The practical answer

- Short answer

- Two Atlassian partners, same revenue, double the multiple. What buyers pay for in 2026: services mix, Marketplace IP, and a clean Cloud migration story.

- Best fit

- Industry: Technology Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x Target EBITDA multiple for specialized Atlassian partners.

Two partners walk into a diligence room

Picture two Atlassian Solution Partners, both doing roughly $14M in revenue, both with the same logo on their certificate wall. One walks out of a sale process at 6x EBITDA. The other clears 12x. The revenue line told you nothing. Everything that mattered was sitting one row down, in the revenue composition — and in a question every buyer now asks first: what happens to this business when Atlassian finishes turning the license renewal into a self-serve checkout?

That question has teeth in 2026. The shutdown of Server, the relentless push to Cloud, and the steady trimming of partner discounts on Data Center renewals have quietly converted the old reseller margin from an annuity into a melting ice cube. A firm whose P&L leans on pass-through license revenue isn't a consultancy to a private equity buyer — it's a billing relationship Atlassian could disintermediate with a feature flag. That's the firm that trades around 5x-7x EBITDA, with diligence teams hammering on customer concentration and asking, politely, how much of next year's gross profit is contractually safe. (The pattern is laid out in the Aventis Advisors Atlassian ecosystem M&A report.)

The 12x firm answered the disintermediation question before the buyer asked it. Its value doesn't live in moving licenses; it lives in problems Atlassian's product doesn't solve out of the box — Jira Align rollouts for SAFe at enterprise scale, ripping out a ServiceNow or BMC ITSM stack and standing up Jira Service Management in its place, and Cloud migrations gnarly enough that regulated customers (data residency, audit trails, app re-platforming) won't touch them without a specialist. Strategic acquirers and PE-backed consolidators — the Valiantys and Adaptavist tier — pay 10x-12x for that, because they're buying capability they can resell across a portfolio, not a renewal book that erodes the day the badge changes hands.

Buyers stopped asking what tier badge you carry the moment they realized your renewal margin was Atlassian's to cut. Now they ask one thing: when the licenses become a rounding error, what's left that they can't get from the next partner down the list?

The three numbers a buyer pulls before they read your deck

When a buyer's analyst opens your data room, they don't start with the narrative. They start by re-cutting your revenue to find out what you'd actually be worth if every license dollar vanished. Three figures decide whether the conversation continues at a premium.

