The practical answer

- Short answer

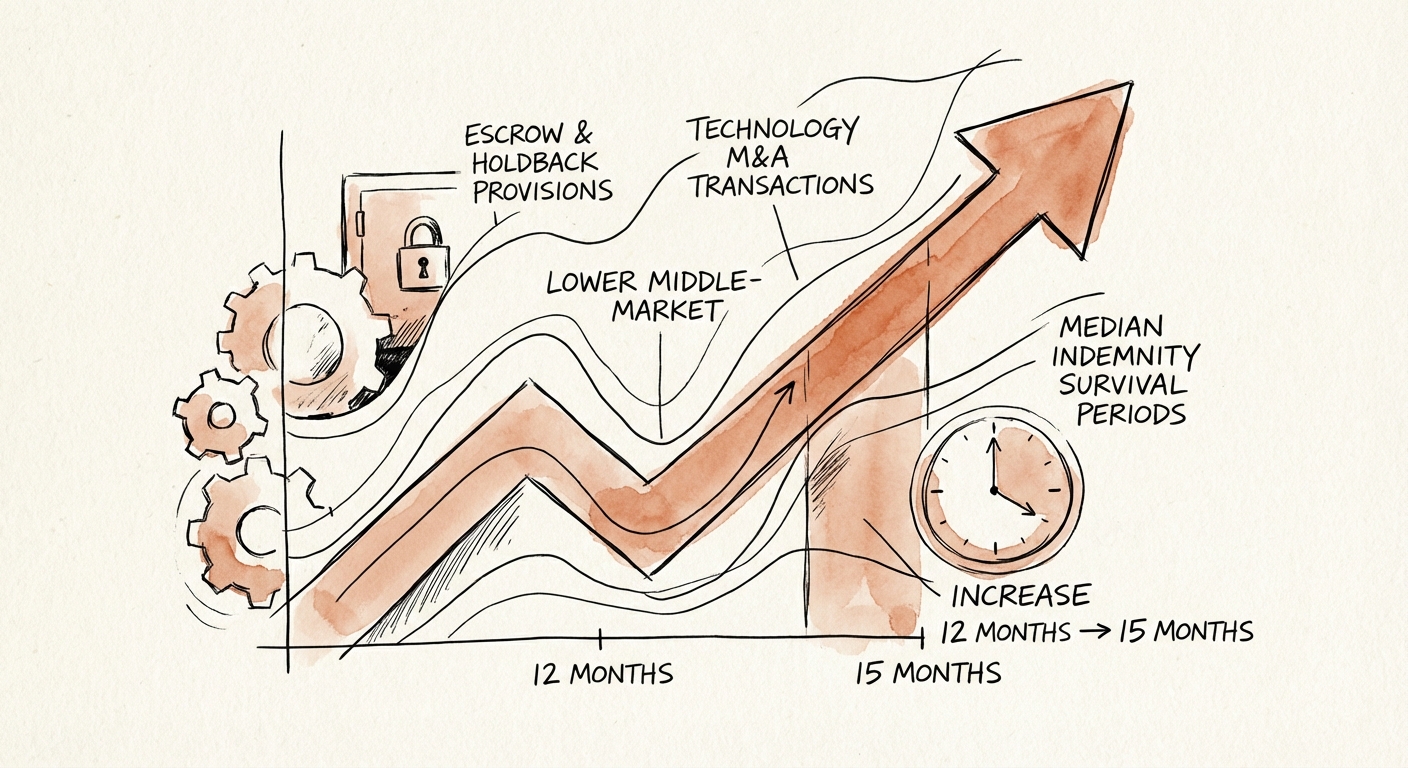

- Diagnostic guide on M&A escrow and holdback provisions. Learn why 15-month survival periods are the new norm and how R&W insurance can unlock 9.5% of your deal value.

- Best fit

- Industry: Technology M&A. Function: Legal & Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 9.5% The 'RWI Arbitrage': The median escrow drops from 10% to 0.5% when Reps & Warranties Insurance is utilized.

The 'Silent Partner' in Your Deal

You have signed the Letter of Intent (LOI). The headline price is $50 million. You have already mentally calculated your share, paid the taxes, and bought the house. But you have missed the line item that will determine whether you actually receive that money: the escrow provision.

