The practical answer

- Short answer

- Series B/C CEOs: stop arguing about code quality. Here's the formula to put a dollar-per-day price on delayed tech debt remediation, and defend it in the boardroom.

- Best fit

- Industry: B2B SaaS & Tech Services. Function: Engineering & Finance

- Operating path

- Technical Debt → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- $2.41T Annual cost of technical debt to US businesses (Accenture, 2025)

The number your VP Eng can't get past your CFO

Picture the Series C board meeting. Your VP of Engineering asks for two sprints to "pay down debt." Your CFO leans back and asks the only question that matters: "What does that buy us?" Your VP says something about "maintainability" and "developer happiness." The ask dies on the table. Again.

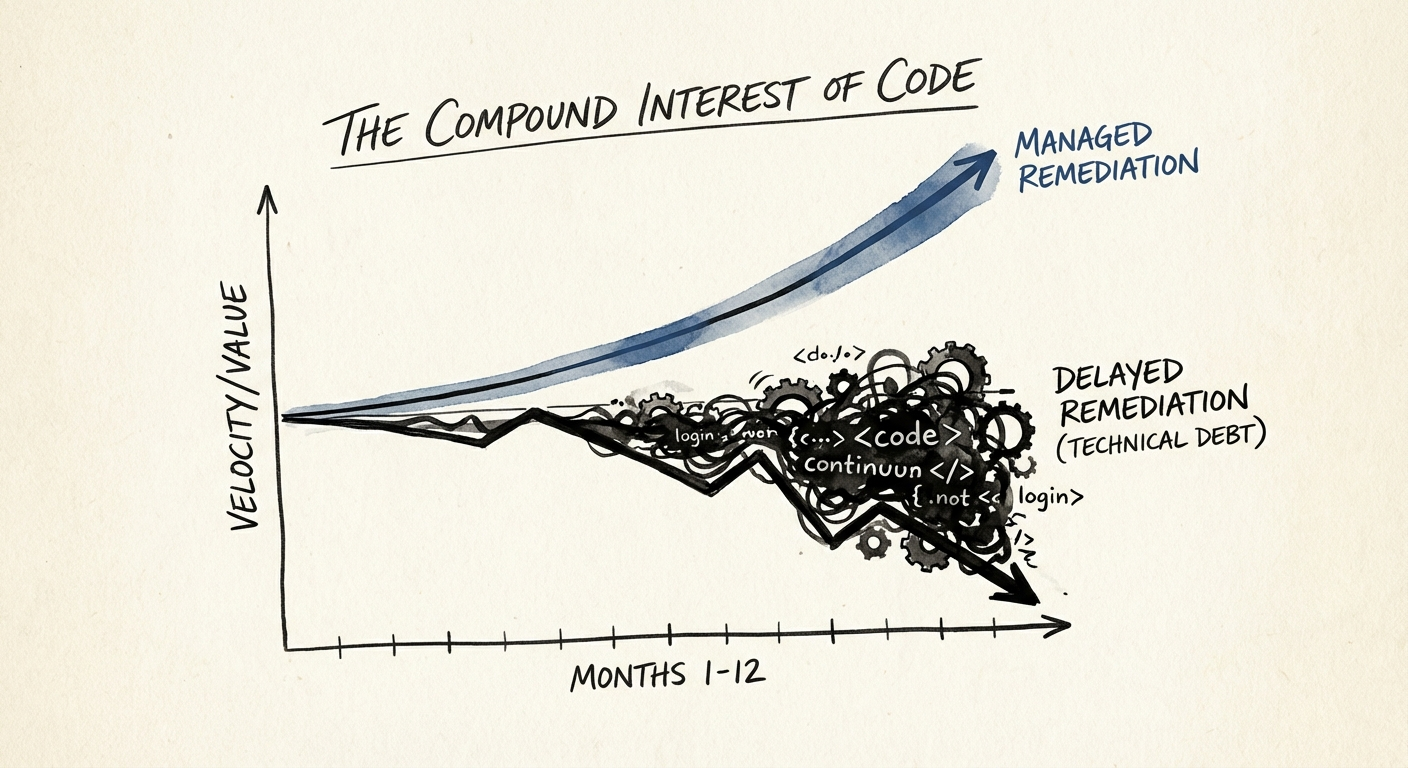

Here is why it keeps dying: engineering is asking for a budget in a currency the board doesn't spend. The board spends EBITDA, ARR, and burn multiple. "Spaghetti code" doesn't convert. So the debt compounds for another quarter, and the next ask is bigger.