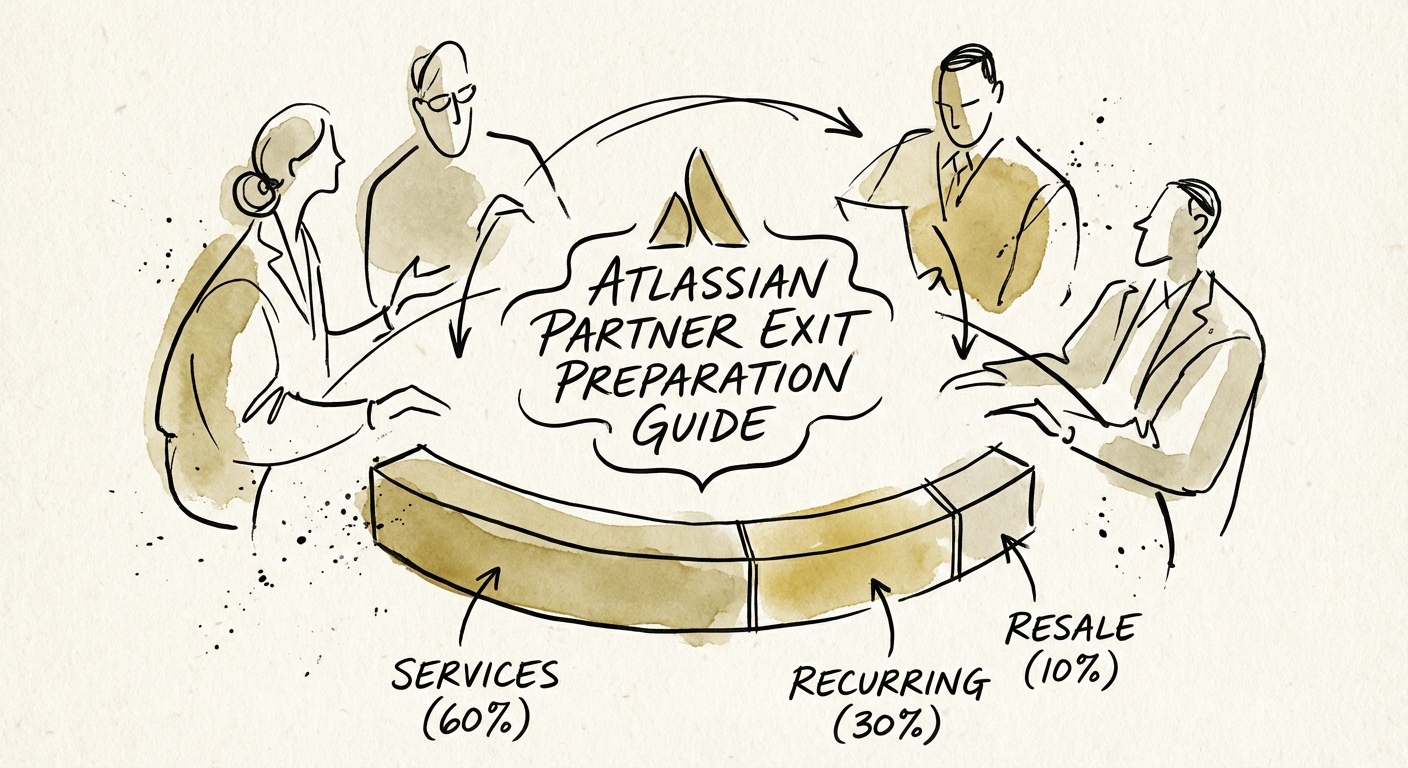

Services-to-resale mix: the 60/40 floor

The first thing diligence does is strip resale out entirely and re-run your margins on services alone. If you're 80% resale, the math is brutal and immediate — you're an outsourced sales channel wearing a consultancy's hat, and the model knows it. Buyers want to see at least 60% of revenue from professional and managed services, because that ratio proves you own the customer relationship rather than renting it from the transaction. Run this cut on your own numbers tonight; if services aren't a clear majority of gross profit, you've found the single largest lever on your multiple, and it takes time to move.

The recurring-revenue bridge that survives the project trough

Implementation revenue is lumpy by nature — a big migration lands, then a dry quarter follows. The partners that command premiums have built a bridge across that trough, and in the Atlassian world the bridge has a name you can monetize. Aim for 30%+ of gross profit from recurring sources: "always-on" managed administration and optimization contracts, plus — and this is the multiplier the generalist consultancy can never replicate — proprietary Marketplace apps. A niche app that solves a vertical-specific gap (think compliance tooling that lives inside Jira) is software margin riding on Atlassian's own distribution. Buyers price that line completely differently than your hourly book. Atlassian's own partner specialization program exists precisely because depth like this is what the ecosystem now rewards.

Utilization and realization: where artificial EBITDA hides

This is where founders get caught. A 75% billable-utilization target for delivery staff and 90%+ realization sound like operations trivia until diligence finds the write-offs. Every hour you quietly eat to "fix" a botched implementation is EBITDA you reported but never earned — and a sharp buyer reconstructs it from your time-tracking and discounts your number accordingly. If your team is bleeding non-billable hours patching delivery quality, your stated margin is fiction, and the quality-of-earnings analysis will say so in writing.

The 24-month repositioning, in the order it actually happens

You don't earn the higher multiple in the data room. You earn it in the two years before, by systematically removing the reasons a buyer would discount you. Start here, in this sequence.

First: get yourself out of the close

In most founder-led partner shops, the CEO is still the closer on every enterprise deal — and to a buyer that's not a strength, it's a key-man risk that walks out the door at the earnest-money payment. Install a sales leader and prove it: two clean quarters of quota attainment on real enterprise deals you didn't personally rescue. That single demonstration does more for your valuation than another year of top-line growth. (Our founder-extraction checklist walks the processes to hand off, in order.)

Second: turn your delivery method into an asset, not a person

Buyers pay for repeatable process; they discount for "hero" architects whose knowledge lives in their heads. Your approach to a Cloud migration or an ITSM cutover has to exist on paper — standardized SOWs, delivery playbooks, QA gates a mid-level consultant can execute without you on the call. That's the difference between selling a system and selling a roster of people who might resign post-close. The 36-month exit planning timeline sequences this work against the clock.

Third: clean up your own Jira before they audit it

Here's the one that's unique to your world, and the one that quietly torpedoes Atlassian partners specifically. Diligence will look at your instance — your time tracking, your resource planning, your CRM data in Jira and Atlas. And Atlassian partners are notorious for cobbler's-children chaos: the firm that sells operational rigor running its own delivery on a swamp of stale workflows and uncategorized tickets. When the people buying your expertise see that your internal systems contradict your pitch, every claim you've made gets re-examined. Make your own instance the reference architecture you'd demo to a prospect. The Valiantys-tier acquirers tracking this market (see their ongoing market analysis) read your internal hygiene as a direct proxy for delivery maturity — because it is.

Monday action: pull your trailing-twelve revenue and split it into resale, project services, managed/recurring, and Marketplace IP. That four-line breakdown is the first slide a buyer builds about you. Build it yourself, and you'll see your real multiple before anyone else does.