The practical answer

- Short answer

- Single-trigger option acceleration isn't a perk—it's a poison pill. Learn why PE buyers demand double-trigger vesting and how to fix your cap table before the LOI.

- Best fit

- Industry: B2B SaaS. Function: Legal & HR

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 80% of PE-backed deals require Double-Trigger acceleration for management equity to align post-close retention.

The Single-Trigger 'Walk Away' Problem

In the early days of a startup, single-trigger acceleration feels like a no-brainer. You want to attract top talent, but you can’t pay market salaries, so you promise them: "If we get acquired, you get paid. 100%. Immediately." It seems fair. It seems generous. But to a Private Equity buyer, this provision is a "poison pill" that can kill your deal or force a painful re-trade.

When a PE firm acquires your company, they aren't just buying your code or your customer list; they are buying your team. They need the engineers to maintain the product and the sales leaders to hit the bookings forecast. If your option plan features single-trigger acceleration, every unvested option fully vests the moment the deal closes. This creates a perverse incentive structure: your key employees receive a life-changing windfall on Friday and have zero financial reason to show up on Monday.

The Economics of the Re-Trade

Buyers will not accept the risk of buying an "empty building." If your diligence reveals widespread single-trigger acceleration, the buyer will force a "Retention Re-Trade." They will calculate the cost of a new retention package required to keep the team—often 10-20% of the total deal value—and they will insist that this cost comes out of the purchase price (i.e., the seller's proceeds), not their own pocket. Effectively, you end up paying for your employees' retention twice: once via the accelerated options, and again via the price reduction.

Single-trigger acceleration creates a 'walk-away' incentive that no PE buyer will accept. If your team vests 100% on closing, you haven't sold a company; you've sold an empty building.

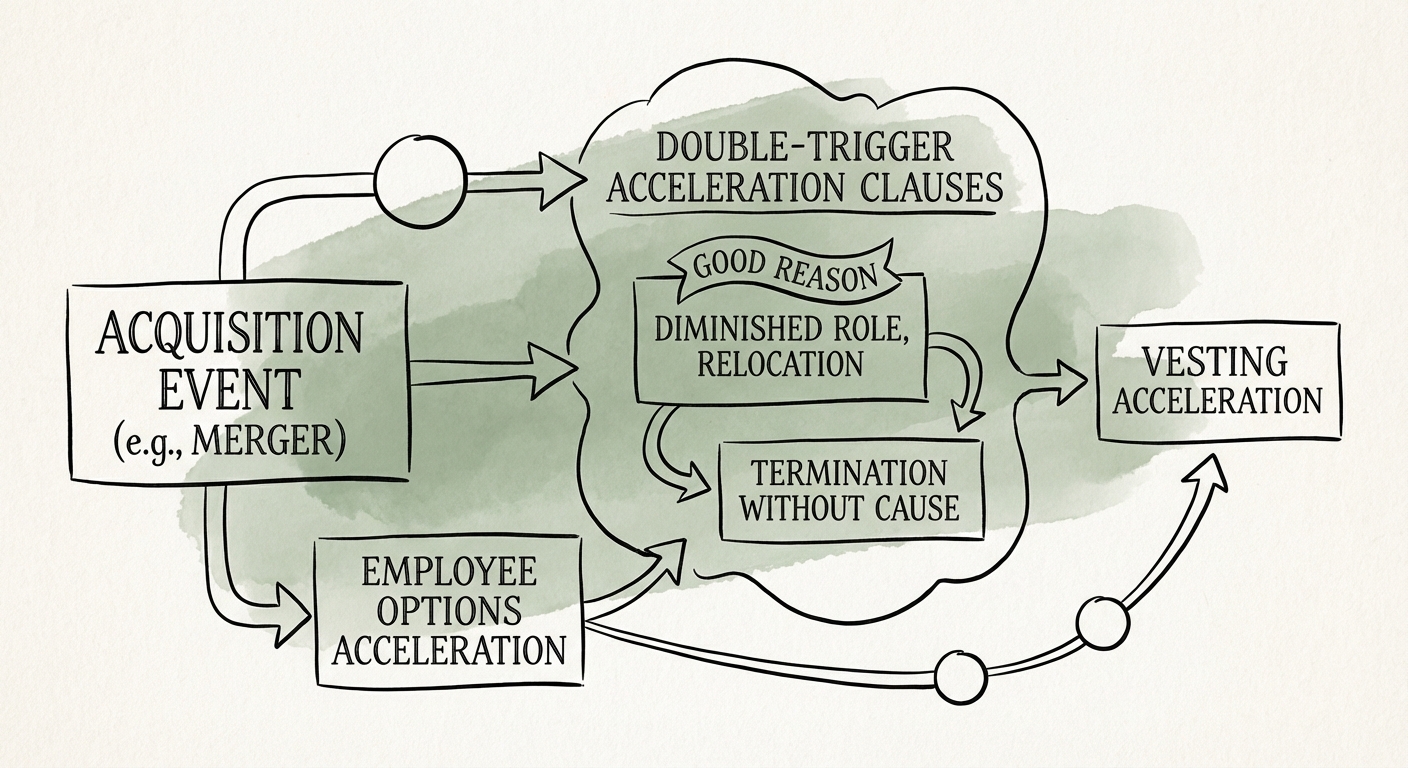

Double-Trigger: The Market Standard

The standard for private equity and strategic acquirers is Double-Trigger Acceleration. This structure aligns the interests of the employee, the founder, and the buyer by requiring two distinct events for acceleration to occur:

- The Trigger Event (Change of Control): The acquisition actually closes.

- The Qualifying Termination: The employee is terminated without "Cause" or resigns for "Good Reason" within a specific window (usually 12-18 months) post-close.

This structure protects the employee from being fired just so the buyer can save on equity payouts, but it also protects the buyer by ensuring the team stays motivated. If the employee leaves voluntarily to sit on a beach, they forfeit their unvested options—just as they would have without the acquisition.

The 'Good Reason' Battleground

The nuance in double-trigger provisions lies in the definition of "Good Reason." A loose definition allows employees to trigger their own acceleration by claiming a minor role change is a "constructive termination." A tight definition forces them to stay even if their role becomes unrecognizable. In 2026 PE deals, "Good Reason" is typically defined as:

- A material reduction in base salary (usually >10%).

- A forced relocation of more than 50 miles.

- A material diminution in title or authority (this is the most negotiated point).

The Diagnostic: Cleaning Up the Cap Table Before the LOI

Do not wait for the buyer's legal counsel to find your single-trigger grants during due diligence. By then, you have lost leverage. Conduct a "Trigger Audit" of your stock option plan (SOP) and individual grant agreements now. If you find single-trigger provisions for key executives, execute a "Waiver and Exchange" strategy before you go to market.

The Waiver and Exchange Playbook

You cannot unilaterally revoke single-trigger rights; that is a breach of contract. Instead, you must negotiate an exchange. Approach the affected executives with a proposal: exchange their single-trigger acceleration for a double-trigger provision, plus a sweetener. The sweetener could be a small cash bonus at closing or a refresh grant of Restricted Stock Units (RSUs) in the new entity.

While this conversation is difficult, it is far better to have it as a CEO aligning the team for a successful exit than to have a buyer force it as a condition of closing. The latter breeds resentment and makes your leadership team feel like the acquisition is "taking something away" from them, rather than rewarding their success.