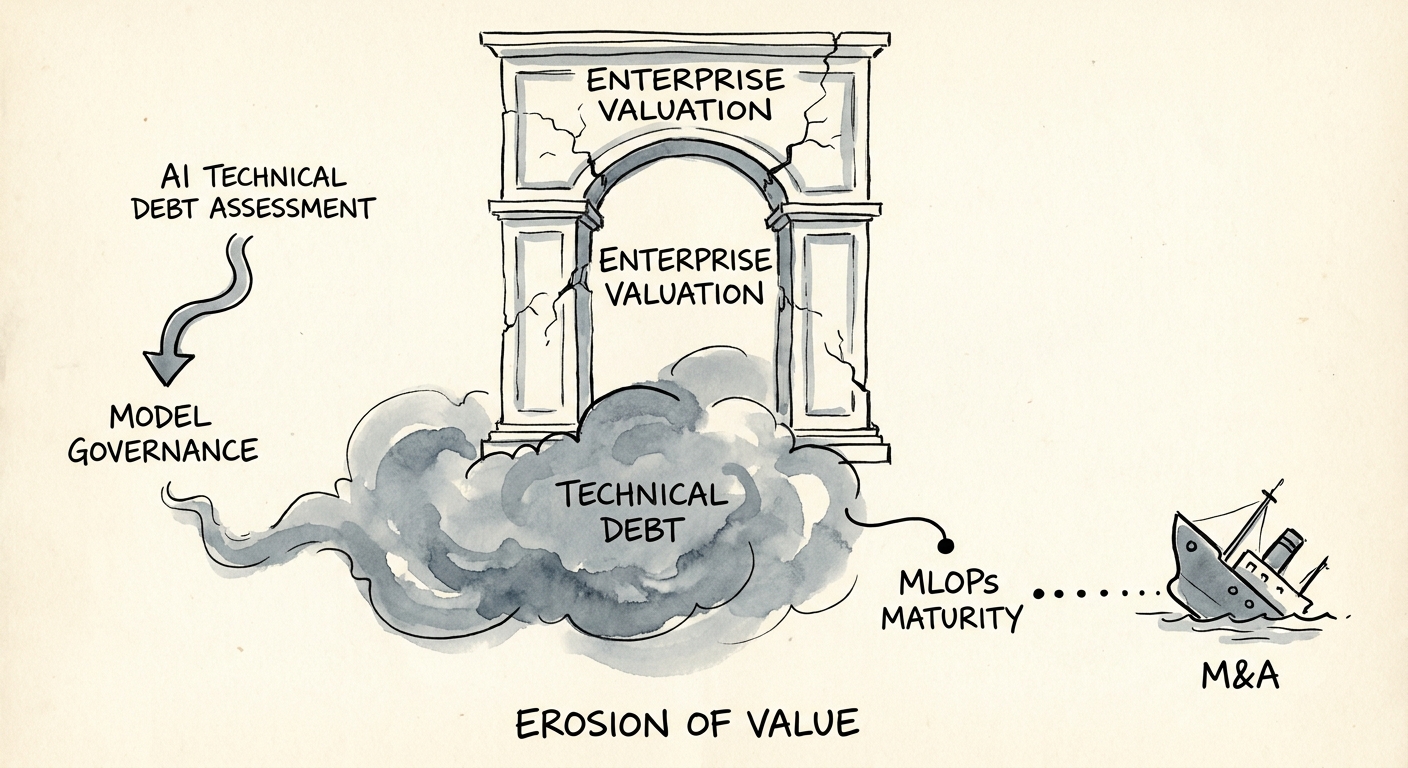

The MLOps Audit: How to Price an AI Target Before the Models Quietly Rot

AI targets don't fail in the codebase—they fail in the retraining pipeline. A buyer's field guide to auditing MLOps maturity, model drift, and registry gaps.

