The practical answer

- Short answer

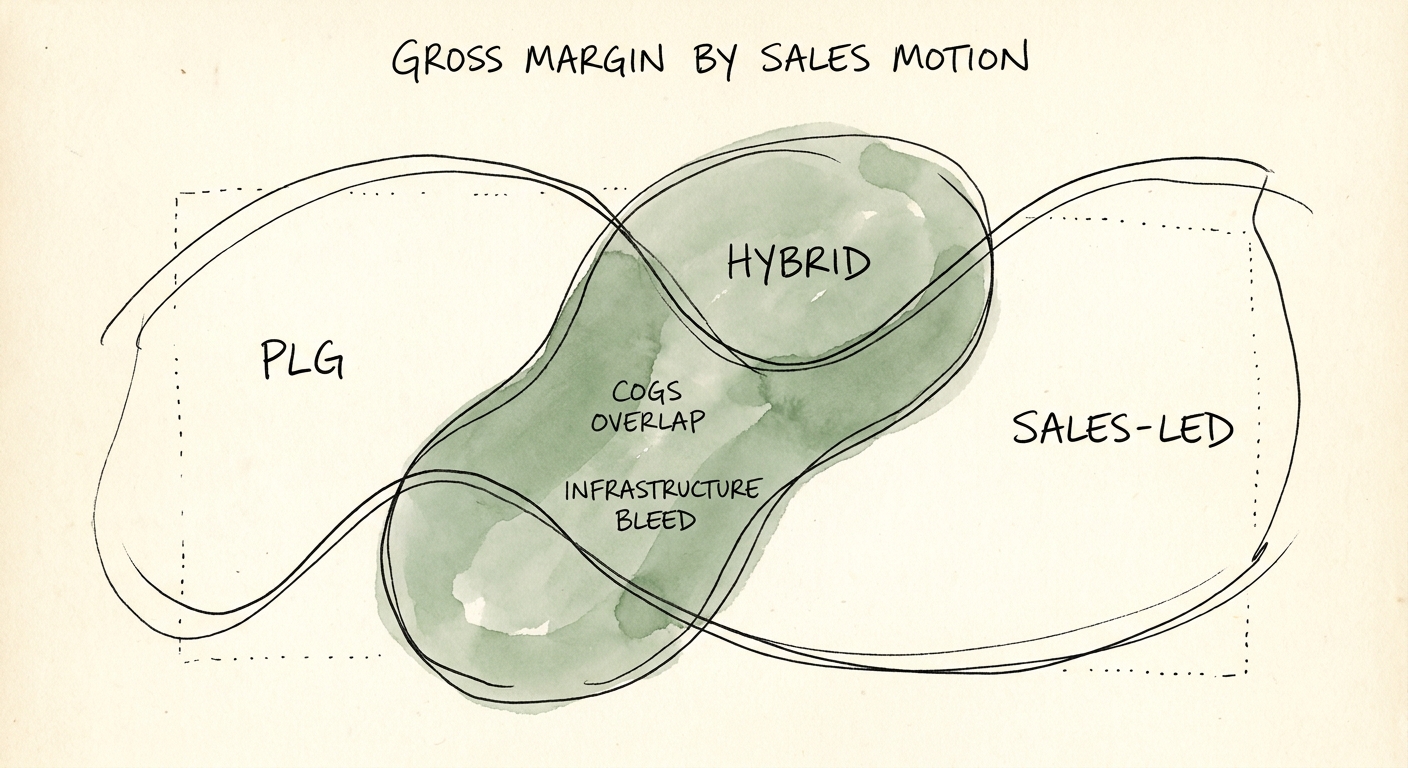

- Pure PLG SaaS averages 68.4% gross margin, not 90%. Here's where the cost hides, why the hybrid pivot makes it worse, and how to re-tag COGS before a buyer does.

- Best fit

- Industry: B2B SaaS. Function: Finance & Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 14.1% Gross margin bleed to unallocated cloud computing in hybrid SaaS models.

The board deck said 89% gross margin. The data room said 68%.

Here is the moment that ends the product-led growth fairy tale. A $40M ARR developer-tooling company is mid-process with a strategic acquirer. The pitch was the usual one: the software sells itself, users swipe a card, the gross margin is basically a software royalty. The deck showed high-80s. Then a diligence analyst asked one question nobody internally had asked in two years: which line item pays for the free tier?

It turned out the free-tier cloud hosting, the automated onboarding pipeline, and the telemetry ingestion that powers the in-product analytics were all sitting inside Research & Development. Reclassify them as what they actually are — the cost of delivering the baseline product experience — and roughly 18 points of revenue moved into Cost of Goods Sold overnight. The real number wasn't high-80s. It was right at the line that PitchBook's 2026 Global SaaS Financial Metrics reports for pure PLG companies under $50M ARR: a 68.4% gross margin, nearly ten full points below their sales-led peers.

