The practical answer

- Short answer

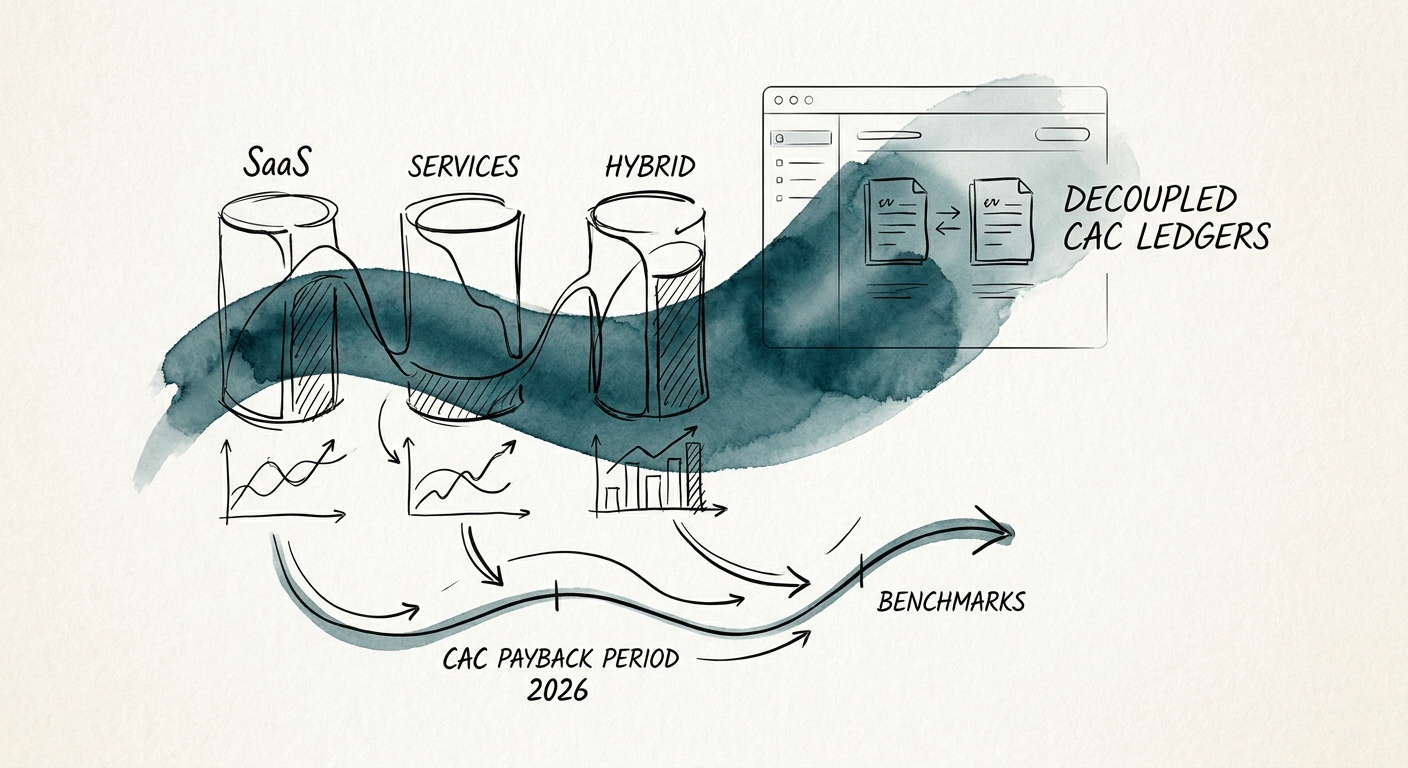

- 2026 CAC payback benchmarks for SaaS (21.4 mo), services (4.2 mo), and hybrid models — and why one blended number hides a cash trough acquirers will find.

- Best fit

- Industry: B2B Software & IT Services. Function: Finance & Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 21.4 Months median CAC payback for pure-play mid-market B2B SaaS in 2026.

One number, two completely different businesses

A $40M ARR hybrid platform we worked with reported a clean 14-month blended CAC payback to its board for two years. Everyone relaxed. The software was "efficient," growth looked healthy, and nobody asked the next question. The next question — the one a financial buyer asks in week one of diligence — was simple: how long does each dollar of acquisition spend actually take to come back, by revenue line? Once we split it, the 14 months evaporated. The software engine was taking 24 months to recover its sales-and-marketing load. The services arm came back in roughly three. The "efficient" 14-month figure was just the weighted average of a stalling software business and a fast-cash services shop, mashed together until neither was visible.

