The practical answer

- Short answer

- Don't let 'standard' terms trap your rollover equity. A diagnostic guide to negotiating Good Leaver clauses, non-competes, and retention packages in PE deals.

- Best fit

- Industry: B2B Technology. Function: Legal & HR

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 82% Of sponsors pay Fair Market Value for rollover equity in 'Good Leaver' scenarios. Without this clause, you risk repurchases at cost.

The Misalignment: You Are No Longer the Boss

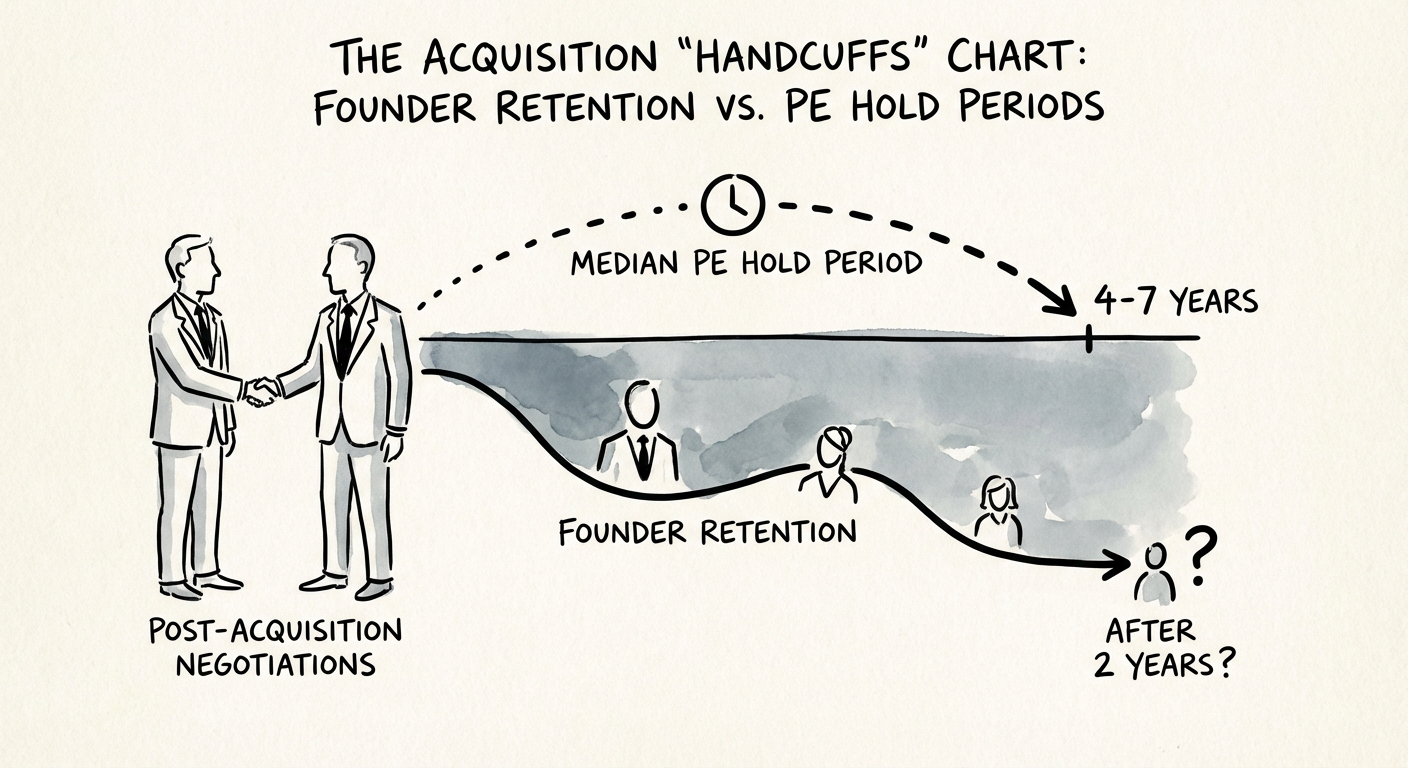

The most dangerous document in a definitive agreement stack is not the Purchase Agreement; it is the Employment Agreement. For the last decade, you have been the Captain. The moment the wire hits your account, you become Employee #1. This psychological shift is jarring, but the financial implications are worse if ignored.

Here is the math that creates the trap: In 2025, the median private equity holding period dropped to 5.8 years, down from highs of 7 years but still significantly longer than the average founder's post-acquisition tenure. Most founders mentally commit to 18 to 24 months of "integration and transition." The PE firm, however, is underwriting a 5-year value creation plan that likely requires your continuity.

This duration mismatch creates leverage for the buyer. If your employment agreement is standard, quitting in year two often triggers "Bad Leaver" provisions that allow the fund to repurchase your unvested rollover equity at cost—wiping out millions in potential "second bite" value. You are essentially signing a contract that says, "I will stay for six years, or I will forfeit 40% of my deal value."

You are essentially signing a contract that says, 'I will stay for six years, or I will forfeit 40% of my deal value.' If you don't negotiate the exit ramp before you enter the highway, you will pay for it with your equity.

The "Good Leaver" Shield: Define It or Lose It

The battle for your rollover equity is fought in the definitions section. Specifically, the distinction between a "Good Leaver" and a "Bad Leaver." In a 2025 study of private equity repurchase terms, 82% of sponsors agreed to pay Fair Market Value (FMV) for rollover equity if the founder was deemed a "Good Leaver." If you are a "Bad Leaver," that number drops to near zero.

Most standard PE templates define "Good Leaver" narrowly: death or disability. You must expand this to include termination without "Cause" and resignation for "Good Reason."

Three Critical Definitions to Negotiate

- Narrow "Cause": Do not accept broad definitions like "failure to perform duties." Limit "Cause" to felonies, fraud, or willful misconduct that materially harms the company. "Underperformance" is not Cause; it is a reason to fire you, but not a reason to steal your equity.

- Broad "Good Reason": You need a parachute if the PE firm changes the deal. "Good Reason" to resign (and keep your equity) should include: a reduction in title or reporting line (e.g., reporting to a new CEO instead of the Board), a material reduction in compensation, or a forced relocation of more than 30 miles.

- The "Sunset" Clause: Negotiate a transition mechanism where, after 24 or 36 months, you can voluntarily move to a Board role without triggering Bad Leaver forfeiture. This aligns your timeline with the fund's hold period.

The Non-Compete Reality: The FTC Won't Save You

Do not bank on the Federal Trade Commission's proposed ban on non-competes to invalidate your restrictions. While the regulatory landscape is shifting, the "Sale of Business" exception remains a robust legal standard. Courts consistently uphold strict non-competes for individuals who have sold a business for significant value (specifically, typically owning at least 25% of the entity).

The danger lies in the scope. A standard PE non-compete will define the "Restricted Business" as "any business the Company engages in or plans to engage in." If your SaaS platform does marketing automation today, but the PE firm plans to acquire a CRM next year, you could be barred from the entire martech stack.

The Fix: Limit the non-compete to the current products and services of the company at the time of closing. Reject "forward-looking" restrictions. If you leave in year two, you shouldn't be blocked from starting a company in an adjacent space just because your former acquirer might pivot there eventually.