The practical answer

- Short answer

- The post-close consulting agreement is the deal document most likely to trigger a 20% 409A penalty or create a Shadow CEO. Here's how to structure it right.

- Best fit

- Industry: Private Equity / M&A. Function: Legal & HR

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 20% Maximum time allocation (vs. previous 36-month avg) a founder can work post-close without triggering IRS 409A 'Separation from Service' failure.

The closing-packet document everyone signs without reading

Picture the close. The Purchase Agreement gets the lawyers, the reps and warranties get the negotiation, the escrow gets the wire instructions. And then there's a 4-page Founder Consulting Agreement that everyone treats as housekeeping. The founder skims it because it feels like a courtesy. The buyer skims it because they assume it's boilerplate. It gets signed in the same fifteen minutes as the parking validation.

That document is the single most likely thing in the packet to detonate eighteen months later. Not because the dollar amounts are large, but because two completely separate landmines live inside the same paragraph: a federal tax rule that can claw back 20 cents on every deferred-comp dollar, and an org-chart problem that quietly defeats the entire reason the buyer paid a premium for the company.

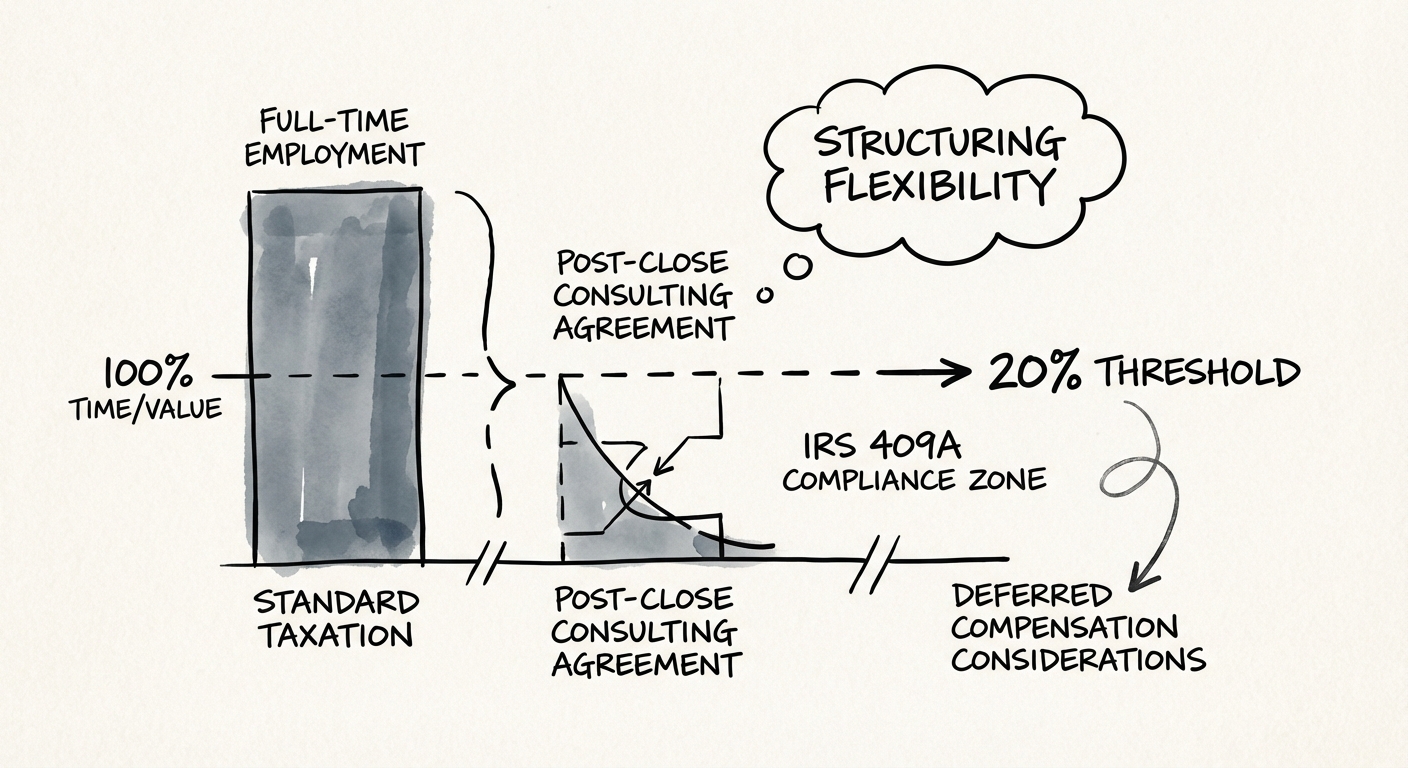

The 20% rule that turns a payout into a penalty

Start with the tax mechanics, because they're the part nobody at the table is qualified to spot in real time. Many founder payouts — earnout tranches, rolled equity, non-qualified deferred comp — are legally triggered by a "separation from service." The IRS does not let you self-certify that you've separated. It measures it. Under Section 409A, you have not separated if you keep providing services at more than 20% of your average level over the prior 36 months.