This is the specific failure mode of hybrid tech firms — companies pairing a proprietary software platform with heavy implementation, integration, or managed delivery. SaaS, pure services, and hybrid are not three flavors of the same metric. They have fundamentally different cash velocities, and a single payback number lies about all three at once. Start with the two clean cases. Per Gartner's 2026 SaaS Sales Efficiency Benchmark, the median CAC payback for pure-play mid-market B2B SaaS has stretched to 21.4 months — past the old 18-month ceiling — as procurement cycles lengthen and outbound gets more expensive. On the other end, McKinsey's 2026 IT Services Margin Report puts top-quartile IT services firms at a 4.2-month payback, because services bill implementation and roadmapping cash up front, often before the work even starts.

Now picture averaging 21.4 and 4.2. You can land on a comfortable number that describes no real cash account you can draw from. The software side is sitting in a deep, multi-quarter trough that the services side's quick cash is quietly papering over on the same P&L line. That's not efficiency. That's one business subsidizing the visibility of another's problem.

A blended CAC payback isn't a metric. It's the weighted average of a 24-month problem and a 3-month win, and the buyer's diligence team will separate them in an afternoon — so do it first.

Why the hybrid number is the one that bites

The reason hybrids get caught is the same reason they're tempting to report blended: the services cash arrives early and feels like proof the model works. It isn't proof — it's timing. Here's the arithmetic that matters. Say a deal closes as a $100K ARR software contract bundled with a mandatory $50K implementation SOW. The SOW invoices on signature. If you let that upfront services cash flow against your software acquisition spend, your software CAC payback looks dramatically faster than it is. You've used early services billing to suppress a number that should be telling you the software motion is in trouble.

This is exactly the adjustment private equity now forces. Bain & Company's 2026 B2B Software Unit Economics Playbook reports that 42% of top-tier PE firms now require onboarding and initial customer-success costs to be loaded into the core CAC calculation for hybrid firms during diligence. That single accounting change moves a typical hybrid payback from an idealized ~11 months to a real ~15.8 months — and that's before they pull the revenue lines apart. The other landmine is which margin you divide by. Use standard gross margin instead of a fully burdened contribution margin and you've ignored the solution architects, sales engineers, and pre-sales consultants who carry your enterprise deals across the line. Bessemer Venture Partners' 2026 Cloud Index — which defines a hybrid as any company drawing more than 30% of revenue from services — found those firms eat a roughly 12% Year-1 margin penalty largely because they never bill for pre-sales scoping and custom proofs of concept.

So the honest hybrid picture is rarely "14 months." It's two ledgers: a software line that may need 24 months to pay back, and a services line that returns cash in about three but runs on thin gross margins. Reported together, both numbers lie. Reported apart, you finally know which engine to fix. If you want the underlying mechanics of pulling hidden costs into the calculation, our breakdown on how to calculate true CAC payback period without hidden costs walks the formula.

The two-ledger fix you can start Monday

The move is to run dual-track reporting before anyone outside the company asks for it. One ledger tracks software acquisition cost and LTV. A separate ledger tracks services acquisition cost and per-project profitability. When the next bundled deal lands — the $100K software plus $50K SOW — allocate the sales and marketing expense across the two revenue streams by actual effort and attribution, not by whatever makes the software number look good. The discipline isn't bookkeeping for its own sake; it's the difference between knowing your software motion needs work and discovering it the hard way when growth flattens and the services cash can no longer cover it.

Three things to do this week. First, pull your last four quarters and recompute CAC payback separately for software and services — even a rough split will usually surprise you. Second, confirm you're dividing by contribution margin that includes pre-sales engineering, not headline gross margin. Third, stress-test whether your reported "efficiency" survives the Bain adjustment — load onboarding and early CS cost into CAC and see where the hybrid number actually lands. If you want a second liquidity read while you're in the numbers, the SaaS quick ratio calculator shows whether growth is funded or borrowed, and our CAC payback benchmarks diagnostic guide covers the full method.

The payoff shows up at exit, and it's not small. PitchBook's Q1 2026 Tech M&A Valuation Report finds hybrid tech firms that maintain strictly decoupled software and services CAC reporting command a 2.4x valuation multiple premium over peers running blended ledgers. The logic is unsentimental: institutional acquirers pay for cash flow they can predict and discount hard for anything they have to footnote. A buyer's diligence team will separate your revenue lines in an afternoon regardless. The only question is whether they find the work already done — or find out you didn't know your own numbers.