In 2026, the gap between "Headline Price" and "Closing Cash" is widening. According to 2025 data from SRS Acquiom, 90% of private target M&A deals now include an escrow or holdback. The median amount is 10% of the transaction value for deals without Reps & Warranties Insurance (RWI). On a $50 million exit, that is $5 million of your capital sitting in a third-party account, functionally dead for more than a year.

The trend is moving against founders in one specific, painful way: Survival Creep. For years, the standard survival period for general representations and warranties was 12 months—just enough time for the buyer to run their first audit. In 2025, that median crept up to 15 months, particularly in the lower middle market ($10M–$100M deals). Buyers are demanding an extra quarter of exposure, knowing that "Undisclosed Liabilities" often surface during the second year of integration.

The RWI Arbitrage

The single most effective lever to break this trap is Reps and Warranties Insurance (RWI). In deals utilizing RWI, the median escrow drops from 10% to just 0.5% (typically matching the policy retention). For a $50M deal, this is the difference between locking up $5M and locking up $250k. If your counsel isn't pushing for RWI, they are leaving 9.5% of your deal value in limbo.

The 15-month survival period is the structural proof of buyer discomfort. It tells you that even after doing their homework, they expect the 'skeletons' of technical debt and churn to fall out of the closet in Q5 post-close.

Escrow vs. Holdback: The 'Possession' Gap

Founders often use the terms "escrow" and "holdback" interchangeably. Buyers love this confusion, because the difference is leverage. An Escrow puts your money in a neutral third-party account (like J.P. Morgan or SRS Acquiom) governed by a rigid agreement. To get that money back, the buyer must prove a claim. If they fail, the agent releases the funds to you.

A Holdback is simply a deferred payment. The buyer keeps the cash in their own bank account. If they feel you breached a representation—say, a technical debt issue surfaces that wasn't disclosed—they simply refuse to pay. They don't need to convince a third-party agent; they just stop the wire. You are then forced to sue your acquirer to get your own money back. In the hierarchy of deal protections, a holdback is a "setoff trap" waiting to happen.

The 'Special Indemnity' Weapon

Even if you negotiate a tight general escrow, sophisticated buyers in 2026 are increasingly using "Special Indemnity" holdbacks to carve out specific risks. These sit outside the general indemnity cap. Common targets include:

- Open Source Risk: If your code audit reveals GPL violations, buyers may demand a specific $2M holdback until remediation is confirmed.

- Sales Tax Nexus: In SaaS deals, "Wayfair" liabilities are rampant. Buyers will hold back 110% of the estimated exposure.

- IP Litigation: Any hint of a patent troll letter in your history can trigger a specific holdback that lasts for the statute of limitations (up to 6 years).

These provisions bypass the "tipping basket" protections you fought for in the main agreement. They are dollar-for-dollar deductions from your liquidity.

The Defense Playbook

To protect your exit, you must treat the Escrow Agreement as a financial instrument, not a legal formality. The default terms are designed to give the buyer a free option on your equity value. Your defense rests on three pillars:

1. The 'Tipping Basket' vs. The 'Deductible'

Never accept a "deductible" on your general indemnity basket. A deductible means the buyer eats the first $250k of losses, and you pay everything after that. A "tipping basket" (or "first dollar" basket) means that once losses exceed the threshold (e.g., $250k), the buyer can claim the entire amount back to zero. While a tipping basket sounds riskier, it actually protects you from "nickel and dime" claims. Buyers are less likely to manufacture small claims if they know they have to reach a significant threshold before seeing a penny.

2. The Anti-Sandbagging Clause

In 2026, pro-buyer jurisdictions (like Delaware) generally allow "sandbagging"—where a buyer can close the deal knowing about a breach, and then sue you for it immediately after. You must negotiate an Anti-Sandbagging provision, or at least a knowledge qualifier. If they knew about the revenue recognition issue before closing, they shouldn't be allowed to claim it against your escrow later.

3. The Release Mechanism

Standard escrow agreements are often silent on the mechanics of release. Demand a "Joint Written Instruction" clause that requires the buyer to actively object to a release within a tight window (e.g., 5 days) of the survival date. If they stay silent, the agent releases the funds. Without this, a lazy buyer can leave your money stranded in administrative purgatory for months.