The practical answer

- Short answer

- R&W insurance isn't a silver bullet. Discover the 'silent' 10% valuation trap in tech M&A, from AI code exclusions to the 'Sufficiency of Assets' clawback.

- Best fit

- Industry: B2B Technology. Function: Legal & Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 0.5% Average RWI retention (deductible) in 2026 tech deals, down from 1%—lowering the bar for buyers to file claims.

The 'RWI Safety Net' Has Holes: The Rise of AI Exclusions

For the last five years, Representations and Warranties Insurance (RWI) has been the magic wand of dealmaking. It allowed sellers to walk away with minimal escrow (often 0.5% to 1% of Enterprise Value) while shifting the risk of a breach to an insurer. Founders slept well, believing their exit was 'risk-free' post-close.

In 2026, that safety net is fraying—specifically for technology companies. While premium rates have dropped to historic lows (~2.5% of policy limits), insurers are aggressively introducing specific exclusions that leave founders personally liable for the most volatile risks in their stack: Artificial Intelligence and Open Source compliance.

The emergence of "Absolute AI Exclusions" in RWI policies means that if your engineering team used GitHub Copilot or ChatGPT to generate code without strict governance, the insurer will not cover the resulting IP breach claims. Buyers know this. They are responding by demanding special indemnities—uncapped, personal liability buckets that sit outside the insurance policy. If you cannot prove data provenance for your AI models or clean IP ownership for your codebase, you aren't just risking a lower valuation; you are risking a clawback that pierces the corporate veil.

In 2026, the most dangerous words in a purchase agreement aren't in the indemnification cap—they're in the disclosure schedules. If it's not listed, you're liable.

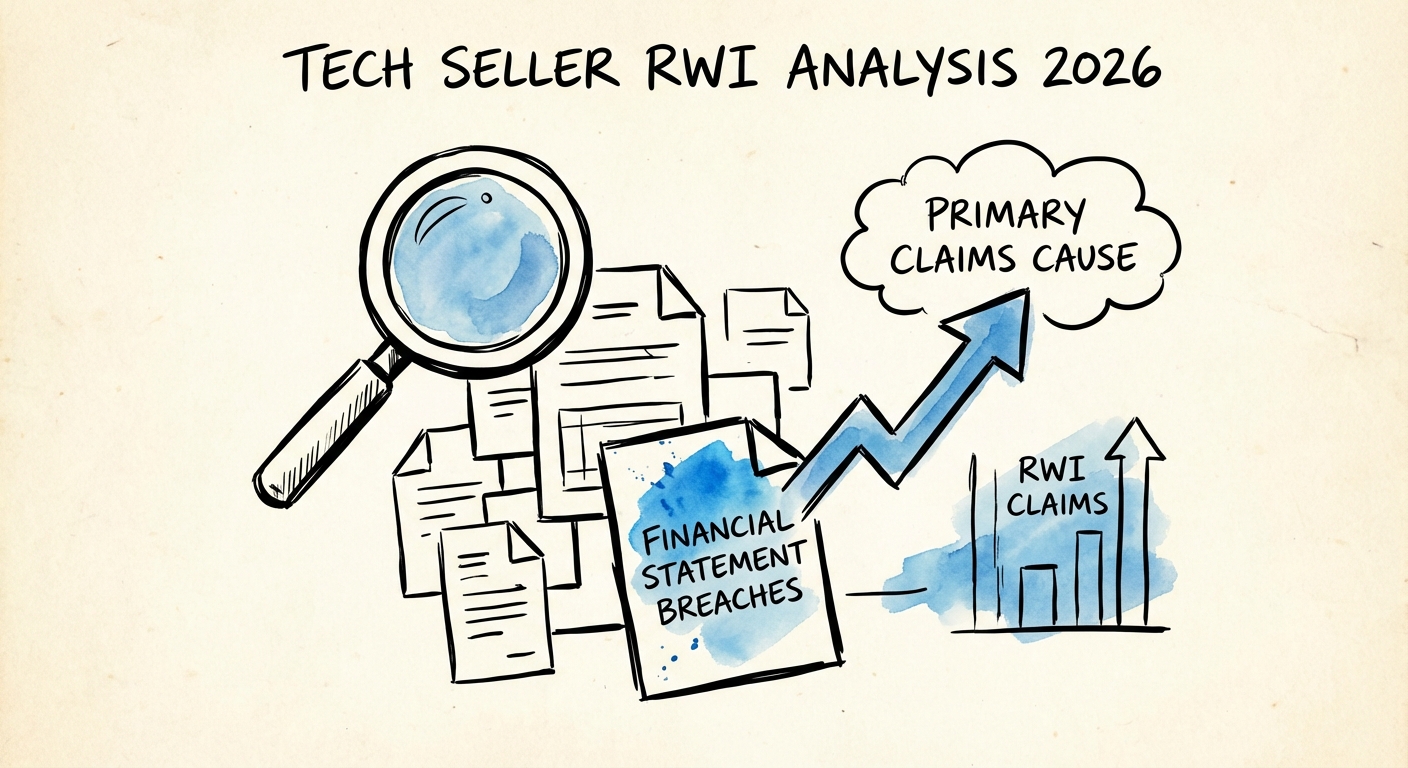

The 'Financials' Rep: Where 55% of Claims Originate

Tech founders often treat the "Financial Statements" representation as a formality, assuming their audit protects them. It does not. According to recent claims studies, over 55% of RWI claims now stem from breaches of financial representations. The disconnect lies in the gap between GAAP financials and the metrics you sold the deal on.

In 2026, private equity buyers are using the definition of "Financial Statements" to include management reports, KPI dashboards, and ARR bridges. If your representation states that your financial data is "true and correct," but your Quality of Earnings (QofE) reveals that your churn calculation excluded 'down-sells,' you haven't just made a modeling error—you have breached a warranty.

This allows buyers to file a claim for the multiple of the error, not just the dollar value. A $100k error in EBITDA, applied to a 12x multiple, becomes a $1.2M breach claim. Since RWI policies often have a retention (deductible) of 0.5% to 1% of deal value, smaller claims might not trigger insurance, leaving the payout to come directly from your escrow or working capital adjustment.

The 'Sufficiency of Assets' Trap: When Technical Debt Becomes Legal Debt

Historically, the "Sufficiency of Assets" representation was designed for manufacturing firms—ensuring the factory had enough machines to produce the widgets. Today, tech buyers are repurposing this clause to penalize technical debt.

If your platform requires a complete refactor to scale from 10,000 to 100,000 users, buyers argue that the assets (code) are insufficient to conduct the business as described in your confidential information memorandum (CIM). This is no longer just a roadmap item; it is a breach of contract.

Smart sellers are countering this by conducting a pre-sale technical debt assessment and disclosing scalability limits in the disclosure schedules. By explicitly listing known bottlenecks, you transfer the risk to the buyer. If you hide them (or remain ignorant of them), you hand the buyer a signed confession for a post-close indemnity claim.