The practical answer

- Short answer

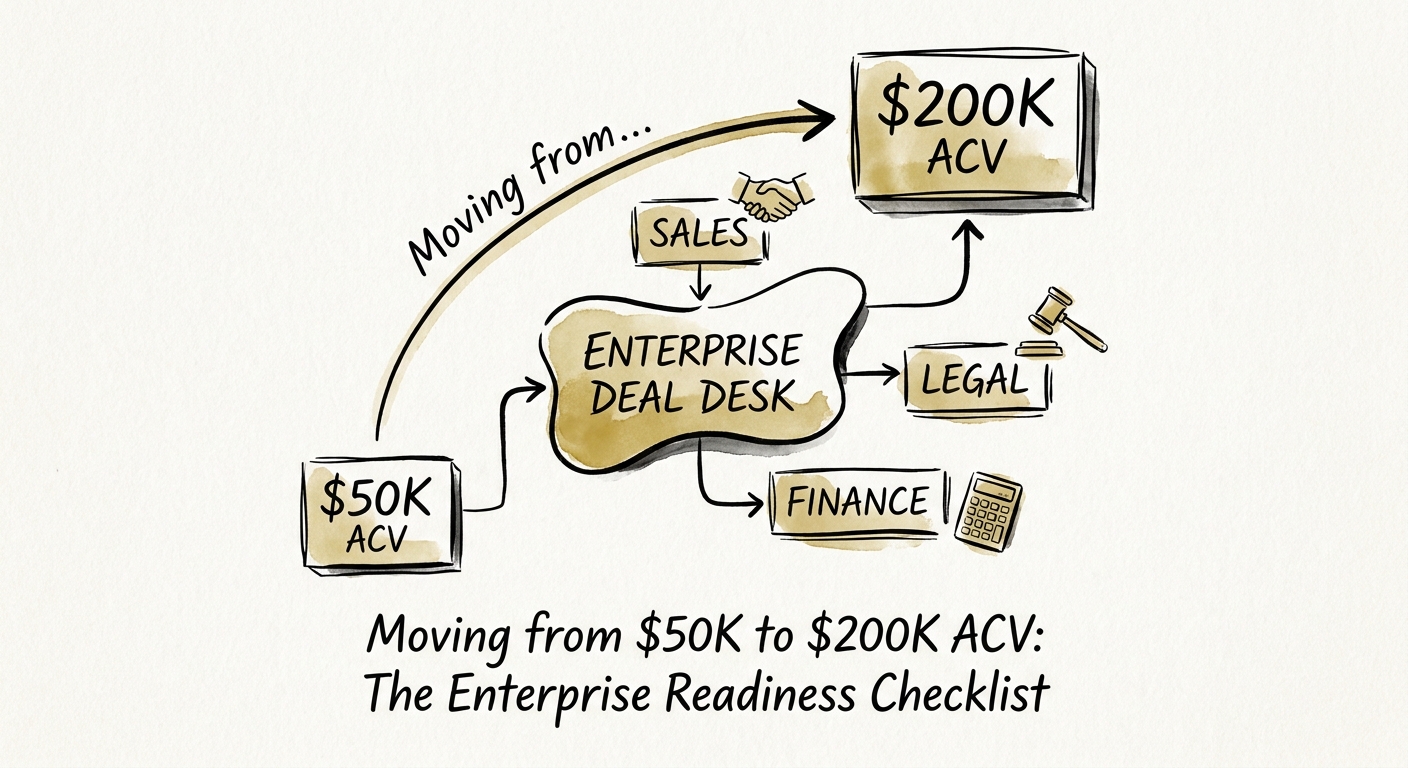

- The jump from $50K to $200K ACV quadruples your price and doubles your sales cycle. Here is what breaks first — and the checklist to clear before you commit.

- Best fit

- Industry: Enterprise Software. Function: Revenue Operations

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 45% Immediate drop in win rates when mid-market sales teams cross the $100,000 threshold.

The 4x price tag arrives with a 2x sales cycle — and nobody warns you

Here is the spreadsheet a founder showed me the week we started working together. Same product, same pitch deck, same two reps. Old plan: 40 deals at $50K. New plan: 10 deals at $200K. Same $2M, fewer logos, fatter ACV — the board loved it. What the spreadsheet didn't model is that a $200K deal is not a $50K deal multiplied by four. It is a different transaction decided by a different group of people on a different calendar, and the engine that printed $50K deals is the wrong shape for it.

The $50K deal closes because one technical champion runs an evaluation, likes what they see, and has signing authority or a fast path to it. Feature-led, single-threaded, decided in weeks. The $200K deal is a change-management project. Gartner's 2025 B2B Buyer Journey Benchmark puts deals over $100,000 at 11 to 14 stakeholders — procurement, security, legal, finance, the line-of-business owner, and a CISO who has never heard of you. Your champion is now one vote in a committee whose job is to find reasons not to sign. Bain & Company's 2025 Enterprise Sales Efficiency study found win rates drop roughly 45% the moment a mid-market team crosses the $100,000 ACV line. You don't grow into the enterprise; you fall off a cliff and have to climb back up with different gear.