Run the founder's actual baseline before signing. Someone who ran a 50-hour week for three years has a baseline of roughly 50 hours. Twenty percent of that is about 10 hours a week — and a "couple days a week, just to help the transition" consulting gig sails right past it. The moment a 409A-triggered payment lands while the founder is still working 25% time, the separation was never valid. The consequence isn't a warning letter. It's a 20% additional federal tax on the founder, plus the premium-interest charge, on top of ordinary income tax. A clean liquidity event becomes a personal tax liability, and the founder usually doesn't find out until a CPA reads the engagement letter against the deal docs the following spring.

The Shadow CEO the agreement accidentally installs

The org problem comes from the same vagueness that creates the tax problem. Write "available as needed" into the scope and you haven't hired a consultant — you've kept the CEO and demoted the new one without telling anyone. Twelve years of muscle memory does not reroute because the cap table changed. A pricing exception, a key-account fire, a "should we really ship this" call — the team walks past the new leader's office to the person whose name is still on the founding story. Every one of those detours teaches the organization that the new CEO is provisional. That's the Shadow CEO, and a consulting agreement with an open-ended scope is how you build one on purpose.

A consulting agreement isn't a soft landing for the founder. It's a knowledge-extraction window with a hard expiration date. The kindest thing you can write into it is the day it ends.

What a consulting agreement should actually buy you

Reframe the whole document around a single question: what is the buyer paying to extract, and how fast can it be extracted? Not "retain the founder." Not "keep them happy." Extract the knowledge that lives only in their head, transfer the relationships that only respond to their phone number, and then close the window. Bain's analysis of the private equity landscape shows hold periods stretching out while transition windows compress — buyers have learned that long founder tails create drag, not insurance.

Duration: build to 3–6 months, not 12–24

The instinct is to buy a long runway "just in case." It backfires. The genuinely irreplaceable knowledge — why this contract has a weird auto-renewal clause, which engineer to call when the legacy billing job fails, what the real story is with the account that pays late but never churns — is finite, and a structured handoff gets most of it across in the first 90 days. Past six months, the marginal value of the founder's time approaches zero while the Shadow CEO risk keeps compounding. The extra time isn't transferring knowledge anymore; it's just postponing the day the founder emotionally lets go, and paying for the privilege.

Compensation: kill the hourly rate

This is the structural decision most agreements get backwards. Pay a founder by the hour and you have manufactured an incentive to find billable work — which, for a founder, means finding decisions to weigh in on. The right structure is a fixed monthly retainer against a capped availability:

- Retainer: a flat monthly fee, roughly $5,000–$15,000 depending on company size and the founder's depth of institutional knowledge.

- Availability cap: around 10 hours per month — deliberately set below the 409A 20% line, so the tax math and the org-chart math are protected by the same number.

- Overage rate: a deliberately steep hourly premium (say $500/hr) above the cap. Not to enrich the founder — to make the buyer's own team think twice before pulling the founder into something the new leadership should own.

Scope: the founder answers, the founder does not do

Write the scope as a verb test. The founder is paid to answer, never to do. "Provide historical context on the X repository." "Introduce the new CEO to the three accounts that signed on a handshake." "Explain why the legacy pricing model has that one grandfathered tier." Those are answers. The moment the scope says "manage key accounts" or "oversee the product roadmap," you have not written a consulting agreement — you've written an employment contract that happens to fail 409A and reinstalls the Shadow CEO in the same stroke. The line between consultant and shadow boss is the difference between transferring knowledge and retaining authority, and you draw it in the scope section or not at all.

Five clauses that separate a clean break from a slow leak

Before the founder signs, pressure-test the draft against five specific provisions. Each one closes a gap that standard templates leave wide open.

1. The no-authority clause

State in plain language that the consultant has no authority to bind the company or make operational decisions. This is doing double duty: it's the legal firewall against liability for the founder's actions, and it's the clause you point to when an employee says "but the founder approved it." If it isn't written down, the Shadow CEO has standing.

2. A fresh IP assignment for the consulting period

The Purchase Agreement assigned the IP that existed at close. It says nothing about what the founder might create during the consulting window — a new integration, a fix, a clever bit of process. Sign a separate intellectual property assignment scoped to the consulting term so that gray-zone work created after close doesn't become a future dispute over who owns it.

3. A broader definition of "Cause"

In an employment contract, "Cause" is narrow to protect the employee. In a consulting agreement, the buyer needs the opposite — the ability to end the arrangement immediately if the founder turns obstructionist, undermines the new leader, or becomes a culture risk. Negotiate "Cause" wide enough that termination doesn't require a lawsuit.

4. Non-compete that runs concurrently, not sequentially

This is the trap that costs founders the most and gets noticed the least. Confirm the consulting period runs concurrent with the non-compete restriction — not before it. A one-year consulting gig followed by a two-year non-compete that only starts on the consulting end date is a three-year lockout dressed up as a two-year one. Read the trigger date on the restrictive covenant, every time.

5. A successor-introduction protocol

Make the trust transfer a written obligation, not a hope. The agreement should require the founder to actively position the new leadership as the authority on every customer introduction — handing relationships forward rather than holding them as leverage. A founder who introduces the new CEO as "the person who'll take great care of you" is worth more than one who introduces them as "my temporary replacement." This is the hinge between a company that stays dependent on its founder and one that can actually run without them. If you want a deeper template, Baker McKenzie's guidance on transition services agreements covers the structural parallels worth borrowing.