This is the part founders refuse to internalize. In a self-serve motion, the "salesperson" is your infrastructure. The user who signs up at 11pm without ever talking to a human is still consuming compute, storage, and engineering hours building the sandbox, the tooltips, the usage dashboards, and the rate limiters that make self-serve feel free. None of that is free. It just doesn't generate an invoice with a rep's name on it, so it drifts into R&D where it quietly flatters the margin. Gartner's 2025 SaaS Sales Efficiency Benchmark shows why the old guard looks cleaner here — strict sales-led motions hold a 78.2% gross margin, largely because multi-year upfront contracts and paid implementation fees offset the human cost of onboarding before the customer ever logs in. PLG has no such offset. The onboarding is the product, and the product runs on a cloud meter that never stops.

A buyer doesn't care which deck your free-tier hosting costs live in. They'll pull every onboarding engineer and success rep back into COGS, recompute your margin, and price you off the number you were hiding from.

The hybrid pivot doesn't blend two margins. It pays for two cost structures at once.

Every PLG company eventually hits the same wall: $49-a-month swipes will not carry you to $100M ARR, and the board wants enterprise logos. So you bolt a top-down sales org onto the bottom-up product. This is where the margin damage stops being an accounting problem and becomes a structural one — because you are now funding two completely different ways of delivering software, simultaneously, and neither one subsidizes the other.

Picture the cost stack on a single quarter. You're still paying the full cloud bill for tens of thousands of free and low-tier accounts that may never convert. On top of that, you've added $250K-OTE enterprise account executives, and behind them, the cost nobody budgeted for: humans who exist to untangle the deployment messes that automated onboarding created inside your biggest accounts. McKinsey's 2025 Enterprise Software Cost Study puts the combined drag at 14.1% of gross margin lost to unallocated cloud computing and duplicated customer success effort. That's not a rounding error. That's the difference between a premium asset and a discounted one.

The mechanism is worth naming precisely, because it's specific to this collision. Your AEs close enterprise deals by promising custom integrations — SSO quirks, on-prem connectors, a non-standard data residency requirement. Each promise forks your standardized PLG codebase. To keep those forks alive you hire DevOps engineers to babysit bespoke environments, and every one of those environments becomes permanent weight on the infrastructure bill. The self-serve product was valuable precisely because one codebase served everyone at near-zero marginal cost; the enterprise motion's entire value is in being willing to break that. Forrester's 2026 Product-Led Growth Infrastructure Report finds customer success infrastructure and dedicated enterprise support headcount alone eat 9.3% of top-line revenue in hybrid product-led motions. The two engines aren't combining. They're competing for the same P&L, and the customer never sees the fight — they just see a margin line that keeps sinking while the ARR chart goes up and to the right.

What to actually do before a buyer re-tags it for you

The fix is not a spreadsheet adjustment. It's a delivery-architecture decision, and you have a roughly 90-day window to make it look deliberate instead of cornered. Three moves, in order.

Month one: tag every instance to a tier. Put your CFO and CTO in a room with the raw cloud bill and don't let them out until every compute, storage, and data-egress line is tagged to a customer tier — free, self-serve, enterprise. You cannot manage a cost-to-serve you've never measured per cohort, and right now your free tier's true cost is hiding inside a single aggregate AWS invoice. The first time you see free-tier cost-to-serve isolated, you'll understand which dormant accounts to prune and which usage patterns to rate-limit.

Month two: fix the comp plan that's hiding the cost. Rewrite customer success compensation to reward expansion revenue, not ticket deflection. That single change lets you legitimately classify those salaries as Sales & Marketing under ASC 606 instead of leaving them as a soft COGS expense — but only if the role genuinely drives expansion. Done honestly, it's defensible in diligence. Done as a relabeling trick, it's the first thing an analyst reverses.

Month three: set a hard margin floor on enterprise deals. No custom integration gets promised, and no Docusign goes out, until the deal clears a non-negotiable cost-to-serve floor. The AE who wants to fork the codebase for a logo has to own the infrastructure cost of that fork in the deal margin. This is the discipline that keeps the hybrid motion from quietly converting every win into a margin loss.

The reason this is urgent and not academic: a buyer will do every one of these calculations whether you've done them or not. Bain & Company's 2026 Tech M&A Multiples Report finds SaaS companies under the critical 75% gross margin threshold take a 2.4x exit multiple penalty in diligence. The acquirer pulls your onboarding engineers and success reps back into COGS, recomputes EBITDA on true delivery cost, and prices you off the honest number. If you've already done the re-architecture, you walk in with a clean, tier-tagged margin story and defend your multiple. If you haven't, you find out what your margin really is on the worst possible day — across a negotiating table, with leverage gone. Do the tagging now, while it's still your number to define.