The cruelest part is the pipeline math, because it's invisible until it isn't. At $50K you ran 3x coverage and hit your number. At $200K, deals slip across quarter boundaries on legal and security holds that have nothing to do with whether the buyer wants you — so 3x coverage produces a forecast that misses by a third. You need 5x just to be predictable, which means at the exact moment each deal costs more to chase, you need 60% more of them in flight. Before you touch the pricing page, read the deal velocity benchmarks by ACV and model what a doubled cycle does to your cash, not just your revenue.

A $50K deal closes when one champion likes your product. A $200K deal closes when fourteen strangers can't find a reason to say no. Those are different businesses.

Legal and security: the two queues where six-figure deals go to die

At $50K, your contract is a click-through. The buyer accepts your MSA, signs, and you're live. At $200K, the order is reversed: the buyer hands you their paper, their counsel redlines yours, and someone asks for unbounded liability, a custom uptime SLA with penalties, and a data-processing addendum that references a regulation your team has never read. If your sales reps have to forward every redline to a founder who answers between meetings, the deal sits. Enterprise buyers read silence as risk. The fix is structural: a deal desk where Sales, Legal, and Finance commit to a turnaround SLA on non-standard terms — I push clients to 48 hours — so a redline never becomes a two-week stall that lets a competitor catch up.

Security is the other queue, and it kills more $50K-to-$200K transitions than any product gap. Founders treat their SOC 2 Type II like a hall pass. It is the cover charge. Once you're past $100K, buyers want a recent third-party penetration test, answers to a 200-line security questionnaire, your sub-processor list, and your seat in their third-party risk management workflow. PwC's 2026 Enterprise Procurement and Infosec Report clocks enterprise infosec review at an average of 42 extra days on the deal cycle — and that's if you pass clean, with no remediation. The pattern I see on repeat: a champion verbally commits, the rep logs it as "Commit" for the quarter, and then procurement and security park the vendor in a 60-day onboarding purgatory that no AE forecast accounted for. The same trap is dissected in why security debt changes deals in due diligence: you are no longer selling software, you are selling whether a Fortune 500 CISO trusts your data-isolation architecture enough to put their name on it.

And the bill comes before the revenue. Cycles double, legal hours pile up, and a presales solutions engineer now lives inside every deal — so your customer acquisition cost balloons a quarter or two ahead of the bigger contract value hitting the P&L. EY's 2026 Enterprise SaaS Benchmarking Study shows CAC payback stretching out toward 22 months for companies climbing above $200K ACV. That is a working-capital trough, not a line on a slide. If you can't fund roughly a year of heavier spend before the new economics catch up, the upmarket move can starve the business that was already working.

You won the logo. Now the delivery math can eat the deal.

Closing the $200K contract is the easy half. The $50K customer onboarded themselves through a guided flow with a couple of CSM check-ins. The $200K customer expects data migration, custom API integrations, a training rollout for three departments, and an executive steering committee that meets every two weeks. If you handed implementation away free to "win the logo," you just signed up to lose money on your biggest account. McKinsey's 2025 SaaS Unit Economics report finds implementation eats about 22% of year-one revenue on $200K-plus deals. Bury that in a "free" rollout staffed by a CSM juggling 50 accounts and you've converted a flagship customer into a margin sinkhole — and a churn risk at month twelve, because under-resourced deployments don't go live, and deployments that don't go live don't renew.

So before you commit to this motion, clear three gates. They are unglamorous and they are non-negotiable.

One: multi-thread above the champion. A single relationship is a single point of failure, and at $200K the failure costs you a quarter. Your CEO needs a live line to the buyer's economic sponsor before the deal reaches procurement, so when your champion changes jobs — and over a nine-month cycle, they do — the deal survives. Two: stand up a real deal desk. A named owner and a committed SLA across Sales, Legal, and Finance to clear redlines and non-standard terms. Without it, every six-figure deal converges on one overloaded person and rots in the queue. Three: capitalize implementation as a priced service. Charge 15–20% of first-year ACV for professional services, staffed by deployment architects, not onboarding generalists. This protects the SaaS gross margin that a future buyer underwrites — bundle it free and you'll fail the Rule of 40 math a premium PE exit demands. If you're weighing this against going deeper in your current market instead, the horizontal vs. vertical expansion framework is the decision to make first.

The $50K-to-$200K crossing is where lifestyle SaaS becomes a venture-scale platform — or quietly bleeds out trying. The companies that make it stop relying on rep heroics and build a multi-department machine: multi-threaded relationships, a 48-hour deal desk, a security posture a CISO can sign off on, and implementation priced like the service it is. Run the checklist before you rewrite the pricing page, not after the first deal stalls in legal.