400% Maintenance vs. Development Cost Ratio for Ungoverned AI

BRIEF · TECHNICAL DEBT

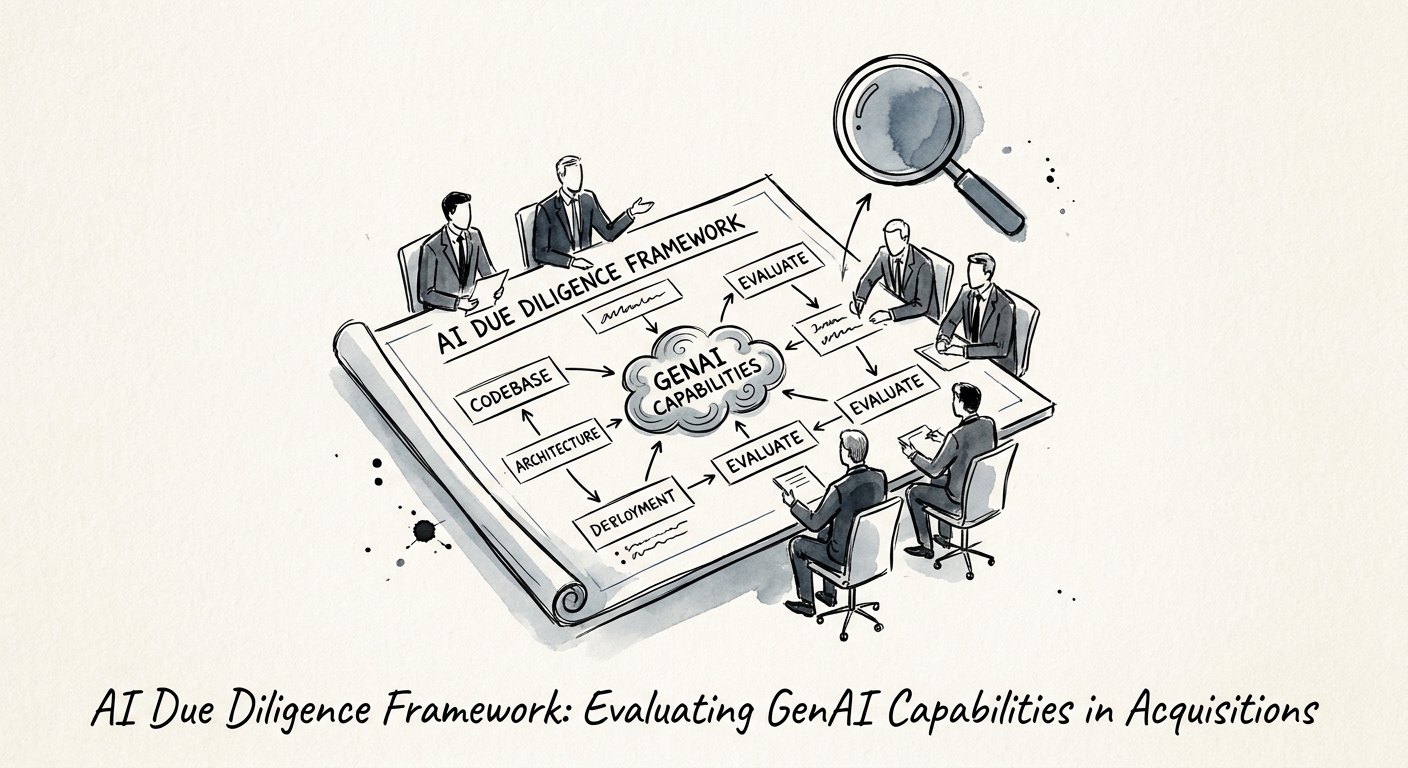

How to Diligence a GenAI Acquisition: Reading the CIM Against the Inference Bill

A PE diligence playbook for tech M&A: separate a real GenAI moat from a $25/month API wrapper, audit the IP chain, and price inference cost before you sign.