The translation rate is brutal and well-documented. Stripe's research found developers spend up to 42% of their time on maintenance, bad code, and keeping the lights on (Stripe, "The Developer Coefficient"). At a Series B/C company that has just doubled headcount on a fragile codebase, that's not a productivity stat — it's nearly half your engineering payroll being burned before anyone ships a feature a customer asked for. You wouldn't tolerate a 42% line item labeled "rework" anywhere else in the P&L. You tolerate it here only because nobody has written the invoice.

Technical debt is not a code problem. It's a borrower's note against your future velocity, and the day a buyer reads it in diligence is the day it stops being free.

Write the invoice: Cost of Delay = (Vw + Io) × D

You don't authorize a refactor by winning an aesthetics debate. You authorize it by showing the daily price of not doing it. So put a meter on the delay. Two inputs, multiplied by how long you stall.

Vw — Velocity Waste. Take fully loaded engineering payroll. Multiply by the gap between your actual maintenance ratio and the ~20% a healthy Series B should run. Say you're a Series C with a $5M eng payroll, and your team admits 40% of their week is firefighting. That's $5M × (40% − 20%) = $1M a year spent standing still. Don't guess the ratio — pull it from the next section's sprint audit. (For turning this into a board-deck slide, see quantifying technical debt in dollars.)

Io — Innovation Opportunity. This is the bigger number, and the one founders skip. Gartner finds teams that actively manage debt ship roughly 50% faster (Gartner). Take the feature on your roadmap with a real ARR number attached — say a $2M expansion play. If debt pushes it from a Q1 launch to a Q3 launch, you didn't "lose two quarters of work." You lost two quarters of recognized revenue on those cohorts, plus the net-revenue-retention compounding you'll never recover, because the customer who churned in month four was never going to see the feature that would have saved them.

Multiply (Vw + Io) by D, the days you keep debating instead of deciding. McKinsey's analysis of tech-equity drag (McKinsey & Company) is the macro version of the same arithmetic: the cost isn't the cleanup, it's the interest accruing while you don't.

The bill comes due in the diligence room

Everything above is the operating cost. The real Series B/C killer shows up the day you raise your next round or sell. A growth investor doesn't just price your ARR — they price the cost of that ARR. If your growth runs on manual heroics instead of systems that scale, they bake the cleanup into the offer.

Call it the re-platforming haircut. A buyer who calculates they'll need $3M and 18 months to stabilize your platform post-close doesn't subtract $3M from your price. They apply a risk multiplier — 2x, 3x — because they're pricing execution risk, not just labor. That's how a $50M outcome quietly becomes a $41M outcome, and the gap traces directly back to the $500K refactor you deferred two years earlier. The debt was free right up until the moment someone with a checkbook read it.

Don't reach for the Grand Rewrite

The instinct, once the number lands, is to freeze the roadmap and rebuild from scratch. Don't. At Series B/C, stopping feature development is how you hand the category to a competitor while you "fix" things. Run a tax instead: carve a fixed 15–20% of every sprint for debt paydown, permanently, so the principal never compounds back to 42%. Keep your velocity solvent instead of declaring bankruptcy.

Do this Monday: Pull your last three sprints and tag every ticket as feature work or as "bug / fix / maintenance." If the maintenance bucket clears 25%, you're already paying the high-interest rate — you just haven't named it. Run the (Vw + Io) × D math on a single slide and bring it to the next board meeting. Stop arguing about code. Hand them the invoice.