95% GenAI Pilot Failure Rate

BRIEF · TECHNICAL DEBT

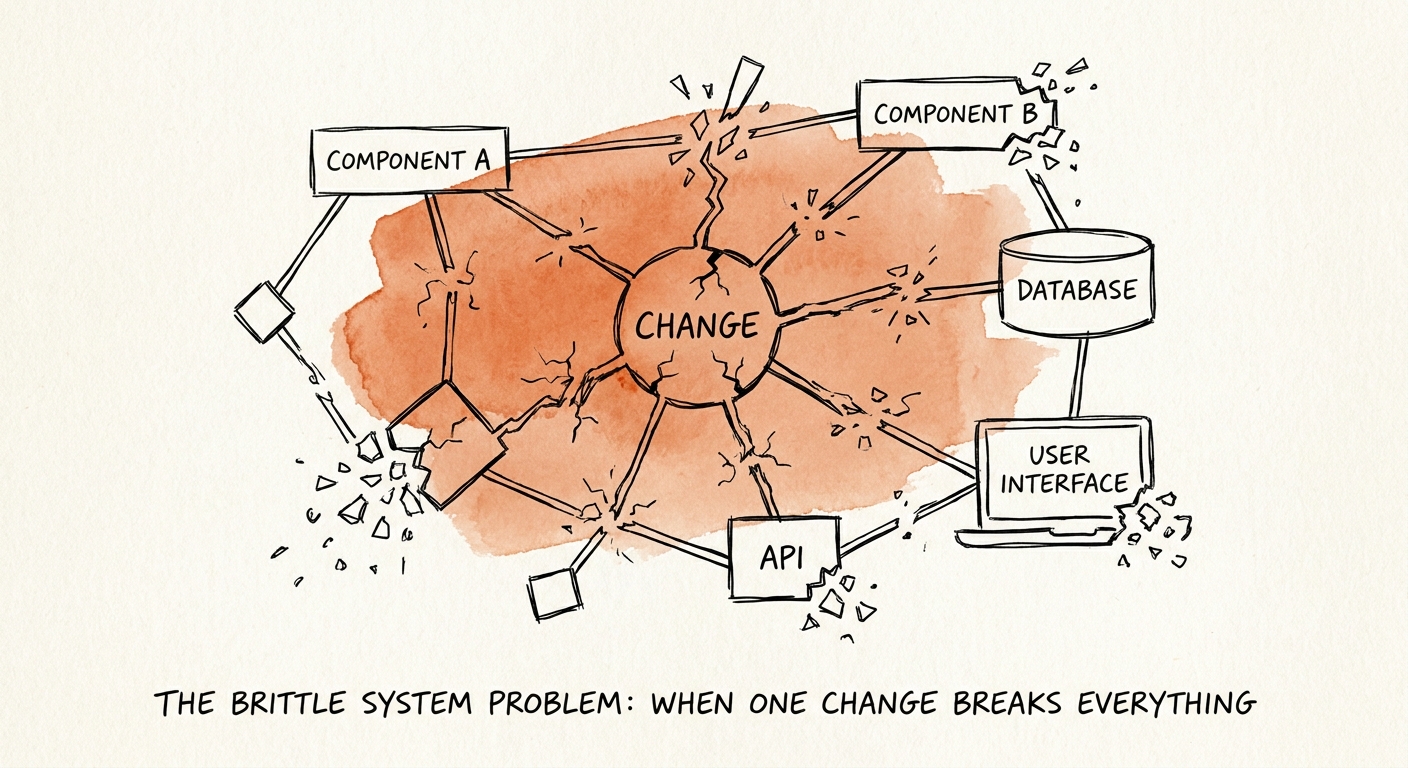

The Brittle System Problem: When a Dashboard Tweak Takes Down Billing

A two-line change to a reporting page shouldn't crash your payment gateway. When it can, buyers cut the price. Here's how brittleness becomes a 22% discount.

22% M&A Valuation Discount Applied to Brittle Architectures

BRIEF · TECHNICAL DEBT

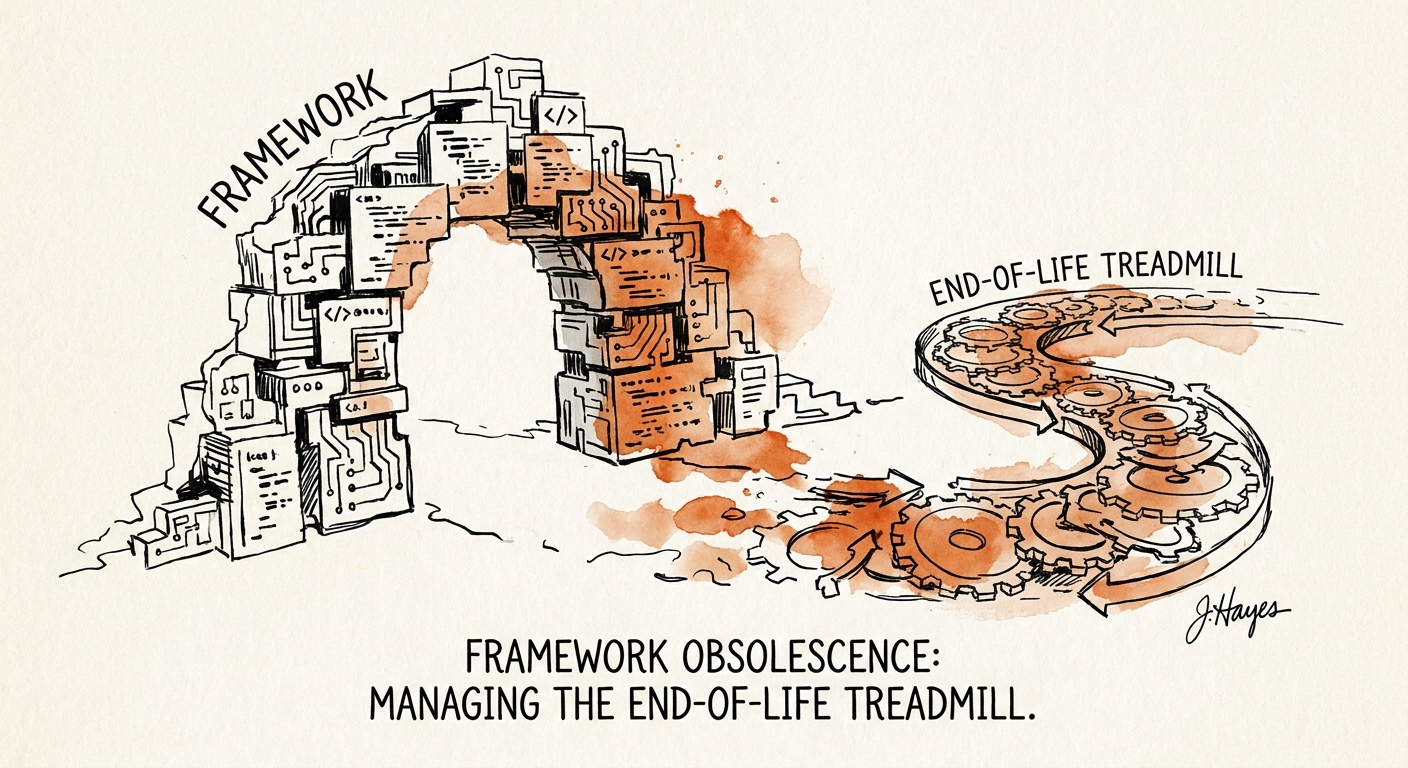

The End-of-Life Treadmill: How Dead Frameworks Sink SaaS Valuations

A frozen framework version is a diligence landmine. How SaaS leaders inventory end-of-life dependencies and run AI-assisted migration without freezing the roadmap.

EOL register first control for framework obsolescence